Authors

Paul Schreck

Economist

Abstract

Observers argue that increased regulation and supervision added in response to the financial crisis will speed the decline of community banks. Determining if the rate of community bank consolidation is higher than it would have been absent this additional regulation requires a baseline estimate of community bank consolidation. A baseline estimate is particularly important because the number of community banks in the states of the Ninth Federal Reserve District and the nation as a whole has been in a steady rate of decline for several decades. This paper uses several simple methods to provide baseline estimates of community bank consolidation. We will compare actual consolidation against these baselines, updated quarterly, to help determine if consolidation proceeds at a higher than expected rate.

I. Introduction and summary

Community banks and their representatives argue that increased regulatory costs—arising out of post-financial-crisis regulatory and supervisory action—will accelerate the fall in the number of community banks. (We use the term “consolidation” to describe this decline.1) That is, there would be more community banks absent the increase in “regulatory burden.”2 Policymakers, too, have expressed concern about consolidation driven by government action rather than underlying market forces; they have suggested that nonmarket-driven consolidation could reduce the net economic benefits produced by community banks focused on information-intensive relationship lending.3

Thus, observers need to know if the amount of consolidation in a world of increased regulation and supervision is higher than it would have otherwise been. Evaluating this question requires a baseline estimate of consolidation. Baseline-to-actual comparisons are particularly important given that a consolidation trend is already well under way in U.S. banking; the number of community banks nationwide has been falling steadily since its peak in 1984. Some states have seen longer declines, some shorter. Because of these underlying trends, analysts cannot simply use the number of community banks or changes to that number as the sole indicators of the effect of regulatory costs. Those numbers would not distinguish between underlying consolidation trends and consolidation arising out of recent government action.

This paper provides several estimates of baseline underlying consolidation trends. To generate those estimates, we use a variety of simple techniques for the nation and the states in the Ninth District. We make these forecasts for one year out.

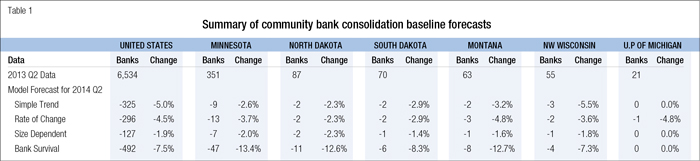

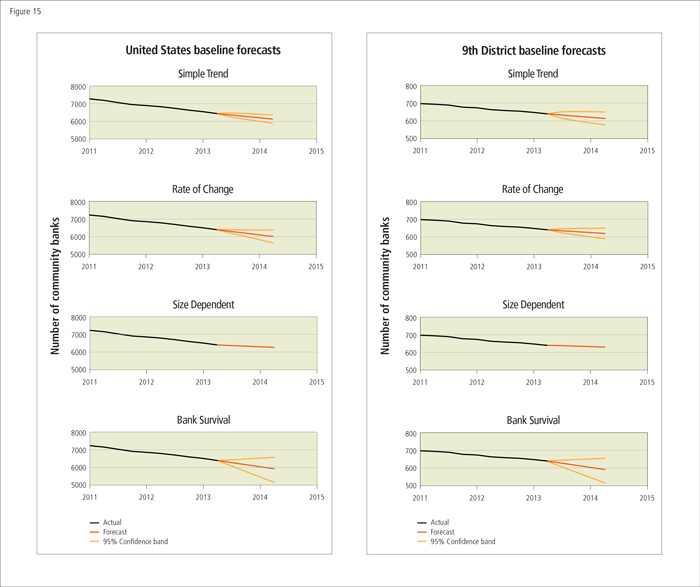

Table 1 summarizes our baseline forecasts for the number of community banks that will exist in each state in the Ninth District and in the United States as of the second quarter of 2014.4 Three of the models forecast annual declines between 2 percent and 5 percent. (The fourth model forecasts a decline between 8 percent and 13 percent.) This range of estimates is consistent with the U.S. long-run trends of a 2.7 percent average annual decrease since 1985 and a 2.6 percent average annual decrease since 2000.

The actual amount of consolidation that will occur in the future can deviate from these baseline estimates for many reasons, including but not limited to forecast error. Less consolidation than expected does not, by itself, prove that regulatory costs do not affect consolidation, nor does higher consolidation than forecast by itself prove that regulation is not affection consolidation. But the size and direction of deviations from forecasts should provide information and context for additional and more direct analysis of the causes of consolidation.

We will update these forecasts quarterly to provide the necessary baseline to make these comparisons.

We proceed as follows. In section II, we summarize data on community bank consolidation over the past 25 years in the nation and in Ninth District states. In section III, we provide summary descriptions of the models used to forecast the baselines (details are in the appendix). In section IV, we provide the baseline forecasts produced by the models. This is followed by a brief conclusion.

II. Historical consolidation of community banks in the nation and the Ninth Federal Reserve District

Consolidation of community banks has occurred at a relatively steady pace. We present data to support this conclusion. First, we present data showing the historical rate of typically constant consolidation. Second, we review the correlation between economic growth and consolidation. We do so to determine if consolidation moves with changing economic conditions. We find a weak link. Third, we review the link between consolidation and prior major increases in regulation. The link is stronger even if not definitive, supporting a closer look at the connection. Finally, we account for the decline in banks by the source of the change. We find that inter holding company consolidation accounted for the bulk of the decline in the 1980s and ’90s and continues to play an important role.

Consolidation to date

Consolidation of banks occurs through failure, merger and acquisition. Some banks simply fail. More specifically, the chartering authority closes certain banks consistent with state or national law. This closure reduces the number of banks.

Mergers and acquisitions also reduce the number of banks. In these cases, one bank can acquire another. Or banks might merge to form a new entity. Sometimes these mergers/acquisitions can occur between two independent banks. That is, the transaction occurs between banks that do not share any common ownership. In other cases, the same ownership can put together two banks that it owns. In all of these cases, the number of banks falls.

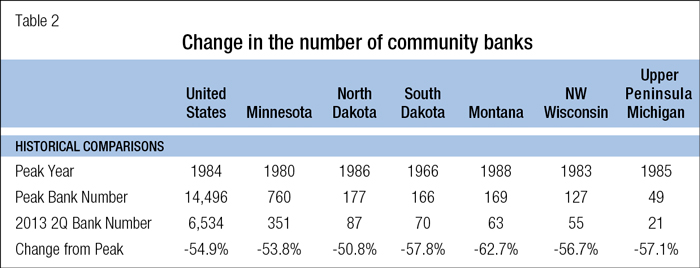

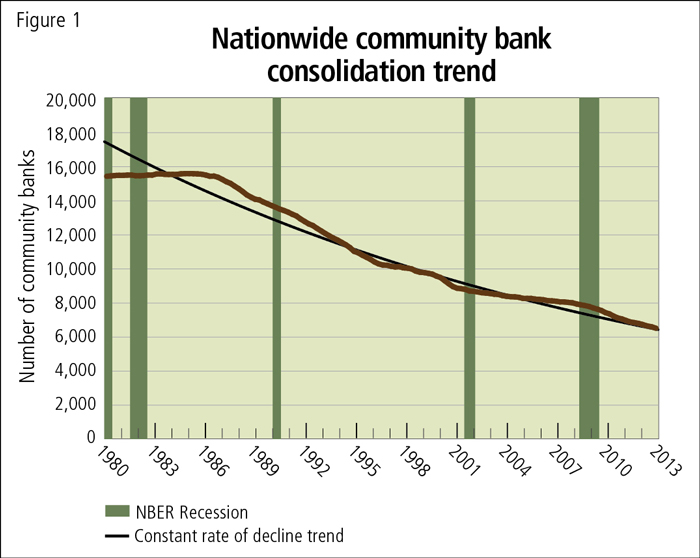

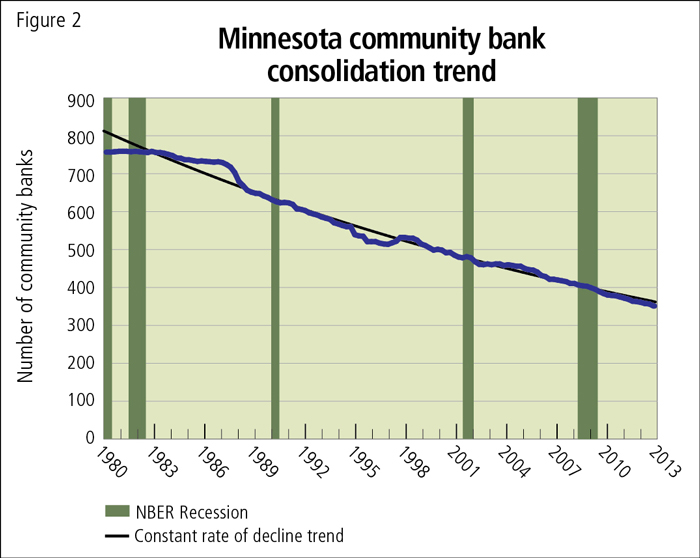

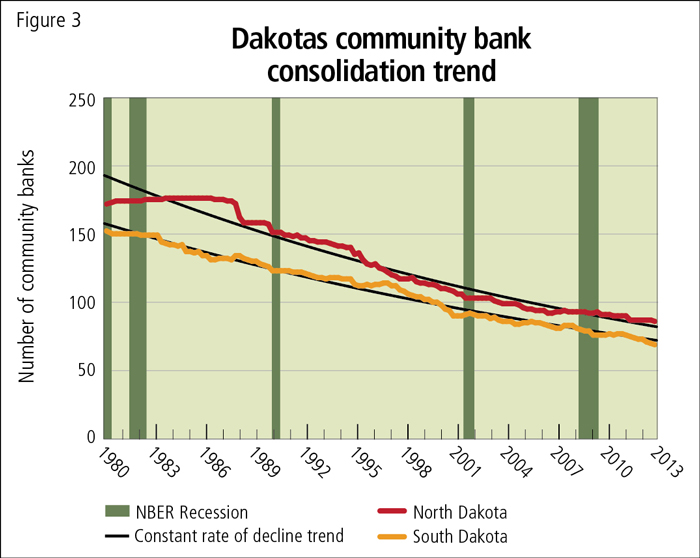

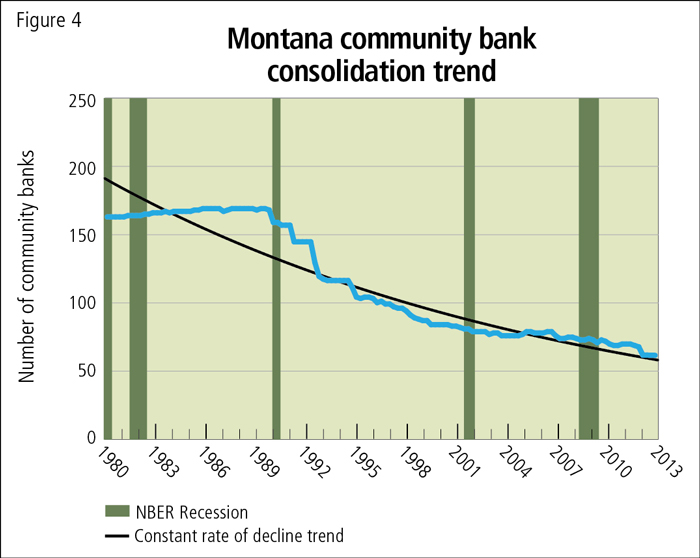

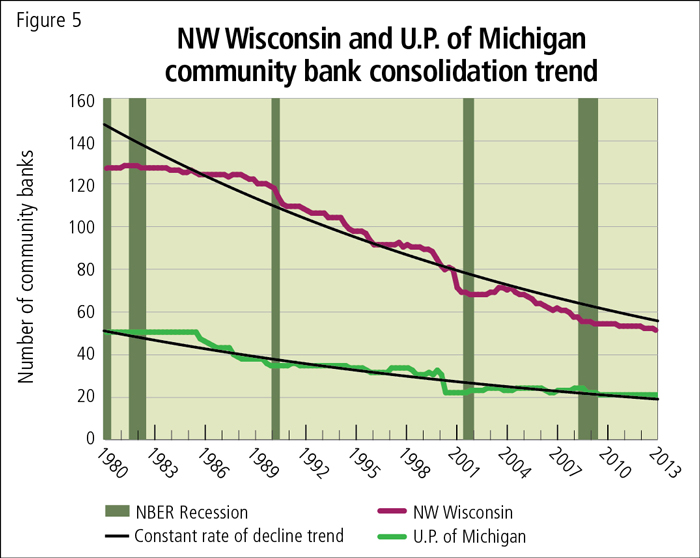

The nation’s number of community banks peaked at 14,496 in 1984. The peaks for states in the Ninth District vary from 1966 for South Dakota to 1988 for Montana; South Dakota’s early peak is an outlier, as most states have peaks around 1985. There has been a fairly steady decline in numbers of community banks since the mid-1980s.

Figures 1 through 5 document this decline. A visual comparison between the absolute level of banks over time and a trend line representing a constant rate of decline highlights the steady pace of consolidation.

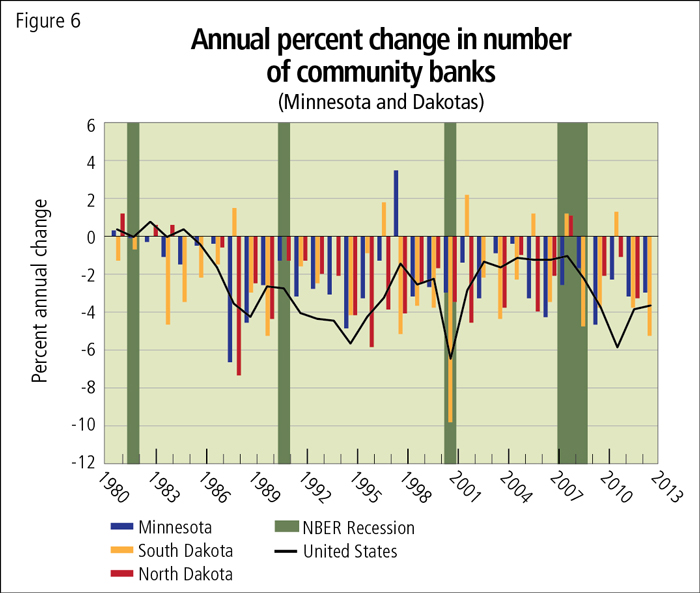

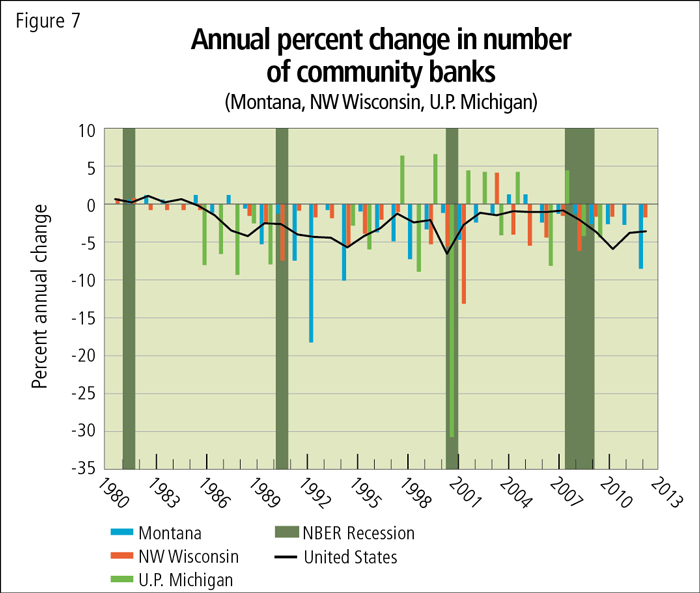

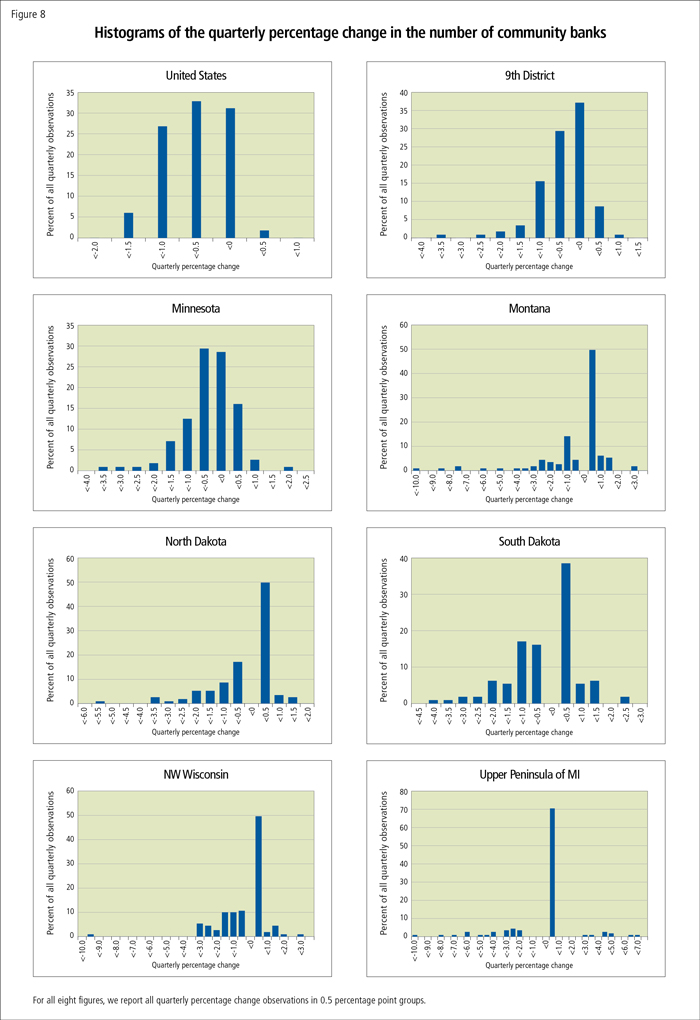

Figures 6 and 7 show the decline in annual percentage terms. Again, the rate has been fairly steady, with the annual decline typically moving within a relatively narrow range. Histograms, which report the percentage of quarterly changes in the number of banks that fall within certain ranges, also show clustering around a central rate of decline, particularly for states starting with more banks (see the histograms in Figure 8).

The total decline for banks has also been relatively similar across states, with about a 55 percent reduction in the number of banks since the peak; Table 2 reports data on the decline of banks since their peak.

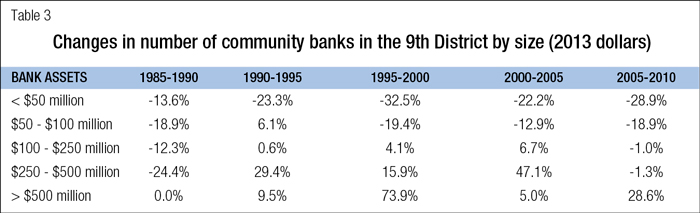

There has been some variation in the rate of decline. Small bank numbers have fallen much more quickly than large bank numbers. Figure 9 and Table 3 document the faster rate of decline for Ninth District banks with assets under $100 million (constant 2012 dollars), particularly with assets under $50 million. The number of such small banks fell by 75 percent since 1985. This decline has concentrated assets in larger banks. The number of banks with assets greater than $500 million had periods of very rapid increase; these banks held 42 percent of Ninth District banking assets as of 1985, while they hold 97 percent now if we include two exceptionally large firms (i.e., Citicorp and Wells Fargo) with charters in South Dakota or 56 percent if we exclude these two charters.

Consolidation links to economic growth and legislative change

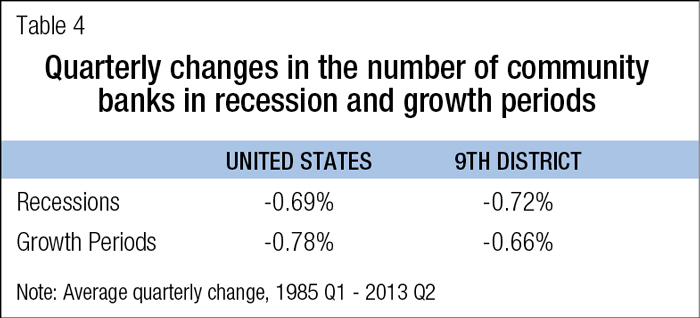

We have highlighted the generally steady rate of consolidation in the Ninth District and the nation. Does this rate of consolidation hold if we break out rates of consolidation by economic growth? Consolidation could pick up during recessions as strong banks acquire weak banks. Alternatively, banks seeking to expand during periods of economic growth might seek out more acquisitions. The data suggest that, on the contrary, there is little if any link between business cycles and trends in bank numbers for the nation as a whole (see Table 4).

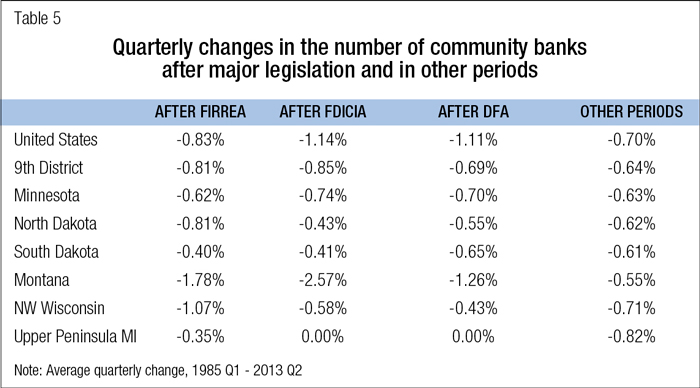

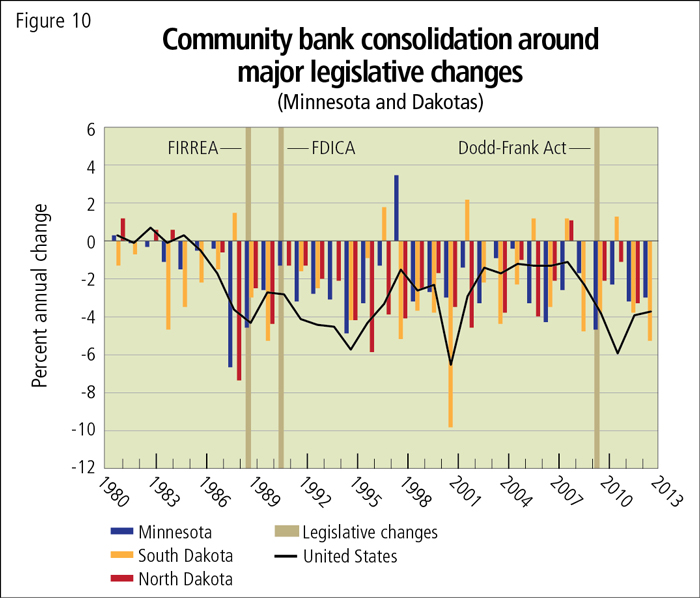

Observers currently view an increase in regulatory costs as potentially catalyzing an increase in the rate of decline of bank numbers. We look at prior periods when Congress took major legislative steps perceived as increasing regulatory cost. Specifically, we look at rates of consolidation in the five years post-passage of laws that augmented bank regulation/supervision. These laws include the Financial Institutions Reform, Recovery, and Enforcement Act of 1989 (FIRREA) and the Federal Deposit Insurance Corporation Improvement Act of 1991 (FDICIA) as well as the Dodd-Frank Wall Street Reform and Consumer Protection Act of 2010 (DFA). As seen in Table 5 and Figure 10, the rates of change during those periods were, indeed, higher than outside those periods (from 1985 to the second quarter of 2013) for the nation and for district states.

These results are suggestive of a potential link between consolidation and legislative changes. This casual analysis therefore supports a closer look at the possible connection between future trends in bank numbers and the more intense supervision and regulation that is now under way, post-financial crisis.

Of course, one should not read anything definitive into this apparent link. The timing of a change in supervision/regulation and future consolidation is unclear. Would we expect an increase in consolidation to occur soon after the passage of new legislation, after regulations are written to implement that legislation or after the regulations are implemented? Moreover, the longer the period we examine, the more the results are confounded with other dynamics that might cause more or less consolidation. The difficulty in trying to confirm a link between changes in regulation/supervision and subsequent consolidation bolsters our case for using a trend baseline when monitoring future rates of consolidation.

Accounting for the source of decline

We break consolidation into four groups. First, we highlight consolidation associated with signs of distress at the acquired bank. The signs include failure and banks rated by supervisors as being in the weakest shape.5 We also include banks with accounting data similar to those of banks that failed or had weak ratings in our distressed group.6

Second, we identify consolidation occurring between banks owned by a single bank holding company (BHC). BHCs have historically had multiple bank charters, because of legislative limits on the geographic operations of banks.7 States began to relax these limits around 1980, and the Riegle-Neal Act of 1994 eliminated these limits via changes to federal law. BHCs began to merge the bank charters they owned following relaxation of such restrictions. We highlight mergers within BHCs because they seem to be a different type of consolidation than that occurring between two independent firms.

We break the within-BHC mergers into two groups: mergers that occur within two years of a BHC buying the bank and those that occur after two years. The former group seems akin to an acquisition between two independent firms; it fits the pattern where a BHC acquires an independent firm and merges it into a previously held bank not long after the initial acquisition. That pattern differs from two long-held banks within a single BHC structure that merge.

Any other consolidation we group into a category of banks that are not distressed and/or not within a single BHC.

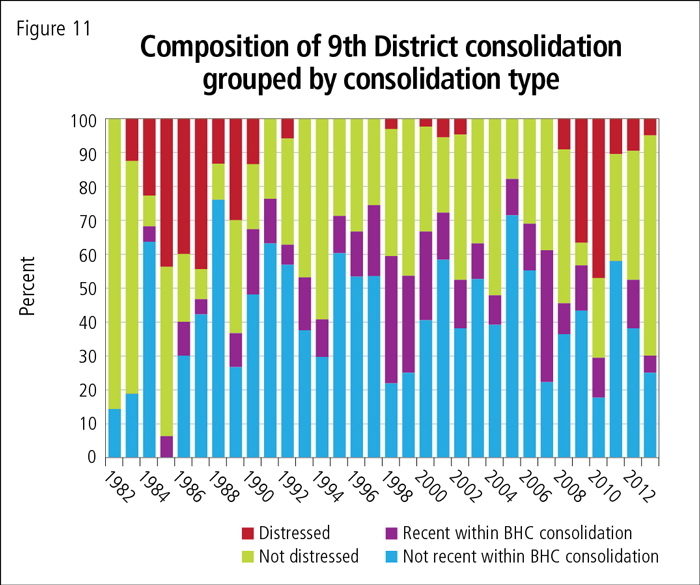

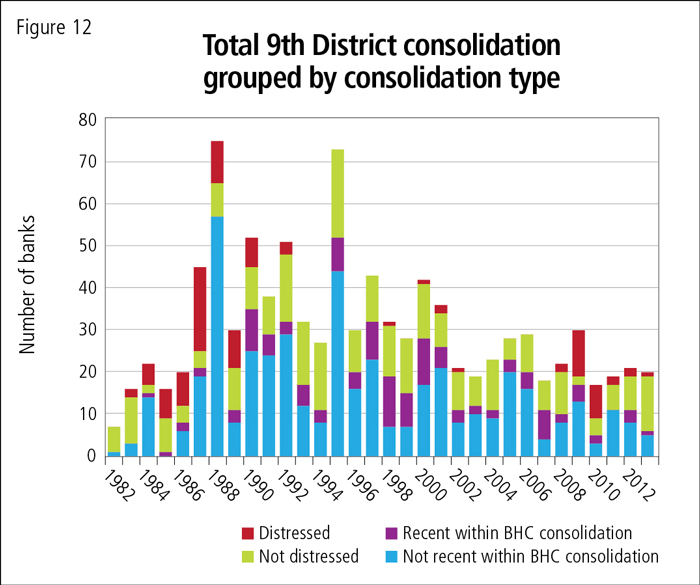

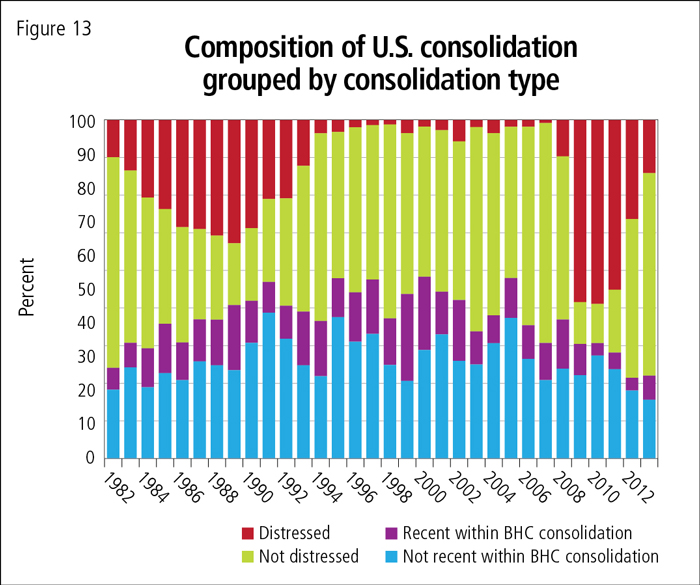

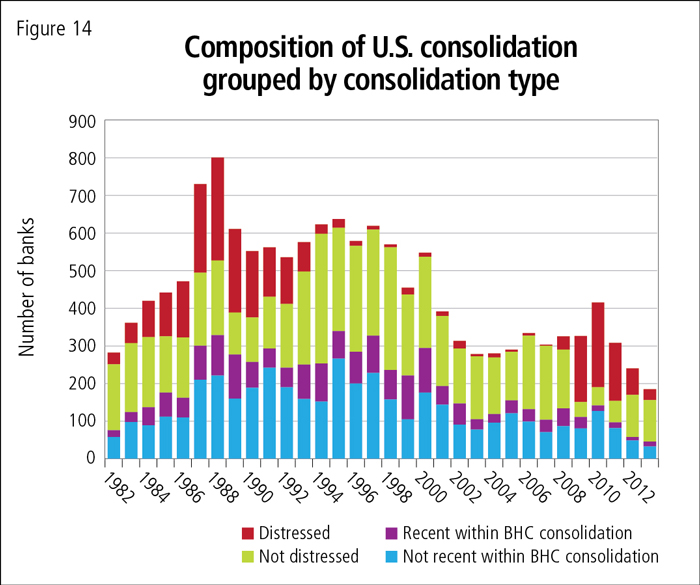

Figures 11 through 14 show the breakdown of consolidation by the groupings just described. These data lead us to three main conclusions:

- Distressed consolidations typically do not account for much of the annual decline since the early 1980s. The exceptions occur, as one expects, during years of significant bank failures (e.g., the banking crisis of the early 1980s and the recent crisis). Even during crises, distress consolidations are not typically the largest type of consolidation.

- About half of Ninth District consolidations and 30 percent of national consolidations reflect within-BHC consolidations that are not recent.

- We consider recent within BHC consolidations and not-distressed consolidations as representing mergers/acquisitions between two independent banks. These groups account for 43 percent of annual decline in the Ninth District and 58 percent of annual decline in the nation.

In sum, the data in section II suggest a fairly steady rate of consolidation driven mostly by within-BHC mergers. The question is whether this rate will accelerate because of higher cost regulation and supervision going forward. Answering this question requires monitoring the observed rate of consolidation relative to baselines of what might have occurred otherwise. We now describe how one might simply and fairly transparently calculate these baseline levels of consolidation trends.

III. Consolidation models

We use four models to make our baseline estimates of community bank consolidation. The models fall into two groups. The first group includes three “time series” models. Forecasts from time series models are heavily influenced by the overall trends in the data over time and do not icorporate data on specific banks as an input. We rely heavily on a time series approach because of the important steady rate of decline trend in the data discussed in section II.

The last model is cross sectional and takes a bottom-up approach. In brief, this approach examines data across a large number of banks and tries to forecast if each specific bank will remain in existence in the future. We then add up the results to come to total bank population numbers.

We use both approaches to forecast the number of community banks for most states in the district and the nation one year out. We also provide confidence intervals for those projections.

Simple, constant extrapolation of consolidation trend (simple trend model)

The first baseline is a simple approach capturing the relatively consistent percentage decline over time.8 The model determines the trend in quarter-to-quarter data over the past 20 years; it is roughly equivalent to the average quarterly change for that period. This forecast then assumes that the percentage decline quarter to quarter in the next period will be consistent with the 20-year trend. Confidence intervals will be consistent with historical deviations from that consolidation rate.

Simple trend model accounting for rate of change (simple rate of change model)

The second model is a bit more complex, but still focuses on determining the underlying trend in the data.9 The model is different from the simple trend model in two ways: First, it estimates the change in consolidation rate instead of the rate itself. Second, it also accounts for the trend in the change in the consolidation rate. This means that periods of accelerating consolidation increase the likelihood of further consolidation in the forecast. A few periods of stability increase the likelihood of further stability (no consolidation).10

Size-dependent consolidation baseline

The third model accounts for the fact that banks in different asset categories have different probabilities of exiting banking. It also accounts for expected changes in the size of banks each forecast quarter: Most banks remain a similar size, but a few grow and/or shrink. For example, banks with assets between $25 million and $50 million in assets may have a higher historical annual exit rate than banks with assets between $500 million and $1 billion in assets. Furthermore, some banks in the $25 million to $50 million size group are expected to move into a larger asset size group during the forecasted period and have a different chance of exit at that point. The amount of consolidation will depend on the number of banks of each size within a state or region. This approach has been used to forecast long-term trends and changes in the structure of the banking sector. (There are no confidence intervals for this model.)11

Bank survival baseline

The fourth model takes the cross-sectional, bottom-up approach. The chance of survival for each individual bank is predicted based on characteristics of that bank and its geographic region. The survival probabilities of each institution along with projected numbers of new banks are used to calculate the expected number of banks in a region. The survival probabilities are based on a variety of balance sheet items, supervisory assessments, geographic variables and state trends.12

IV. Findings

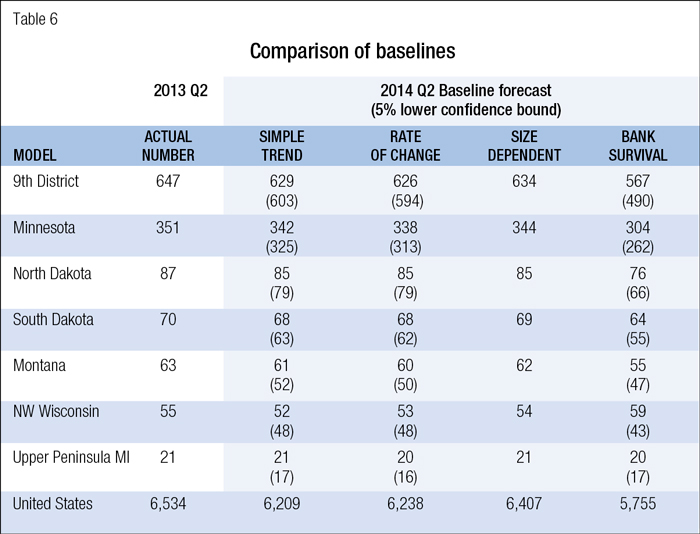

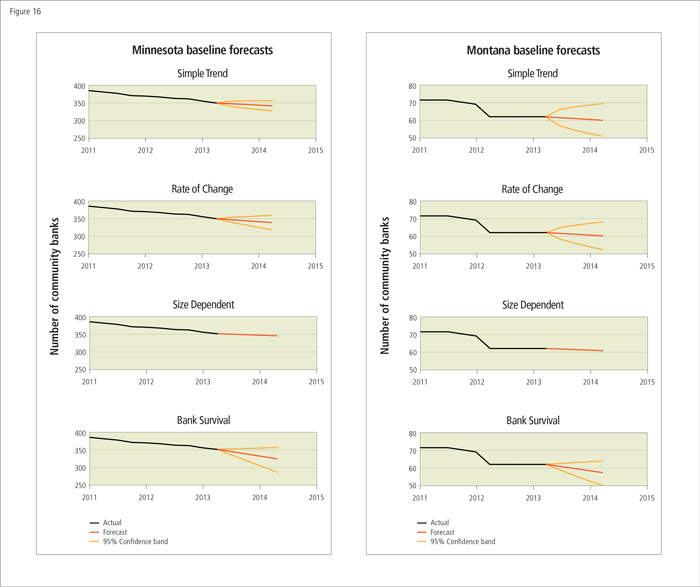

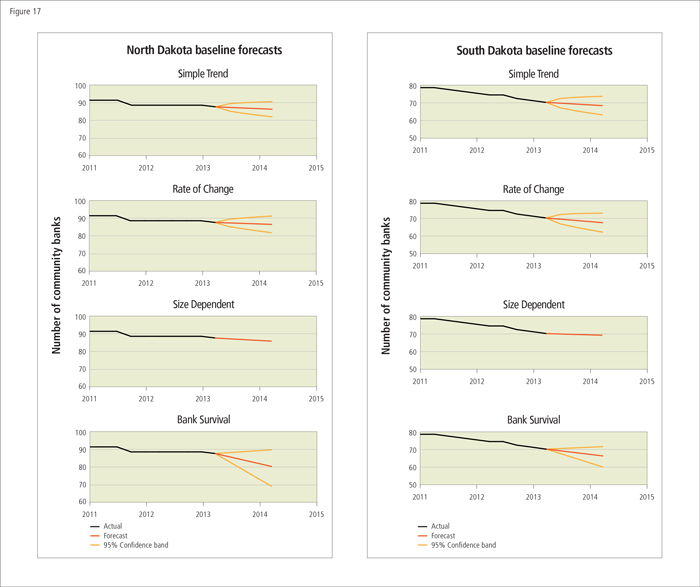

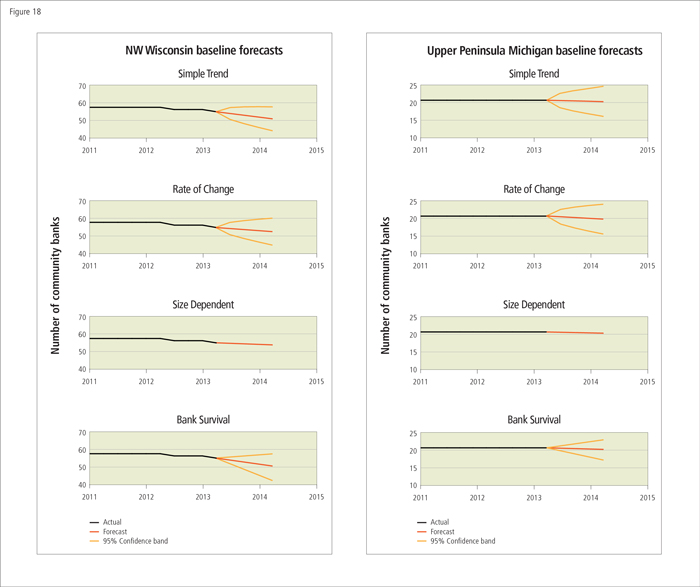

Table 6 and Figures 15 through 18 report the forecasts from each of the models. The main results are threefold:

- Current signs point to continuation of the 25-year consolidation trend, as one would expect given the time series modeling approaches we chose.

- The three time series models produce roughly similar results, particularly for the states in the district with the most banks. The bank survival model produces results that differ from the time series, particularly for geographies—like Minnesota, the Ninth District and the nation—with the most banks.

- The bank survival model forecasts a rate of consolidation as much as three times greater than the time series models. It does so because we used national data to estimate it, and this model is therefore “aware” of the lingering economic stress on banks. The Ninth District has had less consolidation than the country as a whole. With its “awareness” of greater consolidation rates nationwide, the bank survival model forecasts rates of consolidation more akin to the faster national experience.

As noted in Table 6, we report the so-called 5 percent lower confidence bound for each projection. This table captures what the models would consider an unlikely outcome, specifically the outcome expected only once in 20 years. One can compare the actual number of banks in the future to this unexpected figure to gauge if actual experience is unusual.

V. Next steps

To help observers evaluate concerns that the rate of community bank consolidation will increase due to increased supervision and regulation, we have provided baseline estimates for the number of community banks we forecast will exist in the Ninth District and the nation at the end of second quarter of 2014. These baseline estimates will be updated each quarter and will be available at minneapolisfed.org on the Tracking Community Bank Consolidation page.

Endnotes

1 As we discuss in detail, community banks can decline in number due to failure or merger/acquisition. We use consolidation to describe this fall in the number of community banks for expository ease even though the term is more technically linked to mergers/acquisitions. The implications of these two causes of decline can differ on, for example, availability of banking services to a community. We do not explore these implications in this paper or in the baselines we estimate.

2 We define community banks as those with assets below $10 billion for our main analysis.

3 See, for example, a January 2012 speech and February 2013 remarks by Governor Elizabeth Duke. See also Marsh and Norman (2013).

4 The data used in our analysis are released with a lag. We use data from the second quarter of 2013 (close to the most currently available data of third quarter 2013) to make our forecasts for second quarter 2014. In any case, these forecasts will be updated quarterly.

5 Specifically, banks rated composite CAMELS 4 or 5 and banks that formally failed.

6 We take this step because we do not have ratings data for the full period. Specifically, we use a classification tree using equity asset ratios, earnings asset ratios and share of loans in nonaccrual to identify firms classified as failures or merging with a CAMELS rating of 4 or 5. Earnings are estimated to be the first variable in the classification.

7 Calem (1994) discusses these limits and provides contemporary commentary.

8 We are describing an AR(1) estimate.

9 We are describing an ARIMA model, specifically the same model used by Jones and Critchfield (2005) to forecast the number of banks nationally.

10 The second model will also produce a more certain estimate of short-run outcomes relative to the first model. Over the longer periods, it produces more uncertain estimates.

11 See Robertson (2001) and Janicki and Prescott (2006). Specifically, our model uses inflation-adjusted data from 2000 to 2011 to measure changes in size, exit and entry of new banks. These studies show some changes in the transitions from decade to decade, so we chose a shorter, more recent period.

12 This model forecasts all types of consolidation. Thus, while it has similarities to models that forecast just failures or distress, it considers a wider range of variables.

Tables and Figures

References

Calem, Paul S. 1994. “The Impact of Geographic Deregulation on Small Banks.” Federal Reserve Bank of Philadelphia Business Review (November/December), pp. 17-31.

Janicki, Hubert P., and Edward S. Prescott. 2006. “Changes in the Size Distribution of U.S. Banks: 1960-2005.” Federal Reserve Bank of Richmond Economic Quarterly 92 (Fall), pp. 291-316.

Jones, Kenneth D. and Tim Critchfield. 2005. “Consolidation in the U.S. Banking Industry: Is the “Long, Strange Trip” about to End? FDIC Banking Review 17 (4), pp. 31-61.

Marsh, Tanya D., and Joseph W. Norman. 2013. “Reforming the Regulation of Community Banks after Dodd-Frank.” Community Banking Conference. Federal Reserve Bank of St. Louis.

Robertson, Douglas D. 2001. “A Markov View of Bank Consolidation: 1960-2000.” Economic and Policy Analysis Working Paper 2001-4. Office of the Comptroller of the Currency.

Related:

- Appendix - summary of key technical features of the four baseline models [pdf]

- Tracking Community Bank Consolidation

Updated data, charts and forecast for baseline estimates

{kind=link}