Authors

Article Highlights

- Saint Paul’s rent-stabilization policy blamed for production disruptions, owner hardships

- Decline in apartment values is affecting homeowner property taxes

- Overall, rents in the city are dropping

Saint Paul, Minnesota’s capital city, has adopted several changes to its housing and development policies over the last few years. As neighboring Minneapolis attracted national headlines for its Minneapolis 2040 Plan, which allowed development of duplexes and triplexes on lots that previously allowed only single-family detached homes, Saint Paul adopted an ordinance that allows up to four to five units on such lots. While that zoning change in Saint Paul didn’t garner much notice, the city is drawing national attention for its 2021 referendum adopting rent stabilization.

With this backdrop, the Federal Reserve Bank of Minneapolis has now launched the Saint Paul Housing Dashboard, an online tool to monitor the city’s housing market, including rents, housing production, affordability, and stability. The dashboard is designed to help users understand Saint Paul’s demographics and track how housing supply and costs are changing, both within the city and in regional and national comparison cities. In this article, we explore findings from our inaugural analysis of the dashboard data. To supplement those data, we interviewed an array of housing market stakeholders about the challenges and opportunities of building and owning housing in Saint Paul.

Explore the Saint Paul Housing Dashboard

Our latest interactive tool is designed to equip stakeholders with data-informed insights about housing dynamics in Saint Paul. Launch the tool

The Saint Paul Housing Dashboard and our qualitative conversations with housing owners and developers further the Minneapolis Fed Community Development and Engagement team’s understanding of how housing supply affects housing affordability. As such, this analysis supports our team’s mission to advance the economic well-being of low- to moderate-income individuals, households, and communities. The better we understand local housing markets that have seen recent policy changes—like Saint Paul—the better we can pursue the Minneapolis Fed’s overall mission to pursue a growing economy and stable financial system that work for all of us.

Saint Paul allows more missing middle housing

“Missing middle” housing describes housing options that fall in a range between single-family detached homes and large apartment buildings. Typical missing middle housing types such as duplexes, triplexes, and fourplexes were a core part of urban development through the first half of the twentieth century. As Saint Paul and other cities adopted more restrictive zoning that limited new development on the vast majority of residential lots to single-family detached units, missing middle housing went missing.

Recognizing a desire for a broader array of allowable housing types, Saint Paul explored its options by pursuing an analysis known as the 1-4 Unit Housing Study. The city subsequently amended its zoning code in 2023 to create two new zoning districts, H1 and H2, replacing its previous residential zoning districts. The H1 zoning district, which includes most city land, allows up to four principal units on each lot within development standards. The H2 zoning district, intended for neighborhood nodes and areas with high-frequency transit service, allows up to five units. As an incentive for developments that either add affordable units or add homes with three or more bedrooms, both zoning districts allow each lot to add one additional unit. As a result, property owners can potentially build fiveplexes or sixplexes on nearly all of Saint Paul’s residential land.

While development markets are still adjusting to the broader allowable options, production of missing middle housing has increased. In 2024, Saint Paul permitted 76 units in two-, three-, or four-unit buildings, which was 18 percent of all permitted units.1 This one-year total of permitting is equivalent to the number of units in duplexes, triplexes, and fourplexes permitted over the previous 10 years. While the number of permits for units in duplexes, triplexes, and fourplexes declined to 47 in 2025, their share of all permitted units stayed roughly the same, at 13 percent. As a comparison, from the adoption of its 2040 Plan in 2019 through the end of 2025, Minneapolis permitted 362 units in two-, three-, or four-unit buildings. This represents 2 percent of all permitted units in Minneapolis from 2019 through 2025.

Multifamily housing production has felt a chill

Over the last decade, the Twin Cities metro area has seen a significant amount of permitting and construction of multifamily housing. While multifamily housing—buildings with at least five units—can be either apartments (rentals) or condominiums (owner-occupied), few condominiums are being developed anywhere in the Twin Cities metro. This trend of more apartment construction began as rental housing was the first market segment to recover coming out of the Great Recession. Apartment construction further accelerated to support transit expansion with the opening of a new light rail line connecting Minneapolis and Saint Paul in 2014.

Saint Paul saw peak years of housing construction—with 96 percent of it in the form of multifamily buildings—in 2019–2021. In both 2020 and 2021, the city permitted more than 2,000 new housing units, the most in any year since 1970. Though just over half of 2021’s total, 2022’s 1,169 units permitted still represents one of Saint Paul’s 10 highest production years over the last five decades. Building permits ticked up to 1,204 in 2023, then plunged to 404 in 2024 and 357 in 2025.

In November 2021, Saint Paul voters approved a rent-stabilization ordinance that limited property owners to 3 percent rent increases annually. The city implemented the ordinance in May 2022 and amended it in January 2023 to add vacancy decontrol (a measure allowing owners to increase rents after a just-cause vacancy); exempt income- or rent-restricted affordable housing from rent stabilization; and exempt new construction, including buildings built within the last 20 years, for 20 years. In May 2025, the city further amended the ordinance to permanently exempt all new construction.

Our conversations with the owners and developers of multifamily housing in Saint Paul identified an array of headwinds that challenge new multifamily construction. The most commonly cited was an inability to access capital to support new development. Investors have been skittish to lend money or provide capital in Saint Paul in the aftermath of the 2021 rent-stabilization referendum. One owner told us that the rent-stabilization policy has had “a profound effect on capital flows to this market.” Another described rent stabilization as having had a “chilling effect” on Saint Paul’s development.

Development of new market-rate rental housing in Saint Paul slowed after the rent-stabilization measure passed. According to the Metropolitan Council, the Minneapolis-Saint Paul area’s metropolitan planning organization, more than four in five new rental units in Saint Paul had been market-rate in 2020 and 2021. In 2022, market-rate housing dropped to less than half of new rental housing.

While we don’t have hard data about what caused this drop, the property owners and developers we interviewed feel that rent stabilization has had a profound effect on the market. One property owner told us that it “feels like Saint Paul has gone back to being sleepy. Development is not as dynamic as it was before rent control.”

In one example interviewees cited, after the adoption of rent stabilization the developers of a large market-rate apartment building in Highland Bridge, a 135-acre mixed-use redevelopment on the former site of a shuttered Ford assembly plant, suspended construction for several years. Without the tax revenue from this project, there was no additional increment of property tax revenue to support tax increment financing (TIF). And without the revenue from TIF, affordable housing construction in Highland Bridge also stalled. After 2025’s amendments that exempt new construction from rent stabilization, housing developers are, as one interviewee told us, “reengaging at the site.”

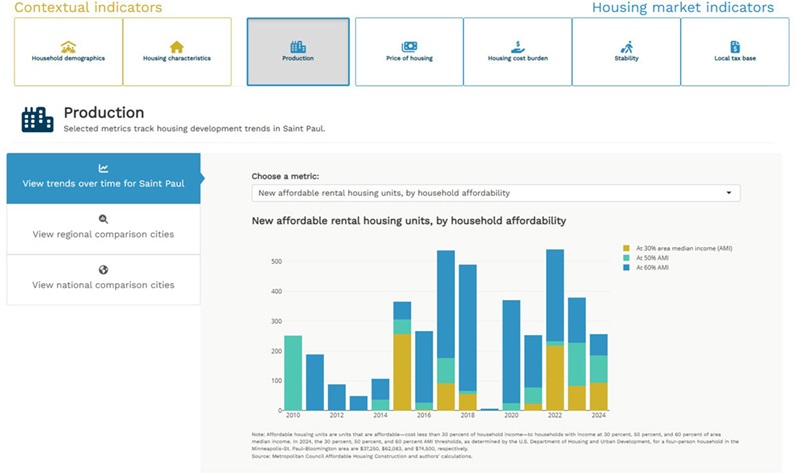

Forty percent of Saint Paul’s new rental development over 2022–2024 has been publicly subsidized affordable housing. Although affordable housing tends to attract different investors and capital sources than market-rate development, these investors have also been somewhat reluctant to invest in apartment development in Saint Paul. One affordable housing developer said they were “struggling to get a Low Income Housing Tax Credit investor because syndicators are not interested in Minneapolis and Saint Paul.”2 This interviewee believes that syndicators, investors who purchase the tax credits, are “turned off by rent control and uncertainty over local governance and policies.” On the other hand, another affordable housing developer told us that if the structure and underwriting are right, “[tax credit] investors will come to Saint Paul.”

One owner told us about a broker trying to sell an existing apartment building in a suburban city outside of Saint Paul. An investor from outside the region asked if the building was subject to rent control. The owner told us that rent stabilization “is having an effect on housing in this region. If anyone thinks that it’s not, they are in denial or deluding themselves.”

Owners of rental housing face operating challenges

As we’ve seen with the apartment sector more broadly in Minnesota, owners of multifamily rental housing in Saint Paul are struggling. Several owners and managers, particularly those with properties in downtown Saint Paul, mentioned that full-time security guards have become a necessary operating expense. As a result, one observed that “our actual operating results are different than the original underwriting.” Operating costs are up while rent revenues remain flat, a metro-wide trend. Others said security concerns are a driver of increased vacancy rates. The vacancy rate in downtown Saint Paul peaked in 2020 at 13.5 percent and has fallen since, to 9 percent in 2025.

The rent-stabilization ordinance, which applies to at least three out of four of the city’s 60,000 rental units, creates additional layers of complexity. Under the ordinance, owners who wish to increase rents above 3 percent to cover the cost of improvements to their building must submit a request for an exemption that documents both the expenses and the impact on net operating costs.

Owners of rental housing expressed frustration about this process. One noted that their financial challenges “would need to be catastrophic before going to the rent control board” because they don’t want to make their operating costs public. Another owner shared frustration about the city’s relative lack of capacity—both in number of staff and their real estate experience—in reviewing exemption requests. They commented that the city’s formula for adjusting rents due to property investment “is totally inadequate and makes no sense at all.” According to this owner, the calculations do not maintain a reasonable rate of return on capital investment.

Additionally, outside of the exemptions mentioned above, property owners can raise rents more than 3 percent if they document a “just-cause” vacancy—in other words, if they identify the reason for not renewing a renter’s lease. Property owners must prove to the city that they did not force out the previous renter just to increase rents. When applications are approved, property owners may increase rents by the cost of inflation plus 8 percent over the rent charged in the previous occupant’s lease.

An interviewee told us that property owners documented fewer than 900 “just-cause” vacancies in 2024. In the same year, roughly one in three units experienced turnover, suggesting that more than 18,000 renting households moved out of rental units. This suggests that property owners are documenting only a fraction of vacancies. Without documenting vacancies, property owners can raise rents by no more than the 3 percent limit. One property owner told us that owners would prefer to simply raise rents by 3 percent because they “don’t want to talk to the city.” By opting not to adjust rents when vacancies occur, property owners are beginning to charge varying rents for identical units in their apartment buildings.

One apartment owner told us that increases in property taxes and property insurance are driving up costs by an average of $30 per unit per month, making it “hard to keep [rents] affordable.” Between aging properties, rising property taxes, and constrained rents, another owner told us, “We don’t feel that Saint Paul is a good place to do multifamily business.”

Realities in apartment markets edge up homeowner property taxes

Housing, whether owner-occupied or rented, both provides homes for residents and is a major source of revenue for local governments. In Saint Paul, housing is 71 percent of the total property tax base.3

With operating costs rising and rent increases constrained, the per-unit sales price of apartments has fallen. The median sales price for an apartment unit in Saint Paul peaked in 2020 at $160,525 (inflation-adjusted to 2025 dollars). By 2025, it was $103,249, a drop of 36 percent. While the impact of reduced prices is not consistently showing up in lower property tax assessments, the lowered valuations reduce property owners’ ability to refinance their properties, particularly in an elevated interest rate environment, and therefore lessen the amount of cash available to invest in property maintenance and improvements. One owner, expressing concern about the market effects that aging buildings could have on neighboring properties, wondered, “What happens with the deterioration of older properties around new development?”

Across all apartments, the median market value, determined by the Ramsey County Assessor’s Office, edged downward 12.9 percent from 2020 to 2025, from $121,547 to $105,875. In other words, despite the higher values of any new construction, the falling prices of existing units have dragged the median down. Moreover, many owners of apartment buildings have told us that they are actively appealing their property tax assessments because of their buildings’ falling sales prices.

Adjusted for inflation, the owners of multifamily apartment buildings in aggregate paid 27 percent less property taxes in 2025 than in the peak year of 2022, down from $141 million to $103 million. The median annual property tax paid per rental unit has dropped from an inflation-adjusted peak of $2,825 in 2020 to $1,958 in 2025. With lower market valuation for multifamily properties, homeowners are paying a larger share of the property tax levy. Over the same time period, the annual property tax on the median-priced single-family home in Saint Paul increased from $3,442 to $4,264.

With weakness in the commercial tax base in downtown Saint Paul, owners of multifamily housing are concerned about future increases in property taxes paid by both homeowners and other residential property owners. One owner observed, “With the tax base in downtown collapsing, we’re expecting diminished services and rising property taxes on other [property] classes. That’s what will really kill us.”

Rents in Saint Paul are stable to falling

Apartment owners and managers shared a range of interpretations about what’s happening with rents in the city. Several believe that rents are increasing more than they would in an unconstrained environment as owners max out the increases to the 3 percent allowed. Others believe that rents are flat. One owner has observed changes in their renter demographics as “Baby Boomers are downsizing into Class A rentals4 and younger people are not buying homes.”

The data show that after adjusting for inflation, typical rents in Saint Paul are actually falling. Zillow’s Observed Rent Index peaked in October 2020 at $1,618 (in 2026 dollars) and fell 10 percent, to $1,456, by March 2026. From 2010 (our earliest year of neighborhood data) to 2025 in 11 of Saint Paul’s 17 neighborhoods, inflation-adjusted market asking rents for two-bedroom units were affordable to households earning 60 percent of the metro area median income. In the most recent data, rents in all 17 Saint Paul neighborhoods fall below that affordability threshold.

While renters benefit from Saint Paul’s lower rents, the lack of “rent lift”—or future rent increases—makes it harder for expected revenues from new market-rate apartment development to exceed development costs. As one interviewee noted, to get more housing, developers want “to know that new [housing] units will absorb at a typical or reasonably typical pace.”

Within these ebbs and flows of supply and price changes, housing affordability in Saint Paul isn’t worsening overall. The share of renter households experiencing housing-cost burden, or paying more than 30 percent of their income on housing costs, has been relatively stable for the last decade, with annual fluctuations between a low of 44.0 percent in 2021 and a high of 50.5 percent in 2022. But renter households with incomes between $35,000 and $49,999 saw their rates of housing-cost burden grow from 19.7 percent in 2010 to 81.5 percent in 2022 before moderating to 67.7 percent in 2024. (Note, however, that the income range of $35,000–$49,999 in 2010 dollars adjusts to $50,350–$71,927 in 2024 dollars.) The share of homeowners experiencing housing-cost burden is edging upward more steadily, from 18.8 percent in 2018 to 25.3 percent in 2024.

Looking ahead

Our interviews happened both before and after the most recent amendments to Saint Paul’s rent-stabilization ordinance were adopted and before the election of Saint Paul’s current mayor. When we spoke with them, some of our interviewees were brutally honest in their assessments of the city’s housing environment. One noted, “Saint Paul now has a reputation as a place that does not want more housing.” Another lamented that there is “no magical switch to save Saint Paul from itself.” However, we also heard a yearning from developers for the city to figure out how to incent development by addressing efficiency and certainty through process improvements and financial assistance that make housing construction more feasible.

Since our interviews, however, multifamily development has restarted in Highland Bridge.

A few other projects, both market-rate and affordable, are advancing. Saint Paul’s relatively affordable rents benefit residents. A developer told us that “Saint Paul feels like it’s within one to three years of having so much momentum, restoring the city’s great energy and fully reaching its potential.” As Saint Paul’s housing market continues to evolve, the Minneapolis Fed’s Saint Paul Housing Dashboard will continue to monitor its evolution.

Endnotes

1 Note that the permits data listed in this article and those used in our dashboard are from the U.S. Census Bureau Building Permits Survey and differ from permits data collected by the Metropolitan Council.

2 The Low-Income Housing Tax Credit program is the federal government’s largest tool providing financial assistance for the development and preservation of affordable rental housing. Under the program, syndicators purchase the 10 years of tax credits associated with a development in exchange for the upfront equity needed for construction costs.

3 Based on authors’ calculations of data from the Minnesota Department of Revenue’s Property Tax History Data page.

4 Class A properties are new or newly renovated apartments that feature prime amenities, attract high-income renters, and command the highest rents.

Libby Starling is Senior Community Development Advisor in Community Development and Engagement at the Federal Reserve Bank of Minneapolis. She focuses on deepening the Bank’s understanding of housing affordability, concentrating on effective housing policies and practices that make a difference for low- and moderate-income families in the Ninth Federal Reserve District.

Maxine Xu is a data scientist in the Minneapolis Fed’s Community Development and Engagement division, where she develops data tools and leads analyses to explore issues affecting the economic well-being of low- to moderate-income communities.