Author

With the turmoil that pervades Latin America these days—from Fidel Castro's uncertain health to the contested election in Mexico to socialist fervor in Venezuela and elsewhere—there can be little question that economics, as well as politics, is on the minds of many south of the U.S. border.

Low standards of living are the norm in Latin America, but the causes of economic adversity are less than clear. Some have suggested that culture is the cause, that Latin Americans place less emphasis on economic progress than their neighbors to the north. Others propose that macroeconomic mismanagement is at the root of underdevelopment.

"Latin America is always in the news," notes economist Lee Ohanian, a Minneapolis Fed consultant, commenting on this macro management focus. "[It's] almost always about monetary issues—exchange rate stabilization plans, anti-inflationary plans, et cetera." But economists generally agree that such factors have short-lived effects. "The shocking aspect of Latin America," says Ohanian, "is that they should not be worried about 'fine-tuning' the business cycle. They should be worried about why their basic level of income is so abysmally low."

In a paper published last year in the Journal of Monetary Economics,* and reprinted in the Minneapolis Fed's September 2006 Quarterly Review, four economists—including Ohanian—have taken a comprehensive look at Latin America over the past 50 years, trying to understand this puzzle: Why have so many nations in this one part of the world made so little economic progress relative to other countries? And their definitive conclusion is that productivity has stagnated in Latin America.

But, of course, that prompts another question: What accounts for the productivity stagnation? Here the economists' answer is more tentative, but equally intriguing: Latin American productivity has remained at a standstill for half a century because of barriers to competition. That is, Latin American countries have erected obstacles—political, institutional and economic—that prevent competitive forces from unleashing greater efficiency in how firms use resources: higher productivity.

Stagnant among peers

The economists, Harold Cole of the University of California, Los Angeles; Lee Ohanian, also of UCLA; Alvaro Riascos of Banco de La República de Colombia; and James Schmitz of the Minneapolis Fed, make their argument powerfully—with a methodical, step-by-step logic that begins with careful documentation of what they term "Latin America's persistent economic stagnation."

Calling an economy "stagnant" implies a comparison: stagnant relative to what? The paper's framework uses a peer group of nations, those the economists suggest are "similar to Latin America in their ability to adopt and learn new technologies and ... similar in their preferences for market goods." Because Latin America is significantly populated by individuals of European descent, they define the peer group as European nations and other countries with significant European populations "in which European religion, language, and culture have been dominantly established."

In a sense, this choice of peer nations holds culture as a constant, eliminating it from the list of possible explanations for economic stagnation. If culturally similar nations display dissimilar economic progress, the cause of economic disparities clearly can't be culture. Instead, the differences must be due to what the economists call "idiosyncratic Latin American choices that differentially affect either the efficiency of production or the employment of the factors of production or both."

The peer group, then, is a set of 22 countries—18 of them in Europe, plus Australia, Canada, New Zealand and the United States. A dozen Latin American nations are included in the study—11 from South and Central America, plus Mexico. The economists present data demonstrating the extent of European influence in Latin America. As an average across the 12 nations, 94 percent of the population speak a Western European language, 89 percent are affiliated with Western religions such as Christianity or Judaism and 84 percent are white or mixed-white racially.

So, how do these culturally similar nations compare from an economic standpoint? All 12 Latin American nations are poorer, in terms of gross domestic product per capita, than their 22 peers (see figure 1). Only two of the Latin American nations (Chile and Argentina) had per capita GDP greater than 30 percent of the United States figure, while the entire peer group was at more than 40 percent of the U.S. standard.

Figure 1

Note: Figures 1-6 are from the Journal of Monetary Economics, January 2005.

A growing gap

Trends from 1950 to 2000 show, moreover, that this relative income gap has grown over time, with the average Latin American nation falling from 28 percent of U.S. per capita GDP in 1950 to 22 percent in 2000, while the average European country rose from 40 percent in 1950 to 67 percent of U.S. per capita GDP by 2000. In other words, "all the other poor Western countries have had significant catch-up over the last 50 years ... [while] Latin America lost ground" (see figure 2).

Figure 2

The economists gather similar data for several East Asian countries with per capita income in 1950 similar to or below the Latin American level. These seven countries, like the European peer group, had significant catch-up to the United States, rising from 16 percent of U.S. per capita income in 1950 to 57 percent in 2000.

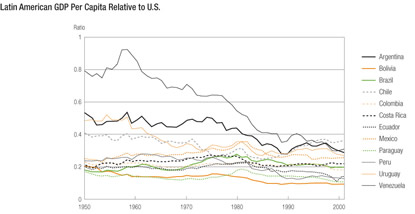

They also find that while there was significant variation among the Latin American dozen in their relative income trends over the half-century (Venezuela dropped from 78 percent of U.S. income to 30 percent, for instance, while Costa Rica was fairly constant at about one-fifth of U.S. income), "not a single Latin American country has had any significant catch-up" to the United States (see figure 3).

Figure 3

And they also point out that Latin American stagnation relative to the United States isn't just a recent phenomenon. Available data on 10 of the 12 nations show an average relative per capita GDP of 29 percent in 1900, slightly higher than the 22 percent figure in 2001—in other words, Latin America actually declined relative to the United States over the past century. Estimates of relative incomes in 1800 suggest, in fact, that Argentina was richer than the United States two centuries ago and that the income gaps with Brazil, Chile, Mexico and Peru were smaller then than they are today.

This stagnation is perplexing, say the economists, when compared to Africa and the Middle East, two other regions that have suffered economic stagnation relative to the United States over the past 50 years. Stagnation in Africa and the Middle East can be explained—at least in part—by AIDS, substantial civil conflict, ethnic cleansing and extremely repressive, nondemocratic institutions. "These development impediments are not nearly as severe in Latin America," they write. "We focus on Latin America because we view it as the most puzzling regional development failure of the last 50 years."

Eliminating suspects

They then set about solving the puzzle, quickly eliminating several possible suspects: low employment, low capital stock and low human capital.

To analyze the problem, they use a standard economists' tool, a growth model, which understands economic output as the result of factors of production. Initially, such growth models focused on labor and capital as the factors that could explain high or low economic output.

But in articles published in the 1950s, Nobel Laureate Robert Solow of the Massachusetts Institute of Technology demonstrated that the doubling of U.S. economic productivity—output per unit of labor—between 1909 to 1949 was due mostly to a third factor: "87 1/2 percent of the increase," he found, was "attributable to technical change."

Solow thus illustrated that economists hoping to understand the process of economic growth within a nation—or differences in growth among nations—should examine not only labor and capital, but also what Solow called "technical change." Economists now refer to it as the "Solow residual" or "total factor productivity."1

Still, a thorough study of the reasons for Latin America's stagnation calls for systematic examination of each factor: labor, capital and total factor productivity (TFP). If it's a matter of labor supply, say the economists, it makes sense to compare regional data on laborers per capita. Perhaps Latin American economies have been stagnant because a relatively small proportion of the population is employed.

But a quick comparison of employment rates by region demonstrates that labor supply is not the central explanation. On average, Latin America's employment rate is about 70 percent that of Europe's or the United States'—a gap, to be sure, but not large enough to account for the huge gap in per capita income. "This finding," conclude the economists, "implies that productivity is the key factor." In other words, the problem of low per capita output is not that too small a proportion of the population is working, but that each laborer produces too little.2

A graph of labor productivity rates relative to the United States from 1950 to 1998 confirms the implication. Latin American productivity was 33 percent of the U.S. level in 1950 and just 32 percent in 1998. But in Europe, productivity levels rose from 39 percent to 79 percent of U.S. rates over the same period. And in Asia, productivity soared from 19 percent to 54 percent. Indeed, a graph of relative productivity trends (see figure 4) is strikingly similar to the graph of relative income trends (see figure 2).

Figure 4

Decomposition

So, if the issue is labor productivity rather than employment rates, what accounts for differential productivity? The economists investigate by decomposing productivity a bit further. Latin American countries could have low productivity because their laborers have less physical capital to work with; fewer machines per laborer could explain lower output per labor unit.

The data on capital stocks, however, show that the capital-output ratio in Latin America has been within 10 percent of the U.S. ratio since the 1960s. And data on capital flows over time substantiate this: Capital investment-to-GDP ratios in the United States and Latin America have been very similar since the 1960s. Conclude the economists: "a capital shortfall is not the major factor retarding Latin America's productivity."

A quick bit of algebra3 shows that if capital-output ratios are similar in Latin America and the United States, but output per capita in Latin America is just one-fourth of the U.S. level, and employment per capita is three-fourths of the U.S. level, then Latin America's capital-labor ratio is one-third that of the U.S. level. And that in turn "implies that Latin American TFP is about one-half of the U.S. TFP level."

TFP, again, is shorthand for total factor productivity, described by the economists as "the efficiency with which an economy uses its capital and labor services." More broadly, it's understood as the portion of output growth that isn't accounted for by increases in quantities of either labor or capital (thus, Solow's "residual"). And if Latin American nations use their capital and labor with roughly half the efficiency of the United States (that is, if Latin America's TFP is half the United States' TFP), that would explain Latin America's relative stagnation.

Differences in TFP could be due to lower human capital. If workers in Latin America have less education or lower labor skills, they may produce less efficiently. But the economists find that human capital levels have climbed more rapidly in Latin America between 1960 and 1990 (19 percent) than in Europe (12 percent) and Asia (9 percent). "The fact that Latin America's relative output continues to decline, despite this significant increase in human capital, indicates that a different factor is driving down Latin American relative TFP and output," the economists conclude.

The remaining possibility

So, if it's not low employment, insufficient capital or inadequate human capital, what does explain Latin America's persistent pattern of stagnant per capita output? Having eliminated the usual suspects, the economists propose that Latin America's inefficiency likely is due to the systematic creation of barriers to competition. Without competition, producers have not had to seek out better technologies nor had an incentive to make efficient use of the technologies they do have.

The rest of their paper is devoted to an empirical survey of competitive barriers in Latin America and to reviewing evidence about what has happened to productivity in individual industries when those barriers were either created or eliminated.

Competitive barriers, they explain, can be categorized as international or domestic. International barriers include tariffs, quotas, multiple exchange rates and regulatory barriers to foreign producers. Domestic obstacles to competition include barriers to entry into an industry, inefficient financial systems and large state-owned enterprises. Latin American competitive barriers fall into both camps.

International and domestic barriers

Barriers to protect domestic industries have a long history in Latin America. Between 1870 and 1913, Latin American nations had average tariff levels of 27 percent, compared to an average level in Asia of 7 percent. And Latin American tariffs rose during the 20th century, especially after World War II. Nominal rates of protection in six Latin American nations in 1960 ranged from 22 percent to 172 percent, depending on the category of good, while similar rates in the European Economic Community averaged 11 percent.

Quotas were also widespread. In 1956, 28 percent of products were subject to quotas in Latin America; by 1974, the figure had climbed to 74 percent. Protectionism persisted until the early 1990s, write the economists, with average tariff rates in Latin America of about 38 percent (compared to 16 percent in East Asia), declining to 27 percent by the early 1990s.

High barriers to international competition were compounded (or complemented) by high domestic barriers, including high entry costs, excessive government intervention in capital markets and high costs of adjusting and building workforces. To document those costs, the economists compile data on business start-up costs, government ownership of large banks and mandated severance pay in the United States, Europe, Asia and Latin America.

They find that for each category, barriers to competition are highest in Latin America.

In Latin America, the total estimated cost in 1997 of starting a business was 80 percent of per capita GDP, compared to less than 2 percent in the United States, 24 percent in Asia and 36 percent in Europe. Government ownership of banks, considered an indicator of whether bank loans are directed toward politically connected businesses, is higher in Latin America than in the other regions. And Latin American nations impose higher job security costs than others, making it far more expensive for Latin American businesses to dismiss workers and reallocate labor from low to high productivity businesses. "In every case," the economists write, "Latin America has the highest barriers."

The impact of barriers

If these barriers truly do affect the wealth of nations, their creation or removal should have a measurable impact. In the rest of their paper, the economists review seven case studies from five Latin American countries: two instances in which barriers to competition were created through the nationalization of private, international firms and five cases in which policies that fostered competition were adopted. In all seven instances, the data confirm the theory that competitive barriers have a strong impact on economic output.

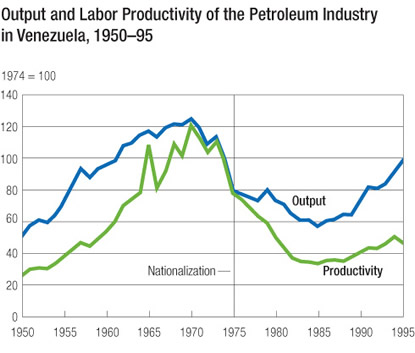

Venezuela is their showcase for anticompetitive policies. They draw on a 2004 study by Diego Restuccia and Schmitz, which examined the effect of that country's 1976 nationalization of both the oil and iron-ore industries. For both industries, the elimination of foreign competition had a serious negative effect on output and productivity. For the petroleum industry, for example, output and productivity had climbed at an annual rate of 4.5 percent and 7.5 percent, respectively, from 1950 to 1970. After nationalization, both output and productivity fell precipitously. By 1995, output had recovered somewhat, though never reaching pre-nationalization peak output, but productivity remained very low, at barely half its 1974 level (see figure 5).

Figure 5

Similar if less dramatic results were seen in the iron ore industry. Productivity and output climbed from the 1950s to the mid-1970s. After nationalization, both plunged to about 60 percent of their peak levels by the mid-1980s. The industry recovered somewhat, but never again achieved its peak 1974 levels.

Anchors away

And when barriers are removed? Here the authors examine five cases: reforming the copper industry in Chile, reversing quotas in Brazil's computer industry, privatizing the Brazilian state-owned iron ore industry and large-scale privatizing of state-owned enterprises in both Mexico and Argentina. In all cases, removal of barriers and creation of competition improved output and productivity.

The Chilean copper industry, which accounts for about 10 percent of Chile's GDP and one-third of its exports, provides a solid illustration. In 1971, the Chilean government nationalized and operated the country's largest copper mines, representing about 85 percent of production. "The key outcome of the nationalization is that [the government-owned copper enterprise] faced very little foreign or domestic competition," write the economists.

In 1990, a new government policy supported reforms in the copper industry, allowing entry by foreign firms. Productivity increased by 14 percent a year, compared to 3.5 percent annually before foreign competition was allowed, and after a decade of growth, total copper output had increased 175 percent.

The productivity rate of Chile's copper industry gained significantly on the U.S. copper industry after the introduction of competition. Before the government allowed foreign entrants, Chile's productivity declined from 41 percent of U.S. levels to 30 percent. "After the reform, Chilean productivity increased from 30 percent of the U.S. level to 82 percent of the U.S. level over a 10-year period" (see figure 6). The economists conclude: "pro-competition policy reforms that encouraged foreign competition significantly increased productivity ... by allowing high productivity producers to enter and by changing the incentives facing the incumbent producers."

Figure 6

Similar results obtained in the four other case studies reviewed by the economists. Eliminating competitive protection for Brazilian-owned computer firms in the early 1990s resulted in a large rise in domestic production, a dramatic productivity increase and much lower prices. Privatizing Brazil's state-owned iron ore industry in the early 1990s resulted in a 140 percent rise in productivity from 1990 and 1997 and a 30 percent increase in output.

Introducing competition works on a larger scale, as well, they find. Mexico's privatization of most of its state-owned enterprises from 1983 on led to large increases in productivity and output by removing impediments to entry by new firms. Argentina also privatized many of its SOEs in the 1990s; even though many of them maintained the monopoly structure they'd had as government-owned firms, productivity rose by 46 percent, on average, unit costs declined and production rose.

The common theme

"These seven cases have a common theme," conclude the economists. "[P]olicy changes that substantially affect the amount of competition faced by Latin American producers significantly and systematically change productivity. In particular, these cases suggest that Latin America indeed can achieve Western productivity levels when competitive barriers are removed."

It's a hopeful theme, lighting a possible path for reducing the gap between Latin American levels of per capita income and levels in other Western nations. But it raises another important question. "Understanding the reasons Latin America has set up so many competitive barriers is central," the economists write.

There are theories, of course. Some scholars suggest that economically powerful groups are able to create political and legal institutions that help maintain their economic advantage. "When a particular group is rich relative to others, this will increase its de facto political power and enable it to push for economic and political institutions favorable to its interests," write Daron Acemoglu, Simon Johnson and James Robinson in a 2004 paper. In Latin America, then, incumbent low-efficiency firms may be successful in lobbying their governments for laws that create barriers against efficient new competitors.

Cole, Ohanian, Riascos and Schmitz refer to these theories as "potentially interesting avenues," but they don't pursue them in this paper. Their work is focused instead on the impact of barriers, rather than the factors behind their creation or destruction. And they suggest that the key open question is whether increasing competition in other Latin American industries—besides those they've reviewed—would lead to similar gains in productivity and output.

It's a suggestion made with a measure of modesty. The question might remain open, but their work provides powerful evidence that whatever the industry, wherever the nation,4 destroying barriers to competition holds major promise for economic progress.

* "Latin America in the Rearview Mirror," Journal of Monetary Economics 52 (2005) 69-107.

Endnotes

1 Mathematically—feel free to skip this part—the growth model is represented in a deceptively simple formula: Output equals the amount of labor times the amount of capital times total factor productivity. Using the symbols Y for output, A for total factor productivity, K for capital and L for labor, and throwing in a couple of exponents to show the share of output represented by K and L, economists come up with the neoclassical growth model: Y = A * K 1/3 * L 2/3. Since economic growth is often analyzed on a per capita basis, the variables are usually divided by total population (N).

2 In the growth model's terms: Since Y/N = Y/L * L/N, the problem of low Y/N could be due to either low Y/L or low L/N (or both.) The data show that Latin America's somewhat lower L/N doesn't sufficiently explain the extremely low Y/N, implying that low Y/L (productivity) is the key factor.

3 In the growth model, K is capital, Y is output, L is labor and N is total population. Algebraically, K/Y * Y/N * N/L = K/L. If the values for the first three ratios are 1, 1/4 and 3/4, respectively, then multiplying them produces a capital-labor (K/L) ratio of 1/3.

4 In related work with José E. Galdón-Sánchez, Schmitz found that productivity increased in the iron ore industry in countries where the industry faced a significant increase in competitive pressure. In countries where the industry experienced little or no increase in competitive pressure, productivity increased very little. See "Mining for Missing Links," The Region, September 2003.