Author

Dave Walter

Contributing Writer

The Ninth District is a leading producer of turkeys—roughly one of every five turkeys sold in the nation last year was raised in the region—and industry growth has been robust in recent years. District turkey farmers are raising more turkeys and producing more pounds of turkey meat for more value than ever before.

Close business relationships among hatcheries, growers and a handful of large processors have made the turkey industry one of the most efficient livestock industries. Raising large, quick-growing birds under contract for regional companies such as Jennie-O Turkey Store and Northern Pride Co-op has helped to keep retail prices low and expand production. “This is a good business to be in,” said David Muehler, a second-generation turkey grower who is president of the North Dakota Turkey Federation.

But the industry faces a grave problem today that is slicing into profits and threatens to stunt further growth: dramatically higher feed prices. A tripling over the past two years in the prices of corn and soybeans has made it more expensive to feed turkeys. Some observers believe that the industry is ripe for contraction, with fewer growers producing more expensive turkey.

More turkey with that stuffing?

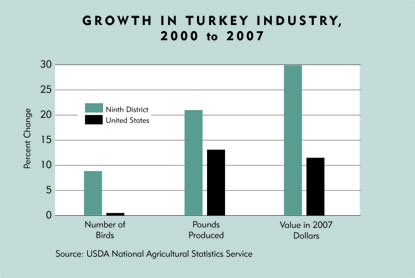

In recent years, chances have increased that this Thanksgiving a turkey gracing any given table in America hails from the district. By virtually every important measure—birds raised, pounds produced, total value—the district’s turkey industry is growing, and at a faster rate than the industry nationwide (see chart).

Last year, district turkey farms raised more than 54 million birds, one-fifth of the nation’s flock of 272 million birds. Much of the increase in the size of the region’s turkey flock has occurred since 2005 and stems from production gains in Minnesota, by far the district’s largest turkey producer.

The strong performance of turkey farmers in the district compares favorably with growth trends in other livestock industries. In the beef industry, cattle and calf production fell 3 percent between 2000 and 2007, and in dairy the number of milk cows raised decreased by 10 percent. Growth in the number of turkeys roughly matched the increase in chicken production, while in terms of pounds produced, the growth rate for turkey was more than twice that for chicken.

Only hog farmers have outdone turkey growers in production growth; between 2000 and 2007, the number of hogs raised in the district increased by about 23 percent. (However, those gains have not translated into higher income for hog farmers, because of dropping hog prices in the past two years.)

Gobbling Minnesotan

Minnesota has enjoyed national bragging rights in turkey production since 2003; the state raises more birds and produces more pounds of turkey meat than any other state. (North Carolina is the second-largest U.S. producer.) Last year, Minnesota raised 48 million turkeys, 8 percent more than the state produced in 2005. Those turkeys accounted for 89 percent of the birds produced in the district and contributed $555 million in market value to the economy.

Geography and history have made Minnesota tops in turkeys. Minnesota is corn and soybean country, so state growers benefit from low transportation costs for feed—unlike their counterparts in North Carolina, who pay more for feed shipped into the state. Minnesota’s temperate summers are also conducive to raising heat-averse turkeys, although barns must be heated in winter.

Minnesota’s natural advantages for raising turkeys attracted turkey processors to the state in the early 1940s, which in turn encouraged more turkey production. Many turkey farmers in the district are third- and fourth-generation growers with long-standing contractual ties to processors such as Jennie-O and the Turkey Store (the two merged in 2001). Minnesota growers have also benefited from pioneering research at the University of Minnesota’s veterinary school that has kept turkey diseases under control.

South Dakota and North Dakota run a distant second and third, respectively, in district turkey production. South Dakota farmers raised 4.5 million turkeys in 2007, while growers to the north produced 1.7 million birds. North Dakota’s production has rebounded from its low point of the decade in 2004, but last year it was still 11 percent below its 2000 level, likely due to general attrition among growers.

The northwestern counties of Wisconsin produce turkeys on a commercial level, but with just a few farms, data for Wisconsin are not reported. Montana and the Upper Peninsula of Michigan don’t raise turkeys commercially.

Growing ’em bigger and better

Since 2000, the amount of turkey meat produced in the district has increased at over twice the growth rate in the number of birds. Turkeys raised in the district, and in the nation, have grown bigger over the years, and they put on weight faster than in the past. In 1980, according to the U.S. Department of Agriculture (USDA), an average turkey weighed 18.5 pounds at slaughter; in 2004—the latest year for which figures are available—the typical mature turkey weighed 26.5 pounds.

Turkey farmers breed and feed today’s birds to grow bigger and quicker (adding as much as two pounds per week to their frames) than their recent ancestors. Careful breeding and nutrition have also produced turkeys of uniform size bearing lots of white breast meat—more desirable to consumers than dark meat.

The supersizing of the American turkey is one indication of how efficient the turkey industry has become at producing large quantities of turkey meat for consumption in the United States and overseas.

Large, uniformly sized turkeys lend themselves to large-scale, automated processing, reducing production costs. Economies of scale extend to turkey hatcheries and farms where turkey hatchlings (called poults) are raised to maturity. The size of turkey “grow-out” facilities in the district varies widely, said Steve Olson, executive director of the Minnesota Turkey Growers Association. But even relatively small farms house 10,000 birds or more, and larger operators raise as many as half a million turkeys at multiple sites.

Efficient production translates into low retail prices. Consumers pay much less per pound for turkey than other meats (see chart); in 2007, turkey sold for about half the price of ham and less than half the price of beef (chicken cost about the same). And the price of turkey keeps falling; adjusted for inflation, turkey costs less than it did in 1998. In contrast, the price of beef has risen 26 percent in real dollars over the past decade.

Affordability, together with the development of “further-processed” products such as turkey lunchmeat, sausages and ground meat, has made turkey more of a year-round food item than it was a generation ago. Per capita turkey consumption in the United States rose from 6.3 pounds in 1960 to just over 18 pounds in 1996, according to the USDA. In 2005, turkey consumption fell slightly to 16.7 pounds per person.

American consumers aren’t the only ones eating more turkey; between 1990 and 2007, U.S. exports of turkey meat increased almost eightfold to 554 million pounds. The three leading export countries for turkey are Mexico, China and Russia.

The corporate turkey

Tight coordination among hatcheries, turkey growers and processors promotes efficiency in the industry. A few large companies in the district—the survivors of decades of consolidation—control the various steps of turkey production by incorporating hatcheries, feed mills and processing plants within a single corporate entity. The output from one step becomes the input for the next, saving time and resources all the way down the supply chain.

“Everything works backwards from marketing,” with the number of turkeys to be raised annually planned a year in advance, said John Burkel, a fourth-generation turkey farmer and member of Northern Pride Co-op, a turkey processor in Thief River Falls, Minn.

Other livestock industries such as beef, swine and dairy are also vertically integrated, but none so thoroughly as poultry (chickens and turkeys).

Typically, independent growers raise turkeys to processing weight, but contractual relationships bind growers to a single processing company in the region. Contracts assure growers a nearby buyer for their product and guarantee processors a steady supply of birds of uniform quality and weight. Contract terms vary; often the processor agrees to provide poults and pay for feed, veterinary care, winter heating and the shipping of fully grown birds to slaughter.

Driven by competition to maximize efficiency by increasing the size of operations, the turkey industry has consolidated dramatically since the 1950s. In 1961, according to unpublished research at the University of Minnesota, 28 processors were operating in the state, down from 60 a decade earlier. Today, Minnesota has nine processing plants owned by just four companies. South Dakota and the district portion of Wisconsin have one turkey processing plant each.

The Jennie-O Turkey Store is by far the largest turkey processor in the district, owner of seven processing plants and a network of hatcheries, feed mills and corporate grow-out farms to keep the plants supplied with live turkeys. Jennie-O also buys from contract growers.

Comprehensive data aren’t available on the number of turkey farms in the district. But USDA Census of Agriculture statistics indicate that the ranks of turkey farmers have shrunk over the years even as production has soared. In 1959, 1,900 farms in Minnesota raised 13.1 million birds—an average of 7,000 turkeys per farm. In 2002—the latest Census year—there were 479 commercial farms in the state, producing on average 13 times as many birds per farm.

Eaten out of house and barn

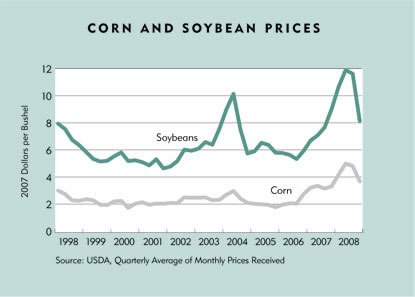

For all its efficiency, the turkey industry is suffering from escalating corn and soybean prices that have increased production costs (see chart). Feed accounts for about two-thirds of the cost of raising turkeys. In the summer of 2006, corn prices hovered around $2 per bushel; by last June, they had hit $5 per bushel. The trend for soybeans is similar: Between 2006 and last July, the price more than doubled to almost $12 per bushel. Since then, prices for both commodities have fallen considerably.

So far, processors have eaten the higher costs of feed. Contracts with growers usually stipulate that the processor pays for turkey rations—once a safe bet for processors because before the recent run-up, feed prices had been fairly stable for years. No more; processors are feeling the impact of rising feed prices, which doesn’t bode well for the industry as a whole. The rising price of feed “is first and foremost the thing we think about,” said Burkel of Northern Pride, which has to foot the bill under its contract obligations to member-growers.

Turkeys are extremely efficient at converting feed into meat; just under three pounds of feed are required to grow one pound of turkey—less than half the amount it takes to produce a pound of beef. Even so, processors can be expected to absorb high feed prices only so long before they’re obliged to pass those costs along to consumers or cut production.

The National Turkey Federation in Washington, D.C., has lobbied for a reduction in the federal ethanol mandate for blended gasoline, arguing that the upward pressure it puts on corn prices will ultimately increase turkey retail prices and force some turkey farmers out of business.

The impact of increased ethanol production on feed prices is debatable, but there are already signs of a shake-up in the industry. A Butterball turkey plant in Colorado announced this fall that it would close its slaughtering facility and local turkey raising operations by Thanksgiving, citing “record-high costs for corn, soybean meal and other feed ingredients” for the loss of almost 500 jobs.

Main dish or leftovers?

The district’s turkey industry has proven itself remarkably efficient at producing high-quality protein at a price that gives other meats a run for their money. The still relatively low per capita consumption of turkey—Americans eat almost four times as much beef and five times as much chicken—shows that the industry has “huge potential” for sales growth through increased, year-round sales of processed turkey products, said Olson of the Minnesota Turkey Growers.

But the surge in the cost of feed demonstrates that there’s a downside to specialization on the farm. In the past, producing multiple products—corn and potatoes as well as turkeys, for example—allowed farmers to spread their market risk. Today, farmers producing a single product face hard times when a commodity price falls or the cost of a key input increases.

Whether the district’s vast turkey flock grows larger still or shrinks depends on what happens to feed prices, and on how turkey processors and growers adapt if future generations of turkeys cannot be raised quite as cheaply as consumers have come to expect.

Senior Writer Phil Davies contributed to this article.