Author

The issue of credit availability is an especially important one to the Federal Reserve. In response to concerns about the health of the financial sector, the Fed has significantly expanded its programs for providing liquidity to markets since the fall of 2007. Although most of this credit has been borrowed by financial institutions outside the Ninth Federal Reserve District, the district has been more than a mere spectator. Historically a significant source of discount window lending, the Federal Reserve Bank of Minneapolis continues to take an active role in providing additional funds to district financial institutions.

The Fed has made credit more widely available by both expanding old lending programs and creating new ones. (See “Actions to Restore Financial Stability,” by Niel Willardson, in the December 2008 issue of The Region.) Lending at the discount window—the Fed's traditional source of credit for depository institutions, including banks, thrifts and credit unions—was expanded by increasing maximum loan maturities and lowering the relative costs of borrowing.

In addition, the Term Auction Facility (TAF) was introduced in late 2007 to offer a new format—sealed bid auctions—for allocating discount window credit to depository institutions, including community banks common to the Ninth District. (Under the emergency authority granted by Section 13(3) of the Federal Reserve Act, the Federal Reserve also created several new facilities to extend credit to nonbank financial institutions normally not eligible for discount window credit. However, no firms in the Ninth District have borrowed through these programs. For more background on Section 13(3), see "The History of a Powerful Paragraph," by David Fettig, in the June 2008 issue of The Region.)

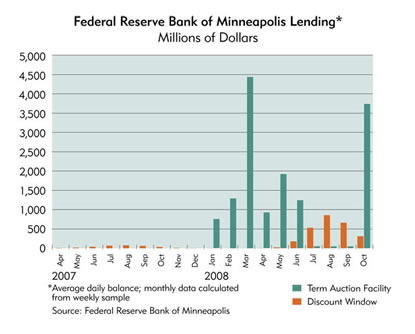

Under these expanded programs, the Minneapolis Fed's lending to district financial institutions has increased rapidly over the past year. In a normal year, total lending from the Minneapolis discount window rarely surpassed $100 million. But in 2008, it peaked above $1 billion.

In addition, district borrowing under the new TAF has skyrocketed. The total balance from outstanding loans at the end of October 2008 was $5.2 billion greater than in October 2006, according to the Minneapolis Fed's weekly balance sheets (Federal Reserve Statistical Release H.4.1: Factors Affecting Reserve Balances). That's an increase of more than 100-fold over the average reported level in 2006. It also accounts for almost 10 percent of the growth in total liabilities (including deposits and other funding sources) among commercial banks in the Ninth District from third quarter 2007 to third quarter 2008.

Despite the rapid rise in Fed lending in the Ninth District, such lending rose even faster in other parts of the country. At the end of October 2008, nationwide lending through traditional programs was 275 times greater than the average reported balance from 2006 (from $340 million to $110 billion). Such large figures swamp even the eye-popping increase in district lending.

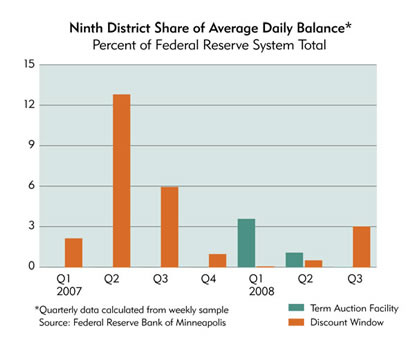

The extensive borrowing elsewhere is a reversal of long-standing patterns. Historically, when overall Federal Reserve lending was much smaller, the Minneapolis Fed's share of discount window lending was disproportionately high—sometimes as high as 40 percent of the national total.

Much of the Minneapolis Fed's lending normally happens during the summer months, much of it through the seasonal lending program, which targets smaller banks with highly seasonal funding needs, typically for agriculture or tourism. But in 2008, the district's share of lending through traditional discount window programs surpassed 10 percent for only one week.

Lending activity through new credit facilities is also much greater outside the district. Nationally, outstanding TAF credit recently surpassed $300 billion. The largest share—and typically well more than half—of those loans has been issued out of the New York Fed. But every Federal Reserve district has had some borrowers over the past year. Though the share of TAF credit funneled through the Minneapolis Fed has hovered below 5 percent, the total dollar amount dwarfs other Minneapolis Fed discount window programs (see charts).

Historically, the Minneapolis Fed has played a significant role in discount window lending. New national credit programs have prompted a huge increase in Federal Reserve lending in the past year, and the Minneapolis Fed's proportion of such lending has dropped as a result. But under the circumstances, that's a market share it doesn't mind losing.

{kind=link}

{kind=link}