Author

Article Highlights

- News media and thought leaders use survey findings to report household financial stability

- More Americans can pay a $400 emergency expense today than in 2013

- However, findings vary by race/ethnicity and employment status

Can you afford a $400 emergency expense right now? If so, how would you pay for it? Every year since 2012, economists from the Board of Governors of the Federal Reserve System have asked these and other consumer-finance questions to a representative sample of U.S. adults through the Survey of Household Economics and Decisionmaking, or SHED. Findings from the latest SHED, conducted in late 2020, were released on May 17. While the survey asks more than 100 questions on a range of topics related to household financial well-being, the question about the ability to pay for a $400 emergency expense has garnered regular attention from the media, policymakers, and the broader public, and has become a go-to data barometer for measuring the financial fragility of Americans.

The go-to barometer

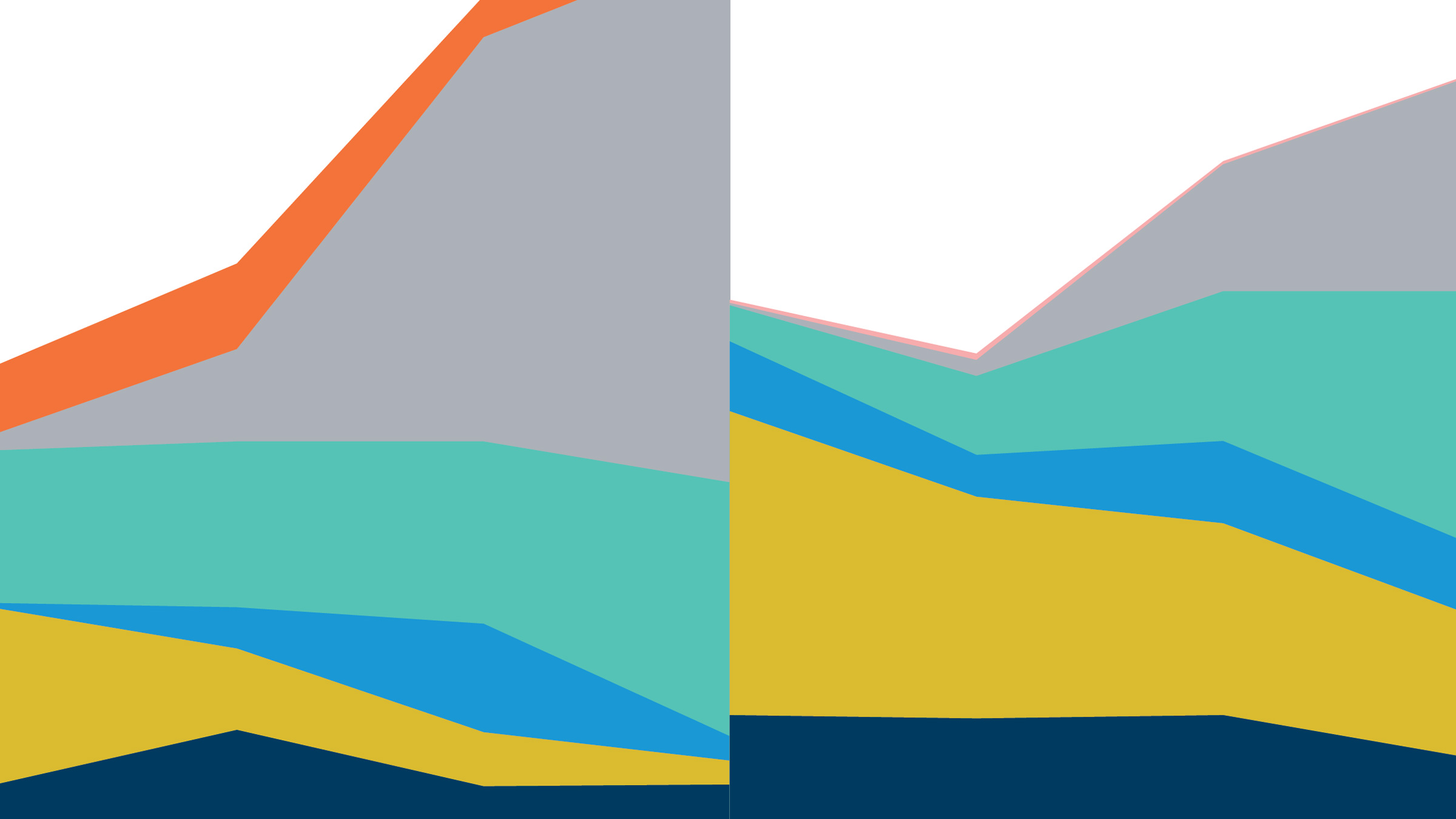

The $400 statistic is widely quoted in the news media’s coverage of America’s financial well-being. An examination with a standard news-search tool, NewsBank’s Access World News database,* reveals that the specific keyword-search phrase “$400 emergency expense” has appeared in more than 1,000 unduplicated news content features in the United States since 2014. Use of the $400 statistic in news content started out small but increased over time, likely as the SHED became more renowned. Appearances peaked in 2019, with the $400 statistic mentioned in more than 300 news sources that year. Newspapers cited the statistic the most (192 instances), followed by newswires (69 instances) and web-only news content providers (32 instances).

A review of news content from that year shows that a broad range of institutions used the $400 emergency-expense data to frame stories about inequality, poverty, savings, and personal finance. The May 23, 2019, release of 2018 SHED data was covered by a variety of national news organizations, including The Washington Post, Bloomberg, and ABC News. Several weeks later, CNBC published a more in-depth story on the survey findings and led their coverage with responses to the $400 question, stating: “The statistic is used to show how unequal things have become in the U.S.: Some 40% of Americans would struggle to come up with even $400 to pay for an unexpected bill.”

Inclusion of the $400-emergency-expense question and accompanying statistic in news content peaked, in part, due to their contextual use for framing the financial hardships households faced during the federal government shutdown in January 2019. Throughout the year, though, a variety of national and regional news organizations, such as TIME magazine and the Detroit Free Press; public policy organizations, such as the Brookings Institution and the Center for American Progress; and personal finance blogs and newsletters, such as the Motley Fool; relied on this specific SHED statistic to help frame their stories, data analyses, and consumer advice.

Policymakers and thought leaders also use the $400 question and statistic as a barometer for financial well-being. On the presidential campaign trail, then-Senator Kamala Harris used them to frame a discussion about the economic difficulties American families confront. Neal Gabler, a journalist with The Atlantic, highlighted the $400 data point to draw readers into his personal story of financial insecurity. Personal finance guru Zach Friedman, writing in Forbes magazine, drew on them to provide advice to readers managing their own emergency funds. Lastly, economist and former Assistant Secretary of the Treasury Alicia Munnell used them in her MarketWatch op-ed that questioned the ability of some households to save for retirement.

How financially fragile are American families?

Taken together, the SHED’s questions on emergency savings provide important insight into the financial fragility of American families. The specific questions, included in the survey since its first edition in 2012, are:

- Have you set aside emergency or rainy-day funds that would cover your expenses for three months?

- Suppose that you have an emergency expense that costs $400. Based on your current financial situation, how would you pay for this expense?

As the Brookings Institution points out in their June 2019 article “Six facts about wealth in the United States,” news organizations haven’t always gotten this statistic right, sometimes characterizing the “I would have difficulty paying a $400 emergency expense” response to the second question above as meaning “I can’t” pay an emergency expense. The precise use of the question and statistic is important, especially for policymakers, since an imprecise interpretation may overestimate the financial hardships households face, when the actual share of households who can’t pay the expense is much lower (see below).

In the development of these survey questions about emergency savings, Federal Reserve economists sought to measure how many people had an emergency fund that was attuned to respective budgets. They also sought to gauge how much of a financial hardship a small, unexpected expense, such as a car repair or a modest medical bill, would be for a family.

“When we first launched the SHED, there was still much we didn’t fully understand about how people were experiencing various aspects of their financial lives,” said David Buchholz, deputy associate director in the Federal Reserve Board’s Division of Consumer and Community Affairs. “We designed the ‘$400 question’ to understand the effects of a much more modest financial bump in the road than some traditional measures, such as the three-month safety net question. I’m not sure that any of us expected to see just how many people would struggle with paying for such a modest expense, indicating a concerning level of financial fragility.”

In 2013, the findings from the first survey painted a bleak financial picture of American families four years after the end of the Great Recession. The survey estimated that only four in ten adults had set aside enough funds to cover three months of expenses. In addition, the survey estimated that 50 percent of all adults would have difficulty paying for a $400 emergency expense, with 19 percent of adults—one in five—not being able to pay the expense at all.

After 2013, as the economy has recovered from the Great Recession, responses to the two emergency-expense questions have shown the financial position of Americans stabilizing, and perhaps even strengthening. By 2020, the share of adults who had set aside three-month emergency funds had risen by 16 percentage points, to 55 percent, and the share of households having difficulty paying a $400 emergency expense declined by nearly the same percentage margin, to 36 percent of all households. Even during the economic downturn that resulted from the COVID-19 pandemic in 2020, the share of respondents having difficulty paying a $400 emergency expense or unable to pay it remained relatively stable, dropping to 30 percent in July 2020 before returning to 36 percent at the end of the year. The temporary decline is likely due to infusions of state and federal resources and pandemic-relief funding to support American households.

Yet beneath the positive trajectory for financial well-being at the aggregate household level, the survey found important differences by demographic characteristics and employment status that suggest the economic distress caused by the pandemic was starkly uneven. At the end of 2020, for example, 45 percent of adults who were laid off in the past 12 months indicated they were not able to pay their bills or would not be able to do so if facing a $400 emergency expense, versus 24 percent of adults who were not laid off.

The survey also revealed that Black and Latino/a adults, even after accounting for their employment status, were more financially fragile than White adults at the end of 2020 when it came to paying their monthly bills after covering a $400 emergency expense. In 2020, for example, 18 percent of White adults who were not laid off could not pay off all their monthly bills after covering a $400 emergency expense, versus 39 percent of Black and 38 percent of Latino/a adults who were not laid off. When the survey examines those who were laid off in the past 12 months, the share of adults increases markedly, with the gaps between demographic groups remaining in place.

Latest SHED findings point to hardship and persistent gaps

Results from the 2020 annual SHED give us a better understanding of the financial well-being of families when the United States was at or near the peak of COVID-19 infections and in a period of elevated unemployment. Thanks to federal and state resources and funding households received during 2020, several measures of financial stability remained mostly unchanged since 2019. However, the SHED results also reveal the emergence of potential financial well-being challenges and the presence of persistent gaps. For example, the share of adults who reported that they were worse off financially than a year earlier increased to the highest level since 2014 (close to one-quarter of all respondents in 2020, compared to 14 percent in 2019 and 21 percent in 2014). In addition, racial and ethnic gaps in financial well-being caused by the ongoing economic distress remained.

Thank you to Sara Brandel of Research Information Services at the Minneapolis Fed for excellent research assistance.

Endnote

* Access World News is a comprehensive resource that includes more than 8,000 news publications from nearly 200 countries worldwide. These sources include major national and international newspapers, as well as local and regional titles.

Michael works to advance the economic well-being of Indian Country and low- to moderate-income individuals, households, and communities. He has conducted research and published articles on affordable housing, community development corporations, homeownership disparities, and foreclosure patterns and mitigation efforts.