Author

The declining prospects of America’s working class are widely discussed and hotly debated these days, from the anthems of Bruce Springsteen to the “deaths of despair” research of Princeton economists Anne Case and Angus Deaton.

A paper from the Opportunity & Inclusive Growth Institute explores this downhill trend for less-educated men and women by comparing life outcomes of two cohorts born 20 years apart. It shows that for the more recent generation, the American dream has undeniably vanished.

“The Lost Ones: The Opportunities and Outcomes of Non-College-Educated Americans Born in the 1960s” (Institute Working Paper 19) compares wages, medical expenses, and life expectancy for non-college-educated white men, women, and couples born in the decade around 1940 with circumstances for those born 20 years later—a cohort 49-to-58 years old as of 2014. The paper’s authors, Institute senior scholar Mariacristina De Nardi and colleagues Margherita Borella and Fang Yang, then analyze how those differences have affected the two cohorts’ labor market outcomes and will affect their lives in retirement. Their goal, they write, “is to better measure these important changes in the lifetime opportunities … and to uncover their effects on the labor supply, savings, and welfare of a relatively recent birth cohort.”

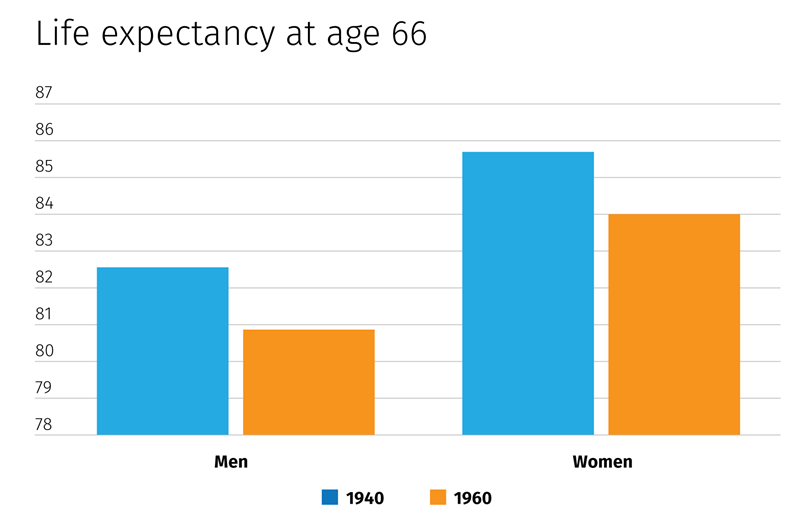

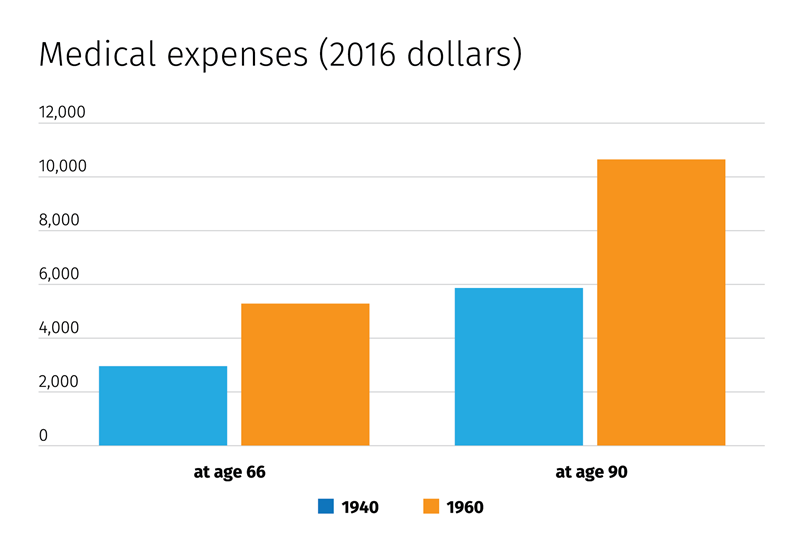

In brief, they find a profound deterioration in well-being. Accounting for inflation, wages have declined for non-college-educated white men. And while wages have increased for women, it’s only because their human capital (education and experience) has drastically increased over this time period. These men and women—comprising 60 percent of their age group—are also expected to experience much higher out-of-pocket medical expenses in retirement and large decreases in life expectancy compared with their earlier counterparts (see figures). They “would have been much better off if they had faced the corresponding lifetime opportunities of the 1940s birth cohort.”

The magazine of the opportunity & Inclusive Growth institute

Borella, De Nardi, and Yang focus on whites for methodological reasons—the need for a sufficiently large and homogeneous data set—not from a sense that they alone suffer bad times. “White non-college-educated Americans are hardly the only disadvantaged population losing ground,” they write, citing research on stagnant wages and dramatic declines in employment rates for less-skilled black men, along with rising incarceration rates and persistent black-white skill gaps.

Generational change, for the worse

To arrive at these conclusions, the researchers take three steps. First, analyze existing data sets in a novel way. Second, compare generations. And third, build a “life-cycle” model of labor supply and savings with single and married people. Using this model, the economists analyze the impact that the later generation’s worse wage schedules, medical expenses, and life expectancy profiles have had on their labor supply, savings, and welfare.

The data being analyzed refer to people who are white, have less than 16 years of education, and were born between 1936 and 1945. The comparison is made with the cohort of whites with the same educational achievements but born 20 years later, between 1956 and 1965. The data show that things got significantly worse. Men’s wages dropped by 9 percent (inflation-adjusted.) Women’s were 7 percent higher but, again, only because of higher human capital. Out-of-pocket medical expenses after age 66 increase by 82 percent. Still worse, life expectancy at middle age declines by 1.7 years for men and 1.1 years for women. “All of these changes are thus large,” observe the economists, “and have the potential to substantially affect behavior and welfare.”

Impact of change

The economists test their theoretical model by seeing if it can generate estimates close to actual data. It does. Model estimates closely match data on labor market participation, hours worked, and asset accumulation for all four demographic groups—single men, single women, married men, and married women—of the 1960s cohort over their entire working lives.

The final step is using the model to measure the impact these changes have had on the well-being of the 1960s generation.

They compare actual labor force participation, hours worked, and savings for the 1960s cohort with the outcomes generated if that cohort had enjoyed the higher wages, lower health expenses, and longer lifespans of the older generation. They first analyze one input at a time—wages, health costs, lifespans—and then all three together.

The effects of these changes on labor supply and savings vary by demographic group (male, female, single, married) but, in most cases, the impacts are substantial. If just wages had stayed at 1940s schedules, for example, while health expenses and lifespans were kept at 1960s levels, married couples would have had the most different labor market outcomes, with husbands staying in the labor force much longer and wives having lower participation rates and working fewer hours because of the much higher wages for men in the 1940s.

Study authors

Mariacristina De Nardi, Thomas Sargent Professor, University of Minnesota, and an Institute consultant. Her co-authors on this working paper are Margherita Borella of the University of Turin and Fang Yang of Louisiana State University.

Changing just health expenses or just lifespans would have altered labor outcomes less significantly. “The decrease in life expectancy mainly reduced retirement savings,” the economists observe, “but the expected increase in out-of-pocket medical expenses increased them by more.”

Loss of welfare

The final question is the impact on overall welfare, a measurement the economists make by estimating the lump-sum compensation an individual would require to be indifferent between the 1940s and 1960s wages, medical expenses, and health and survival dynamics. The sums are large: $126,000 for single men, $44,000 for single women, and $132,000 for couples. Lower wages account for most of the welfare loss, between 47 percent and 58 percent, depending on demographic group. Shorter life expectancies explain 26 percent to 34 percent of the decrease in well-being, and higher medical expenses account for the rest.

These deep welfare losses, along with the associated effects on labor supply, health care spending, and asset accumulation, contrast starkly with the American economy’s strong aggregate growth, indicating that this large segment of the population has not enjoyed the fruits of that broad economic health. By illuminating that difference, this research can serve well in any effort to, in the economists’ words, “evaluate to what extent current government policies attenuate these kind of shocks and whether we should re-design some policies to reduce their impacts.”