Authors

Richard Liu

Research Associate, Institute

The first two statistics in the Census Bureau’s annual Income in the United States report are median household income and its change from the previous year. Every three years, when the Federal Reserve releases the Survey of Consumer Finances, the first summary bullet point reports how much median family income has grown. When organizations like the Pew Research Center discuss topics such as the “hollowing out of the American middle class,” they define these groups based on the national median household income.

But what does “real median household income” mean? For example, which Americans benefit when median household income rises? If households do better, do people do better?

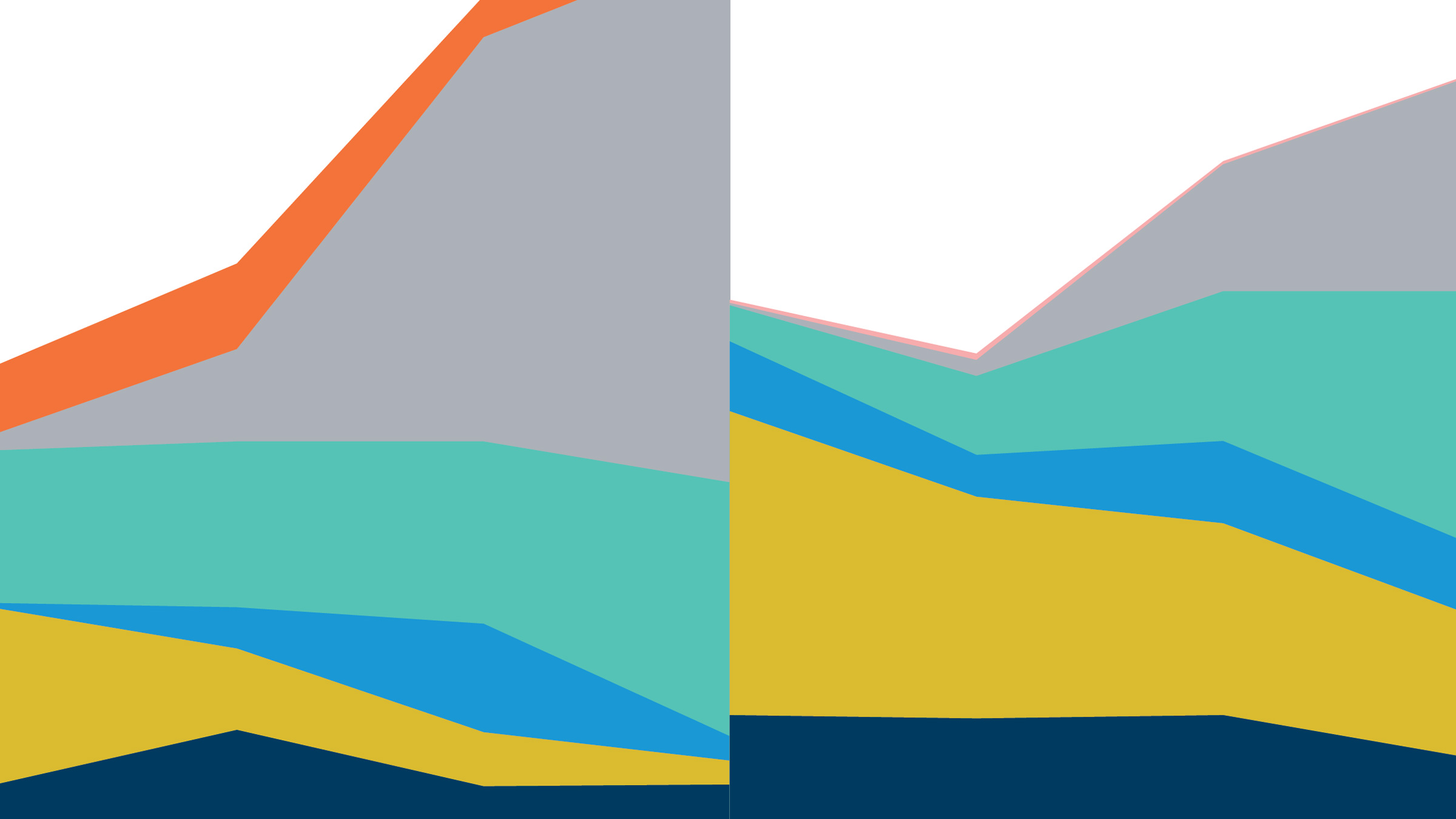

The figure plots real median household income from the Current Population Survey starting in 1947 and running through 2024. One clear takeaway is that median household income has grown tremendously—more than double—since 1947. Yet there are also periods of stagnation and, especially around large recessions such as in 1981 and 2008, times when median household income fell.

While economic analyses of the income distribution can be complex, understanding what real median household income means and, perhaps more importantly, what it does not mean, requires just a few simple concepts. In this piece we break down the nuances of this pivotal and common measure.

First, the “real” part. Income grows, especially over long periods, partly because prices change. But a higher income can’t actually buy any more goods or services if they have also become more expensive. In the 1970s, for example, reported median income rose by 103 percent, but prices rose by 112 percent. Income statistics have to adjust for this, and the data in the figure do: They reflect the value of a dollar in 2024, factoring in inflation.

Second, the word “household” plays a central role in shaping the trends we see. For statistical agencies, a household is a group of people who live together and share expenses, like a family or roommates. Household income equals the income earned by all household members. Therefore, median household income reflects not only how much each person earns but also how many earners each household has. When a household breaks up, for instance because of a divorce, one higher-income household becomes two lower-income households, which can lower median household income.

Changes in households have a huge effect on the trends in the figure between the 1970s and 1990s, when the share of new parents living together dwindled and divorces increased. The share of people ages 25–34 in households that contained just one adult rose from 8 percent in 1970 to 15 percent in 1990. This change meant more households with fewer earners and thus lower median household income. Median household income still provides a useful measure of economic well-being, since households, by definition, share resources and a household with fewer earners has fewer resources. As an indication of how much people can earn, however, median household income cannot say that much.

We can also combine data on changes to household structure and the income of different kinds of households to measure approximately how much change in median income came from shifts in household size versus shifts in income. For example, between 1970 and 1990, real median household income barely changed, but it grew by $8,493 for one-adult households and $9,010 for households with multiple adults. How can that be? It’s largely because the share of one-adult households doubled. Had the share of one-adult households remained steady at its 1970 level, real median household income may have increased by as much as $8,968.

On the other hand, had the range of real incomes among one- and multi-adult households stayed as they were in 1970, the shift in household size would have led to a reduction in overall median income of several thousand dollars. (Decomposing income changes into a within-group component and a compositional component works exactly for averages but is only an approximation for medians.) Therefore, even though incomes for each type of household grew fairly strongly during these 20 years, the composition of households offset that. Stagnant median household income in the latter 20th century is partly an artifact of the rise of one-adult households.

Next comes the meaning of “median.” Median household income is the level of income that divides households in half: Half of households have more income and half have less. But this means that changes in income among households in the bottom or top halves of the distribution do not affect the median at all. A recession that causes unemployment primarily among workers in low-income households might leave median income largely unchanged, even though it clearly has large effects on economic well-being. In fact, this is almost exactly what happened to hourly wages in the 1970s and 1980s.

Economists who have looked closely at median wages (including Juhn, Murphy, and Pierce in 1993; Autor, Katz, and Kearney in 2008; and Lemieux in 2010) have found that while the median wage dropped just slightly from the early 1970s to the late 1980s, wages at the bottom of the distribution fell much more. The result: a sharp rise in income inequality on top of roughly flat median household income.

Therefore, median income only really reflects how households in the middle are doing, and this provides one reason to look beyond the median. One in four households make less than the 25th percentile of income, for example, so this statistic is more relevant than the median for measuring the resources of lower-income households. At the other end of the distribution, economic inequality is often summarized by the 99th percentile (or higher), the minimum income earned by the richest 1 percent of households.

It can be hard to get enough data to paint an accurate picture of these extremes, however. The Institute’s Income Distributions and Dynamics in America resource, which calculates these kinds of statistics using millions of data points from U.S. tax records, provides one easy-access way to do so. Changes in median income will tend to reflect the experience of a broad group of households when all the percentiles are moving together, but not when incomes at the top or the bottom of the distribution are behaving differently.

Finally, one must understand what counts as “income.” Most American households get their income from wage and salary earnings, but not everyone. The feature article in this issue looks at nonwage income, who gets it, and how much they get. Trends in real median household income therefore come not only from changes in the labor market but also income support programs, financial markets, and even real estate markets.

In September 2026, the Census Bureau will report how much real median household income changed from its 2024 level of $83,730. What that says about economic well-being in America depends on much more than just one number.

This article is featured in the Spring 2026 issue of For All, the magazine of the Opportunity & Inclusive Growth Institute