Authors

If you ask a Minnesota home seller about the prospects for a buyer, you'd better bring your parka to protect you from the icy stare.

As many are now quite familiar, selling a home in Minnesota, and throughout much of the Ninth District, is much more difficult than it used to be. In April of this year, the average home for sale in the Twin Cities sat on the market for 154 days—a month longer than the previous April—and it received just 92 percent of the asking price, according to the Minneapolis Area Association of Realtors. Despite the fact that more homes were for sale, existing home sales in Minnesota in the first quarter of 2008 declined by 11 percent—some 12,000 units—from the same period a year earlier, according to the National Association of Realtors.

Misery loves company, and Minnesota can take cold solace from widespread news stories bemoaning housing market conditions in many parts of the district. Maybe worse, homeowners and the entire housing industry are still feeling nervously for the bottom.

The prevailing pessimism in frequent headlines can make one think that the housing industry has slumped to levels rarely seen before. A longer view, however, shows that housing activity (as of May) has certainly slowed, but remains above 1999 levels for many indicators. There is also considerable variation within the district; housing markets in Montana and the Dakotas have not experienced the same decline as those in Minnesota and Wisconsin.

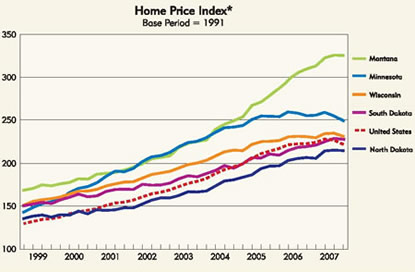

To put current activity in better context, go back to the 1990s. From 1991 to 1999, housing values in Minnesota appreciated an average 4 percent per year—not bad, but almost turtlelike compared to what happened after this period in Minnesota and throughout the Ninth District. From 1999 through the second quarter of 2006—roughly the peak in housing prices in the district's larger states—nominal housing prices in Minnesota leapt by 82 percent, or an average annual rate of almost 9 percent. Every district state saw housing appreciation of at least 43 percent. Indeed, homes in the Dakotas and especially in Montana continued to appreciate. Prices in some urban areas—Minneapolis-St. Paul; Duluth, Minn.; Missoula, Mont.—also rose by more than 80 percent.

But starting in 2006, home values in much of the country began to fall, often commensurate with previous gains. Previously hot coastal markets such as Sacramento, Calif., and Fort Myers, Fla., have seen double-digit percentage price drops on the heels of triple-digit gains since the beginning of the decade. On the other hand, more stable markets have averted losses.

The Ninth District, with the exception of a strong Montana market, mirrors this national trend. From the second quarter of 2006 to the fourth quarter of 2007, Minnesota home prices declined almost 4 percent, according to the Office of Federal Housing Enterprise Oversight, a regulatory agency (see chart below). Price data from other sources suggest that prices might have taken a much steeper dip, at least in some places. For example, the median sale price for homes in the Twin Cities fell from $230,000 in April 2006 to $204,000 in April 2008, and had dipped below $200,000 earlier in the year, according to the Minneapolis Area Association of Realtors.

At the other end of the spectrum, North Dakota and South Dakota showed more modest appreciation in home values, but through the end of last year, home prices in the Dakotas barely dipped, declining by just 0.3 percent.

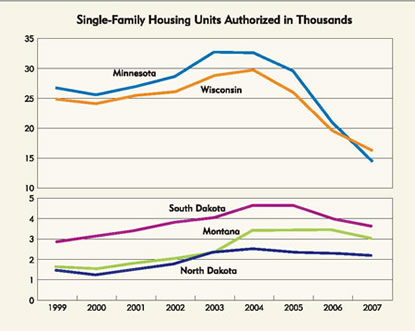

Building permits and home sales also reflect the tendency for hotter markets to cool more quickly. In 1999, approximately 57,000 single-family building permits were issued in the five-state region. Permits slowly increased until they spiked from 2003 to 2005, with the bulk of the increase coming from Minnesota and Wisconsin (see chart).

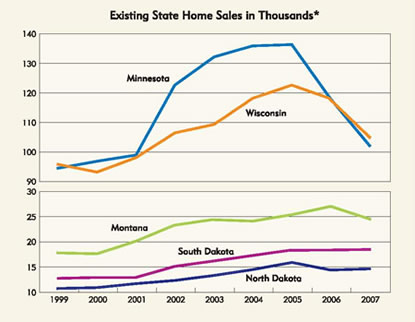

But since then, permit totals have fallen dramatically—to about 40,000 in 2007. Here, too, Minnesota and Wisconsin bore most of the decline, with permit levels falling well below 1999 levels. Likewise, sales of existing homes in Minnesota and Wisconsin have fallen back toward 1999 levels, while sales in the Dakotas and Montana remain well above their 1999 benchmarks (see chart).

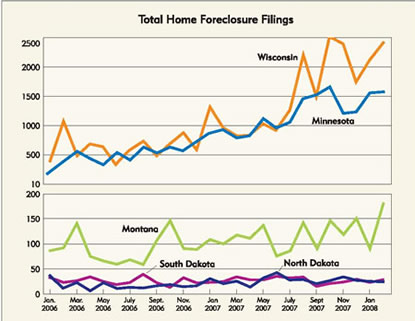

Foreclosure data offer additional, and painful, examples of the contrast between Minnesota and Wisconsin and the rest of the district (see chart). In January 2006, both Minnesota and Wisconsin had fewer than 500 foreclosure filings. By February 2008, monthly filings had increased sixfold to nearly 1,600 and 2,400 in Minnesota and Wisconsin, respectively.

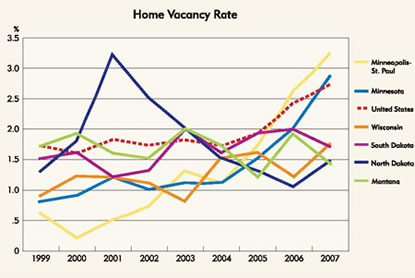

Other district states saw increased foreclosures, but not nearly at the rates of Minnesota and Wisconsin. As a result of high foreclosures, home vacancy rates have also shot up; in Minneapolis-St. Paul, the rate has gone from virtually zero (0.2 percent) in 2000 to more than 3 percent (see chart).

The new normal?

Despite the pain in district housing markets, particularly in Minnesota and Wisconsin, the sky hasn't fallen, at least completely. Rather, the market appears to be orienting itself closer to the historical trend line. The first half of this decade showed a dramatic increase in housing values, building authorizations and sales volume. After an unprecedented housing expansion, the district is now feeling the pain of contraction to what appears to be a more sustainable housing market, with Minnesota and Wisconsin suffering the most after several years of exceptional growth.

Conversely, the North Dakota and South Dakota markets have cooled more slowly in proportion to their more measured growth over the period. Whether that continues is hard to say.

South Dakota, for example, had been riding a hot housing market in Sioux Falls for several years running. But single-family permits fell significantly in 2006, and last year fell again, this time to pre-1999 levels, according to Census figures. During this period, the construction sector shifted hammers to a growing multifamily housing sector. But whether that continues is dicey: Through the first quarter of this year, total housing permits in Sioux Falls were less than half their 2007 levels, with both single- and multifamily units seeing a sharp drop.

Montana is the district wild card. Between 1999 and 2007, prices exploded with sales and building showing significant increases. In spite of growth over the past several years, Montana has not experienced the downturn in accordance with the district pattern. Some of the state's high growth areas are showing signs of housing fatigue; Flathead, Missoula and Gallatin counties are showing a dip in housing starts, for example, and last year the Missoula area reported its first decline in home sales in five years. Still, housing indicators across the state remain relatively strong. In Missoula, housing prices went up by 6 percent last year despite lower sales, according to an April report from the Missoula Organization of Realtors.

Glenn Oppel, government affairs director of the Montana Association of Realtors, characterized his expectations for the Montana market as "pretty steady." In a way, it's been pretty steady in other district markets of late, just steadily bad. Homeowners in Minnesota and elsewhere are hoping that frowning trend line turns upside down soon.

Ron Wirtz is a Minneapolis Fed regional outreach director. Ron tracks current business conditions, with a focus on employment and wages, construction, real estate, consumer spending, and tourism. In this role, he networks with businesses in the Bank’s six-state region and gives frequent speeches on economic conditions. Follow him on Twitter @RonWirtz.