Author

In the wake of the recent financial crisis, government debt relief to private firms has been viewed as odious, to be avoided if at all possible. But could it actually be good policy?

Recent research by Minneapolis Fed Senior Research Economist Javier Bianchi suggests that when done properly, government financial relief for private businesses is a prudent, even beneficial practice for the overall economy. A well-designed policy can actually curb moral hazard—the tendency to take greater risks when someone else pays the cost of failure. Good debt-relief policy can also lead to optimal employment and borrowing decisions by reducing financial frictions that otherwise constrict firms wanting to hire and invest.

These conclusions may seem contrary to conventional wisdom. An implicit or explicit promise from governments to rescue firms going bankrupt is widely considered both unfair and inefficient. The 2010 Dodd-Frank Act (DFA) sought to address existing weaknesses in the financial system and avoid future crises by including explicit restrictions on government lending to financially distressed companies.

Bianchi’s research clarifies that while bailouts for just a few select firms is unwise and likely to exacerbate moral hazard, a policy that provides broad-based relief and only during a systemic crisis will be beneficial both before and after a crisis. Indeed, it affirms the DFA’s Title XI requirement that emergency lending programs provide for “broad-based eligibility.”

A bailout model

He starts by building a model economy that permits qualitative and quantitative comparison of alternative bailout plans. The model includes households that consume, provide labor, pay taxes and hold shares of the model’s firms. Firms hire workers, invest in capital and issue stock and bonds; they pay wages to workers, interest to bondholders and dividends to shareholders.

To generate a credit crunch to precipitate a financial crisis, the model economy must include a mechanism whereby firms are occasionally unable to finance their preferred level of investment. Bianchi introduces two such frictions. The first is “unenforceable” debt contracts, meaning that lenders can’t get iron-clad guarantees that borrowers will repay their debts. Before agreeing to lend, therefore, lenders demand collateral. The constraint on borrowing is set by the amount of collateral a borrower can offer. Bianchi’s second model friction is an equity constraint that requires firms to issue stock to raise more equity and pay dividends to the households that buy their stock shares. The necessity of paying that dividend is the constraint.

When economic times are good, these frictions don’t restrict firms from borrowing and investing as much as they want. But when leverage is high (firms have borrowed a lot relative to their assets) and a bad shock hits the economy, firms are forced to cut back, leading to less investment, hiring and production. Financial crisis breaks out; prolonged recession ensues.

Analysis

Bianchi’s model allows him to analyze, theoretically and quantitatively, the optimal response for policymakers who want to avoid recession and the economic turmoil of systemic financial collapse. “How should bailouts be designed,” he asks in his Minneapolis Fed working paper (“Efficient Bailouts?” wp730), “and how important are policies to prevent excessive risk-taking?”

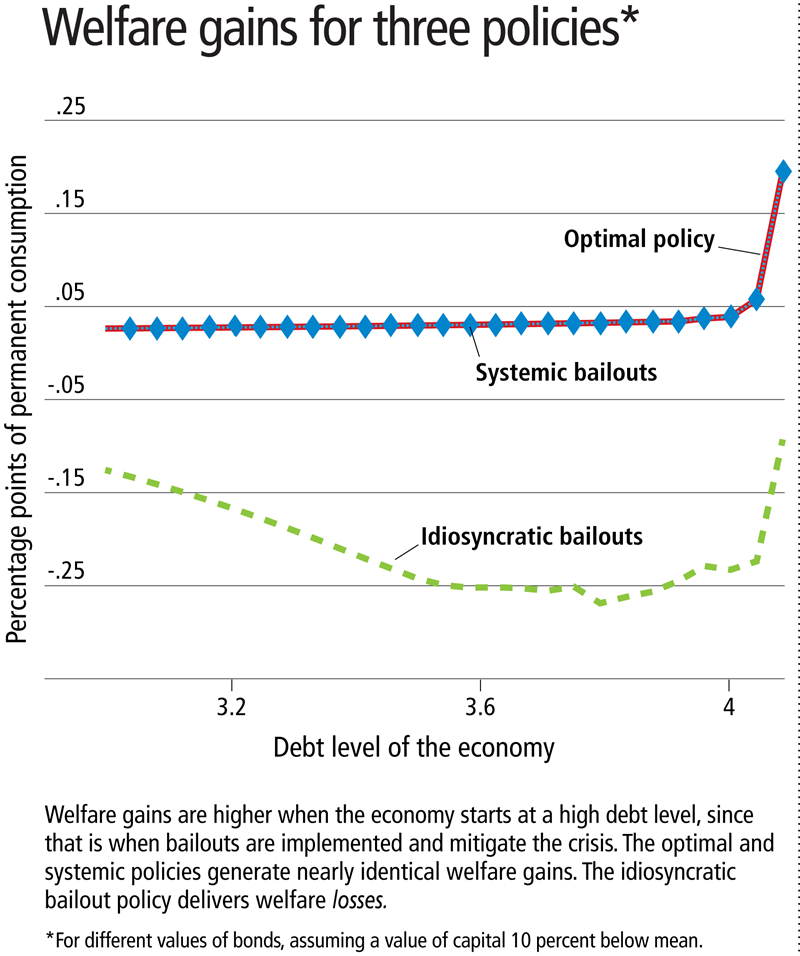

Bianchi considers three bailout policy designs: “optimal,” “systemic” and “idiosyncratic.”

- “Optimal,” the best possible policy, includes a government “debt tax” exacted from firms to discourage overborrowing.

- “Systemic” bailouts exclude a debt tax but are enacted only when the entire financial system is distressed and bailouts apply to all institutions, not just a favored few.

- “Idiosyncratic” bailouts are what we’re most familiar with: providing public funds to help a select number of financially distressed firms because their collapse would significantly impact the broader economy.

When Bianchi runs his model under these three options, the results are qualitatively clear. Optimal policy is best in that it results in the least economic damage from the financial shock and essentially no excessive borrowing because the debt tax discourages it. Systemic policy also works well from a macro and welfare perspective; overborrowing is still possible, though, because anticipation of bailouts naturally induces moral hazard. The idiosyncratic bailout policy is the worst of the three, resulting in significant economic damage spurred in part by excessive borrowing.

His quantitative results provide much richer perspective. Using U.S. data from 1984 to 2014 to calibrate the model, he measures the degree of response to different policies when financial shocks hit the economy. The stimulative effect of a bailout is large, he calculates: A bailout equal to 1 percentage point of GDP in a crisis comparable in size to the Great Recession generates GDP gains of 1.5 percentage points (relative to no bailout). Thus, well-designed bailouts can provide an important stabilizing effect, preventing prolonged recession.

Another intriguing quantitative finding is that there is very little difference between optimal policy (that includes a debt tax) and systemic policy (which doesn’t) in terms of welfare gains. Bianchi finds results under the two policies “almost indistinguishable.” (See chart.) Given that debt taxes clearly discourage excessive borrowing, why is there so little actual difference?

“The key reason why systemic bailout policies generate little moral hazard is [that] these bailouts are contingent on a systemic crisis and not on individual firm decisions. ... Anticipation of bailouts [does] not [much] modify borrowing decisions,” writes Bianchi. “In contrast, with the idiosyncratic bailout policy, the firm directly internalizes how borrowing decisions affect debt relief policies and significantly raises leverage to take advantage of bailouts.”

Conclusion

In light of prevailing sentiment about bailouts and the moral hazard they create, Bianchi’s findings are startling. “In fact, prohibiting bailouts can actually increase financial instability,” he writes. A well-designed bailout plan is wise policy and can improve welfare not only after a financial shock happens but before it does. Bailouts “alleviate the undercapitalization of firms during a financial crisis” and speed economic recovery. Thus, “bailouts constitute a powerful stabilizing force ex post, yet generate modest moral hazard effects when appropriately designed.” Proper design is crucial. “Bailouts,” he stipulates, “should be broad based rather than targeted to specific institutions, in line with the special provisions introduced in the Dodd-Frank Act.”