Author

Bonding is back in style in Belle Plaine, Minn. In 2014, faced with crumbling streets, the Minnesota River community southwest of Minneapolis pulled the trigger on a $2.4 million bond issue to pay for street and utility reconstruction in a seven-block area of town.

The project had been planned for years, but was put off during the Great Recession and slow economic recovery, said City Administrator Holly Kreft. City leaders were unwilling to assume more debt at a time of high unemployment and sagging revenues at area businesses. “Given the uncertainty of the market ... they wanted to make sure that [property owners] who were struggling already were not hit with an additional [tax] assessment,” Kreft said.

Today most city taxpayers are better off and so are more predisposed to vote for bond issues supported by property taxes. At a public hearing on the street project, “We didn’t have anybody come up and say, ‘Don’t do this project,’” Kreft said. “People were saying, ‘Yes, please do our project; we know we have to pay 30 percent of the cost, but we need it.’ That’s a reflection of the change in the market.”

In the past two years, more and more Ninth District communities have jumped back into the market for municipal bonds, debt securities used to pay for large capital projects such as roads, wastewater treatment plants, athletic fields and school buildings. The 2008 financial crisis rocked the muni bond market, but since 2011 bond issuance in district states has seen a resurgence. The value of bond issues has increased, although issuance hasn’t returned to prerecession levels.

Local governments are feeling more secure in their ability to support bonding, said Kathy Aho, president of Springsted, a Twin Cities-based firm that advises local governments on bond issues. “What we’re seeing in the communities that we work with is that the resistance to borrowing for new projects has diminished as the economy has stabilized. People are more confident that tomorrow is going to be similar to today, and today ain’t so bad.”

Low bond interest rates have also fostered bonding, both for new projects and to refinance previously issued bonds. But not all district communities have experienced a bonding rebound. Some lack the tax base to support bond issues; in others, economic recovery hasn’t changed a longstanding aversion to bond debt. And across the district, bonding for housing development hasn’t regained the favor it enjoyed before the recession.

Brighter days for bonding

The municipal bond market has come far since 2008, when bond investors sat on their hands and issuance sank under the weight of high unemployment and falling property values. “It’s difficult for many of us to remember how dark everything was at that time,” said Kreg Jones, managing director of fixed income capital markets at D.A. Davidson & Co., a bond underwriter based in Great Falls, Mont. “There was really no buy side to the market, and issuers were even reluctant to ask voters or ratepayers for anything because of the hard times.”

The Great Recession changed the muni bond market in important ways. A flight to quality by investors, combined with the financial troubles of bond insurers, made bond issuance harder for less creditworthy public entities. Investors avoided some types of bonds, such as issues for housing development, because they were considered too risky. And issuing bonds for small projects under a million dollars became problematic because of the expense of increased due diligence by investors.

Bonding activity faltered in the financial crisis, both nationwide and in the district, according to data compiled by Thomson Reuters, a financial services information firm. From 2007 to 2008, the value of new bond issues in the United States dropped 9 percent, and in district states new bond volume fell twice as hard (see Chart 1).

But the bond market didn’t collapse in the depths of the recession. It got a leg up from the Build America Bonds program, created in 2009 as part of the federal government’s economic stimulus package. Federal tax credits and subsidies encouraged the issuance of billions of dollars in taxable BABs until the program expired at the end of 2010. About $4.1 billion in BABs were issued in district states.

The refinancing of variable-rate notes—a type of bond with an interest rate that changes periodically—into long-term, fixed-rate financing during and after the recession also shored up muni bond volume, according to industry sources.

In 2011, bond issuance dropped nationwide—the number of new issues plummeted 23 percent—and in district states. But U.S. bonding increased slightly in 2014, with further strengthening last year. In the district, bonding volume increased significantly in 2015, building on gains from the year before. New issues accounted for over 60 percent of the value of district bonding; the balance was refunding—the refinancing of outstanding bonds.

“You’ve seen more appetite over the last 18 months to two years for new money, new projects” in municipal bonding, said Brian Reilly, principal and senior municipal adviser at Ehlers Inc., a large bond sales firm with offices in the Twin Cities.

In Wisconsin, the value of new issues increased 42 percent from 2014 to 2015, to over $3.7 billion—the most new issuance since 2009. Much of that increase came from new bond debt by cities, counties, and local districts and authorities. (Thomson Reuters figures show that overall bonding by Wisconsin cities and towns rose by roughly the same proportion in 2015.)

In Minnesota, new issuance surged in 2014 and declined slightly last year, while total issuance was up year over year. Only in Montana has new issuance failed to rally in recent years, although it increased 32 percent in 2015. (Click the “next” button under Chart 1 for additional charts on bonding trends in individual district states.)

Deferred no more

The main impetus for increased municipal bonding in the district is a newfound willingness by state and local government to undertake large capital projects that require debt financing and by investors to hold municipal bonds.

During the recession and its aftermath, many communities shelved plans to fix up city buildings, repave streets or lay new water and sewer lines. Today they’re playing catch-up. David Unmacht, executive director of the League of Minnesota Cities, sees a “dramatic need” for capital spending in Minnesota cities and towns. “The fact of the matter is that, regardless of the state of the economy, the need for these improvements was, is and remains there.”

A recent survey by the Minnesota Pollution control agency identified $4.2 billion in necessary upgrades to sewer systems and wastewater treatment facilities in communities across the state.

Current market conditions appear ripe for renewed capital investment. In communities across the district, lower unemployment and rising property values have bolstered confidence that residents will accept higher fees or taxes necessary to support new bonding. “Certainly on the part of the elected officials, there does seem to be more openness to absorbing the impacts of taking on capital and infrastructure projects,” Reilly said.

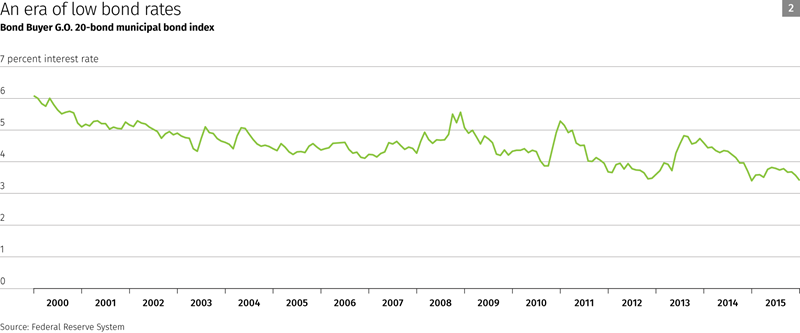

Historically low interest rates offer another incentive to bond now for projects. Federal Reserve data show that U.S. long-term bond rates rose during the financial crisis, then declined (see Chart 2), dropping rates below even the historically low rates that had prevailed since the early 2000s. The average 2015 rate for 20-year general obligation bonds was the lowest in half a century. “There’s a sense within our cities that now is the best time to borrow,” Unmacht said. “Interest rates are low and money is cheap.”

An improved local economy and low interest rates were instrumental in the Belle Plaine City Council’s decision to approve bonding for street reconstruction, Kreft said. The general obligation bond issue comprised $1.2 million for the street work, slated to be completed this summer, and an equal amount to refinance outstanding bonds issued in 2007 for street, park and sewer improvements.

On the other side of the Twin Cities metro area, the city of Red Wing has issued $15.5 million in bonds since 2010, a marked increase from previous years. A $7.7 million issue last year paid for street reconstruction, improvements to City Hall and equipment purchases.

Finance Director Marshall Hallock said increased property tax capacity due to investments by Xcel Energy in the city’s Prairie Island nuclear generating plant opened the door to bonding for capital projects that had been deferred for years. He added that a healthier local economy, “extremely low interest rates” and “hungry contractors” also were factors in the decision to “start an aggressive campaign to address the backlog that we’ve had.”

All you ever wanted to know about muni bonds

State and local governments have long relied on bond financing to pay for capital projects such as schools, highways, civic buildings, and recreational and cultural amenities. When a government entity issues bonds, it promises to pay investors interest and return the principal on a specified maturity date.Read more

True to their school

Similarly, rising demand for capital spending combined with favorable market conditions has spurred increased bonding by school districts in some states.

In Wisconsin, bonding by K-12 schools fell during the recession but has since rebounded, according to the State Department of Public Instruction. In 2014, the value of bond issues, including refunding, surged to over $580 million, more than double the 2013 volume. Bonding in 2015 was almost $400 million.

Tighter state revenue caps since 2009 have restricted school spending in Wisconsin. Many districts that put off construction and remodeling are now issuing bonds approved in local referendums, bypassing the caps, said Jon Bales, executive director of the Wisconsin Association of School District Administrators (WASDA).

There’s a “large need for capital projects for buildings,” he said. “Secondly, it’s an opportune time relative to interest rates and also construction costs.” (The recession dealt a lasting blow to growth in construction wages and materials prices in Wisconsin and other district states.)

In Montana, “we’re seeing some of the largest educational bond issues that the state has ever seen, in part because of pent-up demand,” said Jones of Davidson and Co. Voters in Billings, where an influx of workers who commute to the Bakken oilfields has swelled school enrollment, approved a $122 million bond in 2013 to pay for school construction and renovation. Last fall, Missoula County Public Schools issued $158 million in bonds for extensive renovations of four high schools and all elementary and middle schools in the district.

Municipal bond issues in the district don’t usually go begging for takers. Public debt in the region is attractive to investors because, for the most part, state and local governments and school districts have sound credit ratings from credit rating agencies. “By and large, the Midwest represents a pocket of credit strength, and if you were to look at the ratings spectrum, we would skew to the high end in the distribution of ratings,” Reilly said.

In Minnesota, Ehlers competes with other bonding agencies for K-12 business, and when Eau Claire, Wis., issued $16.5 million in bonds last summer for street repairs and downtown development, 21 bond dealers bid for the right to market different portions of the issue.

The bonds of debt

Not everybody is riding the bonding wave in the district. In areas with stagnant populations or little commercial development, the local tax base may be insufficient to support bonding for rebuilding streets, repairing buildings and making other necessary improvements.

Elsewhere in the district, some communities have the fiscal means to bond for capital projects but are reluctant to assume debt, even under favorable terms such as low interest rates. Reflecting the views of constituents, some local governments are averse to bonding, said Aho, from Springsted. “Each community has a personality, and some of those personalities would prefer not to take on debt, because debt is bad.”

Local governments in the Bakken oil patch have done little bonding over the past decade, despite the huge impact of the oil boom on roads, schools, utilities and other public goods and services. Instead they have relied on oil and gas production tax revenue and low-interest state loans to pay for capital projects.

In North Dakota, only Williston and Watford City have run up significant bond debt (at the end of last year Williston carried $72.4 million in outstanding bonds), and over the past year shrinking energy tax receipts due to a decline in oil prices have led both communities to reconsider their bonding plans. Watford City Mayor Brent Sanford said the city is “tapped out” and “done with bonding” and won’t increase sales or property tax rates to support more bond issues.

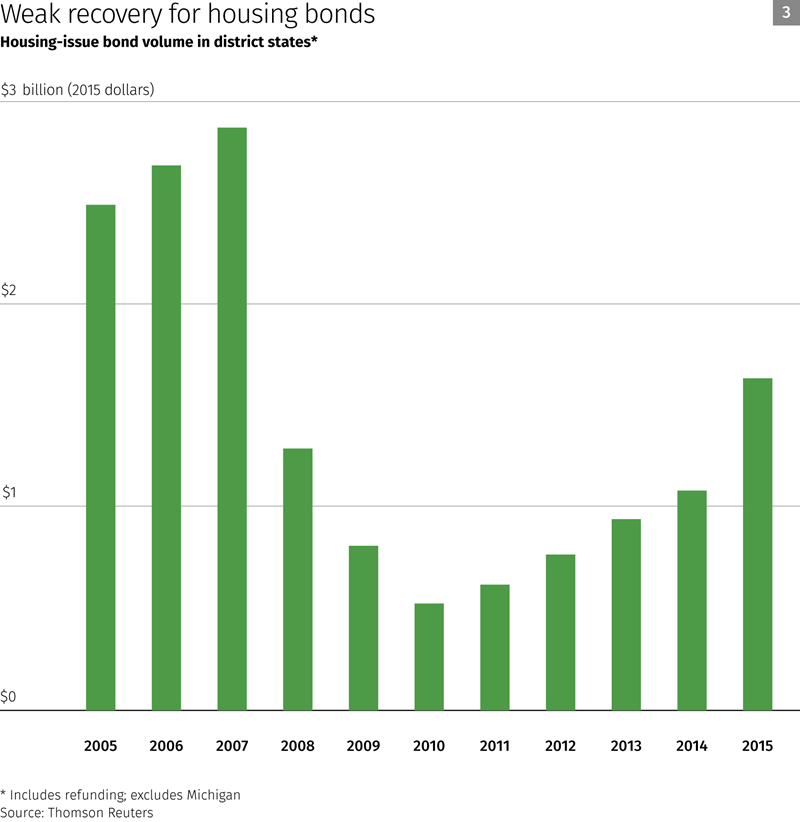

Even in district states and communities that have seen increased bonding, bonding for housing has made only a partial comeback. Echoing a national trend, the volume of bonds issued in the district for housing purposes has fallen sharply since the housing boom of the mid-2000s, according to data from Thomson Reuters (see Chart 3).

Much of the decline in housing bonds was due to a shrinking market for so-called dirt bonds—bonding for utilities and other infrastructure in exurban housing developments. After being saddled with bad debt during the recession, many municipalities and other bond issuers remain leery of bonding for housing infrastructure, said Reilly of Ehlers.

Despite scant bonding activity in some communities and for some types of bonding, demand for projects and economic conditions in the district appear conducive to increased bonding this year.

Bales of WASDA sees ongoing demand for school bonding in Wisconsin to refurbish and upgrade aging buildings and, in communities with rising enrollment, to build new ones. “I expect the trend to continue,” he said. “In population growth areas, there’s still going to be a need to add facilities.”

A rise in short-term interest rates since December doesn’t necessarily augur a national slowdown in municipal bonding. Aho and Reilly noted that interest rate hikes have been modest and that long-term rates are what matter in the bond market. Higher returns from short-term investments could in fact stimulate bond issuance, particularly refinancing, Reilly said. Issuers may find it advantageous to advance refund—issue new bonds and invest the proceeds in an escrow account to pay off an older bond when it comes due.

Higher interest rates haven’t changed Red Wing’s plans to continue bonding for capital projects. Capitalizing on what Hallock called a “unique point in time,” the city intends to issue $7.9 million in general obligation bonds this summer to finance construction of a new public works facility and ongoing repairs to the downtown library.