The economy can present funding challenges for consumer, agricultural, and commercial borrowers, as well as the community banks and credit unions that provide vital financing to them. Low commodity prices, challenging weather, simmering trade tensions, and volatile real estate markets amplify seasonal liquidity challenges facing banks and credit unions. The Federal Reserve Bank of Minneapolis’ Seasonal Lending Program may help mitigate these liquidity pressures. This article briefly summarizes the Seasonal Lending Program and serves to remind Ninth District depository institutions of its potential benefits.

What is the Seasonal Lending Program?

Under the Seasonal Lending Program, eligible banks and credit unions may qualify for a seasonal credit allocation, up to nine months during the calendar year, to meet the seasonal borrowing needs of the communities they serve. Eligible depository institutions must have less than $500 million in deposits. They must also demonstrate a seasonal need for funds, as indicated by a consistent pattern of seasonal swings in total deposits and loans over the past three years. The Seasonal Lending Program is not intended to substitute for core deposit growth, but to support community banks and credit unions that may have limited or unreliable access to national money markets. The interest rate for seasonal borrowing is usually below that for borrowing primary credit from the discount window. In the Ninth District, borrowing terms can be monthly instead of daily.

Seasonal Lending in the Ninth District

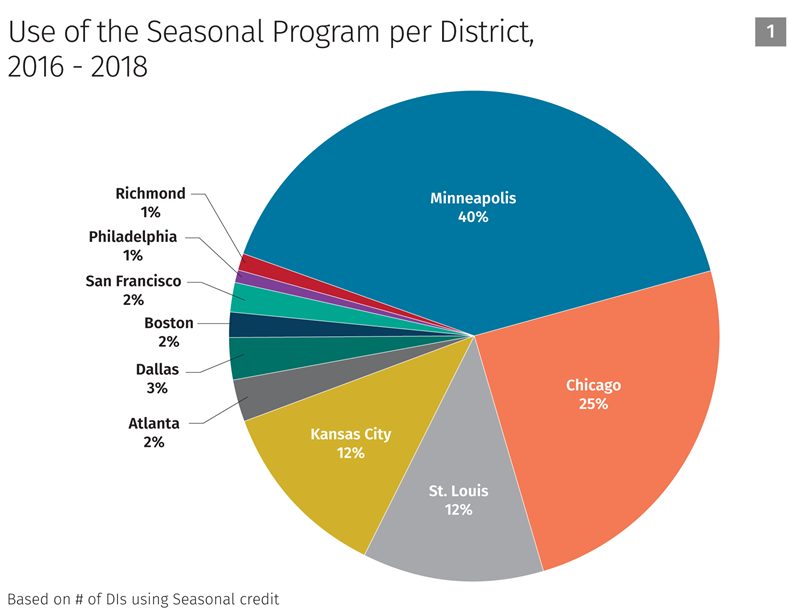

In recent years, the Ninth District has had the highest number of institutions using the Seasonal Lending Program in the Federal Reserve System. Community banks and credit unions in this district constitute 40 percent of the users of the System’s seasonal lending. The other Midwestern Federal Reserve districts also account for significant percentages: Chicago at 25 percent, and St. Louis and Kansas City at 12 percent each.

A variety of reasons can cause an institution’s seasonal fluctuations in deposits and loans, depending on its customers’ industries:

- farming

- higher education

- municipal deposits

- construction

- tourism

- any other seasonal types of businesses

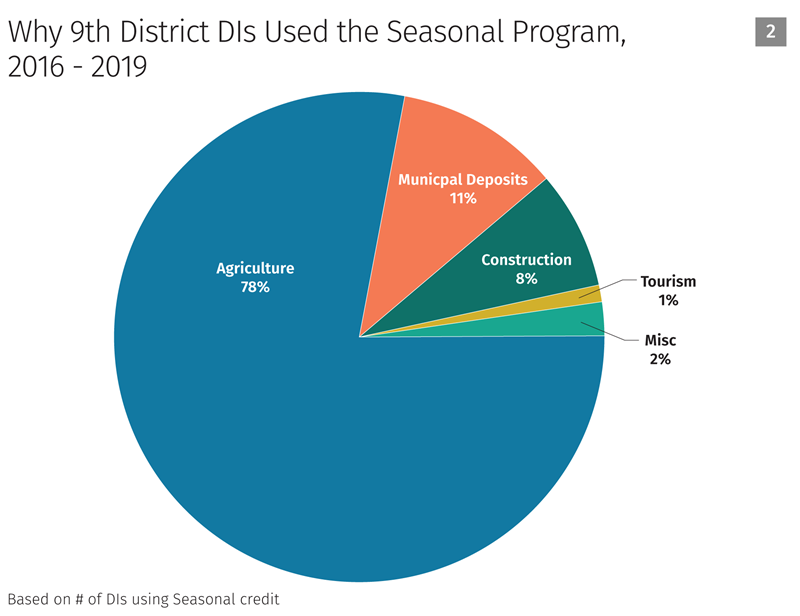

In the chart below, you can see that agricultural loans are the most common seasonal need in the Ninth District, along with some others:

Common reasons why banks and credit unions use the Seasonal Lending Program include:

- Agricultural loan advances and repayments

- Seasonal fluctuations in loans and deposits due to municipal deposits

- Large deposits and withdrawals several times a year from tax collections

- Home construction and commercial customers with variable deposits and credit needs that vary from year to year

- Lower deposits between the winter tourist season and the summer tourist season

Learn more

Ninth District institutions are encouraged to consider the Seasonal Lending Program as a potential tool in liquidity management and funding for loans to their local communities.

Begin by ensuring that your institution has established access to the discount window. If it has not, complete the required Operating Circular 10 (OC-10) agreements found on the discount window website.

For more information, visit https://www.frbdiscountwindow.org/ or contact Minneapolis Fed discount window staff directly at (877) 837-8815.

You can download the Seasonal Lending Program application form and brochure, which provide more details: https://www.frbdiscountwindow.org/pages/select-your-district/minneapolis/seasonal-lending-program-and-application-form-for-minneapolis-9th-district-.