Author

Many fundamental risks shape expected returns for investors. What factors might affect the performance of a corporate stock, the price of a commodity, or the default of a bond? Professional or institutional investors also weigh another distinct form of risk when optimizing their portfolio: liquidity risk. When a trade settles, will the investor have enough cash on hand? If not, how costly will it be to borrow on short notice? What if they wind up holding too much cash that could have been earning better returns elsewhere?

In asset prices, these liquidity risks (also referred to as settlement risks) emerge as a “convenience yield” on liquid assets, such as Treasury securities, reserves at a central bank, or highly liquid private securities like commercial paper. All else equal, these assets should provide a lower return that reflects their value as liquidity (that is, more liquid assets have higher convenience yields). It seems intuitive that convenience yields would also depend on portfolio composition and changing market conditions. Yet they are traditionally imposed as a fixed, exogenous factor in economic models of asset pricing—including models that help estimate the effects of monetary policy changes.

To remedy this deficiency in modeling, Minneapolis Fed Monetary Advisor Javier Bianchi and UCLA’s Saki Bigio have developed a theoretical framework for how convenience yields arise endogenously (Working Paper 812, “Portfolio Choice and Settlement Frictions: A Theory of Endogenous Convenience Yields”). While the inherent liquidity qualities of assets naturally play a role in determining convenience yields, Bianchi and Bigio further quantify the important role of frictions in the over-the-counter (OTC) market, where investors strike deals with each other to lend or borrow short-term cash. They then propose how key parameters of their model might be identified from observable financial market data, yielding a tractable approach for economic modeling.

The new paper provides a broader theoretical foundation for the economists’ earlier work, published in Econometrica in 2022, exploring how endogenous convenience yields affect the transmission of monetary policy through the banking system.

In the first stage of a two-stage model, investors choose a portfolio of assets and liabilities with varying expected returns and liquidity/settlement risk. In the second stage, the investors experience a shock to their cash flow. This shock could be positive, such as an unexpected repayment of a loan, or negative, such as a bank experiencing a sudden withdrawal of deposits or an investor facing a margin call.

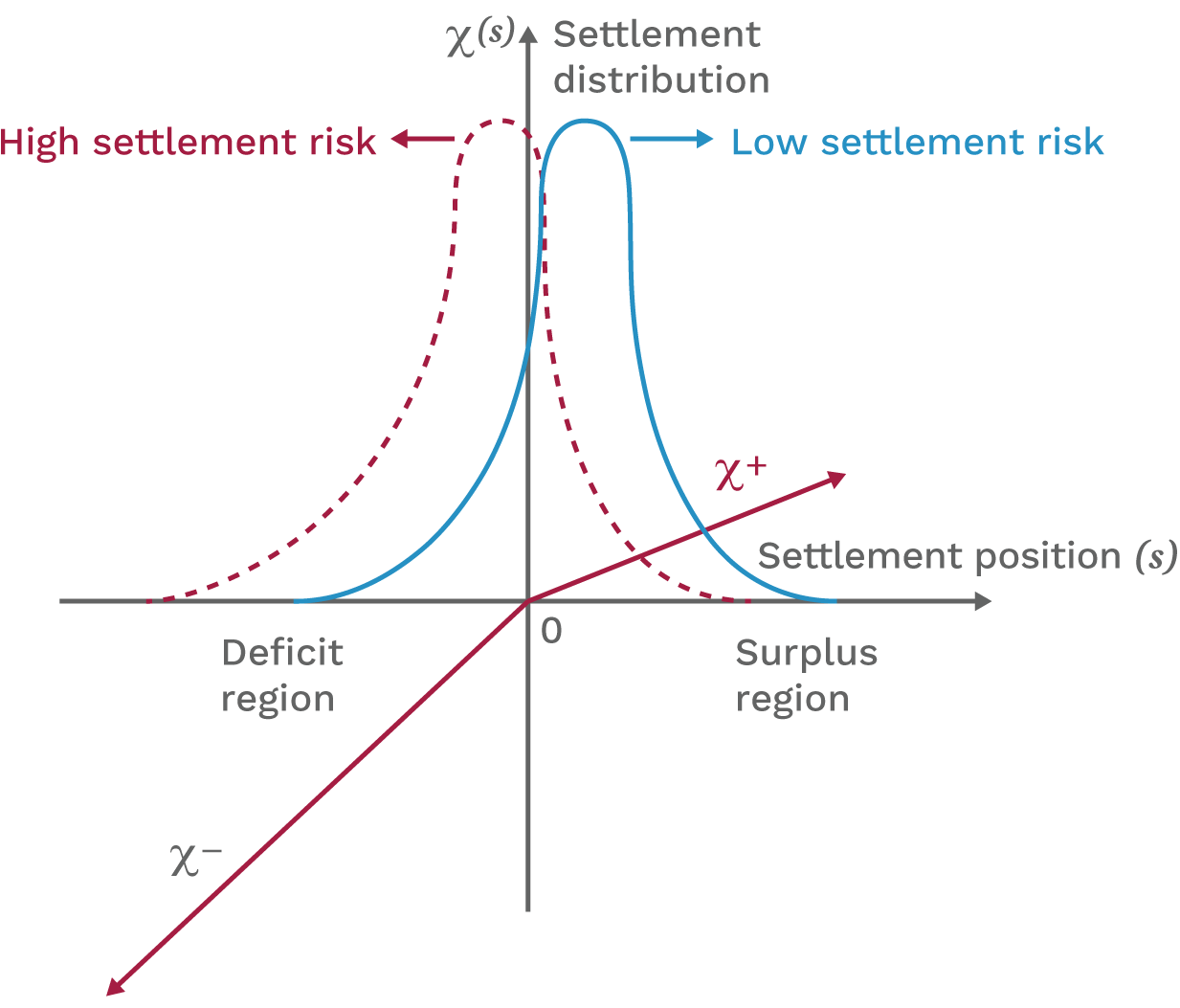

Investors who need cash to settle their positions can trade in the OTC market, over multiple rounds, with investors who have surplus cash to lend. OTC market “tightness” is the crucial variable in this setting. It is determined by the ratio of negative-to-positive cash positions and also reflects frictional factors, such as matching efficiency and the bargaining power of borrowers. It determines the shape of the convenience yield function.

Importantly, the proposed convenience yield function is non-monotonic: It is kinked at zero, reflecting that the interest rates charged to borrowers with negative cash positions rise more steeply than the returns available to investors with cash to lend (see figure).

Source: Bianchi and Bigio, “Portfolio Choice and Settlement Frictions: A Theory of Endogenous Convenience Yields,” November 2025.

The economists observe that this asymmetry leads otherwise risk-neutral investors to behave in a risk-averse manner, since the penalty for coming up short on liquidity is higher than the return for having surplus cash at settlement. It follows from this asymmetry that assets with more unpredictable settlement needs will require a higher convenience yield.

Bianchi and Bigio note that the fundamental risk of an asset can be correlated with its liquidity risk. (An economic downturn can simultaneously mean worse asset returns and greater risk in accessing liquidity for settlement.) The potential for these covarying risks makes investors even more risk averse in their portfolios, further pushing up convenience yields.

The framework also reveals the circumstances when the liquidity preferences of individual investors will not result in the socially optimal outcome. In tight OTC markets—negative cash positions outweigh positive ones—individual investors do not internalize the social value of accumulating more liquid assets, which would reduce settlement frictions for all. Individuals underinvest in liquidity, from a social planner’s perspective. This externality becomes more severe when society is more risk averse. In loose markets, on the other hand, investors will overinvest in liquidity, sacrificing returns.

Modeling the microfoundations of convenience yields could be valuable to a regulator like the Fed that is concerned with liquidity conditions in financial markets. Bianchi and Bigio propose that observable financial data, such as trading volumes and interest rates in the interbank OTC funding market, could be applied to estimate the parameters needed to solve their closed-form expressions. If so, their theoretical framework could become a practical tool leading to more informed monitoring of markets and smarter policy—including a better understanding of the downstream effects of quantitative easing and quantitative tightening.

Read the Minneapolis Fed working paper: “Portfolio Choice and Settlement Frictions: A Theory of Endogenous Convenience Yields”

Jeff Horwich is the senior economics writer for the Minneapolis Fed. He has been an economic journalist with public radio, commissioned examiner for the Consumer Financial Protection Bureau, and director of policy and communications for the Minneapolis Public Housing Authority. He received his master’s degree in applied economics from the University of Minnesota.