In their effort to accurately measure banks’ share of financial intermediation, John Boyd and Mark Gertler (BG) made two important but distinct adjustments to flow of funds data. The first accounted for off-balance-sheet activity. The second adjustment tried to account for the offshore activity of the U.S. operations of foreign banks. Here we discuss this distinct correction and present corrected flow of funds data for the post-BG period.

BG noted that when foreign banks operating in the United States make loans to U.S. customers, they sometimes report all or part of these U.S. loans in the accounts of their non-U.S. subsidiaries. Such seemingly odd “exporting” might have tax or regulatory benefits. Regardless of the reason for such accounting, it reduces the level of banking intermediation reported to occur in the United States.

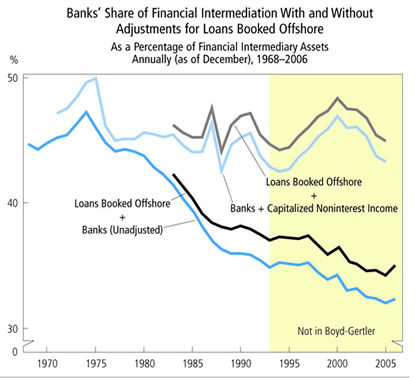

Sources: FDIC, Federal Reserve Board of Governors

To correct for this understatement, BG relied on Federal Reserve Bank of New York estimates of offshore lending by the U.S. operations of foreign banks. The New York Fed estimates, in turn, relied on data from the U.S. Treasury. BG added these estimates of offshore lending to the balance-sheet data already captured in the flow of funds plus their off-balance-sheet corrections. In BG’s analysis, the off-balance-sheet corrections generally led to the biggest adjustments to banks’ market share. That said, the offshore adjustments were more than trivial; they raised banking sector assets by roughly 10 percent at the end of BG’s sample period.1

We do not have access to similar Treasury data to adjust the flow of funds data, but we do not need to. As of March 1993, bank supervisors have required foreign banks with a U.S. presence to report information on offshore loans.2

In the accompanying chart, we present the offshore adjustments made by BG in the period they reviewed for both the unadjusted bank share and the share adjusted for capitalized noninterest income. We augment their data with similar adjustments for the more current period. As one might expect, these data increase bank market share for every year.

We note that while loans booked offshore continue to grow, their rate of growth has declined over time. In the 1983–92 period BG examined, such loans grew fivefold. Since then, they have only doubled. BG predicted such a turnabout. Changes to the regulatory regime and a reversing course in the trade deficit led them to surmise that “the foreign share of banking is likely to decline.” We do not investigate these potential causes.

1 John H. Boyd and Mark Gertler. 1994. "Are Banks Dead? Or Are the Reports Greatly Exaggerated?" Federal Reserve Bank of Minneapolis Quarterly Review 18 (Summer): 2–24, Table A2.

2 The report is formally called "FFIEC 002, Report of Assets and Liabilities of Non-U.S. Branches That Are Managed or Controlled by a U.S. Branch or Agency of a Foreign (Non-U.S.) Bank." Edward Ettin (“The Evolution of the North American Banking System,” 1994) also recommends that analysts use this series to account for offshore lending by the U.S. operations of foreign banks.

Return to: Are Banks Really Dying This Time?