Author

This essay is also available on Medium.

I joined the Federal Reserve because I want to help tackle the most important economic policy challenges we face as a country. In some cases, the Federal Reserve has tools that can directly address problems, including the various monetary policy tools we have used over the past several years and during the financial crisis. In other cases, our contribution can be made through research and analysis to understand issues and identify potential solutions. After my appointment to the Minneapolis Fed was announced in November 2015, I asked the economists in our Research Department to think about the biggest economic challenges our country might face over the next decade. We gathered in January to discuss their ideas. That process identified an array of issues, including ongoing risks posed by large banks as well as economic disparity within the United States, among other topics. Eight months later, I am pleased that our ending-too-big-to-fail initiative is on track to produce a plan that we will release by the end of the year. And we have recently begun engaging with a wide range of constituents to better understand the structural factors that lead to disparate economic outcomes for different communities.

In addition to these important issues, there is another fundamental question that we are trying to understand: Why has the economic recovery been so slow?

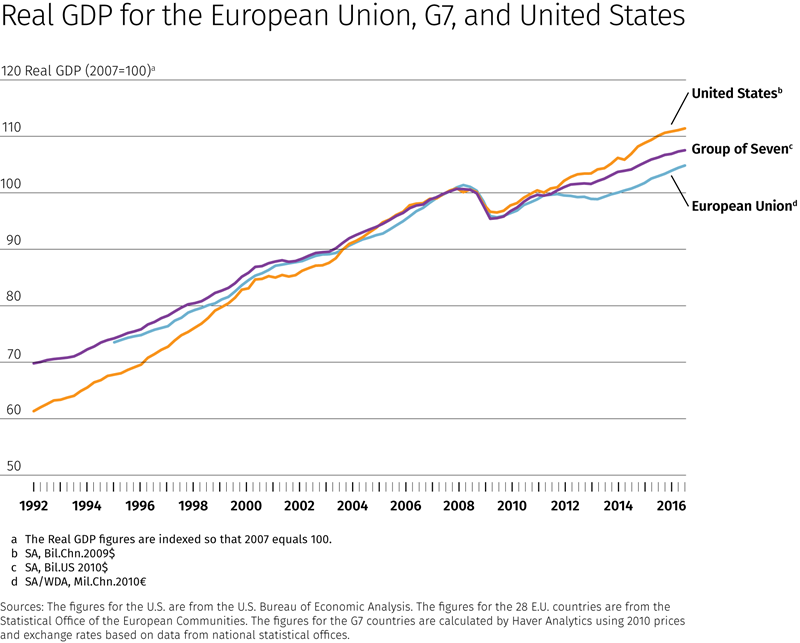

Major central banks have implemented extraordinarily accommodative monetary policies, including record low interest rates for many years and quantitative easing programs, which have driven down long-term interest rates and driven up asset prices via large-scale asset purchases. When these programs were launched, some experts expressed understandable concerns that these programs could result in high inflation. Although, eight years on, it hasn’t happened yet. In fact, inflation has been too low rather than too high for several years. When accommodative monetary policies were coupled with expansionary fiscal policies, other experts had reasonably expected a strong recovery from the depths of the Great Recession. Going back decades, the U.S. economy has exhibited a remarkable ability to bounce back: The rule of thumb was the deeper the recession, the stronger the recovery. Yet, the U.S. economy has experienced the weakest recovery in the postwar period, despite unprecedented policy responses to a very deep recession. Why?

It is important to understand why the recovery has been so slow if we hope to design policy responses to jump-start economic growth. The consequences for Main Street are profound: If the U.S. economy fails to return to precrisis growth rates, improvements in standards of living for families will come very slowly, and entitlement programs such as Social Security and Medicare will be much harder to pay for. Small changes in a country’s long-term growth rate result in enormous changes in outcomes for its people. For example, real economic growth of 3 percent instead of 2 percent over the next generation would result in inflation-adjusted income being roughly one-third higher, $30,000 per person, after 30 years.

Because this issue is so critical, I use this essay to initially explore some reasons why growth has been slow and discuss many potential policy responses, some of which I support and some of which I don’t. This essay is very broad in scope as I lay out these wide-ranging issues. I plan to explore some of these specific points in more depth in the future.

The Approach

Many experts are wrestling with the fundamental question of why growth has been so low. Harvard Professor Greg Mankiw published an op-ed1 in the New York Times in June that identified five possible explanations for the slow recovery. He concluded by admitting he didn’t know which diagnosis was right, nor did he offer recommended policy solutions (space is limited in an op-ed). I thought Mankiw’s framework for considering the range of possible diagnoses was helpful, so I challenged my Research Department at the Minneapolis Fed to respond to his commentary. Did they agree with his five possible diagnoses? Are there others? And, importantly, if we knew which diagnosis was right, what could we do about it?2

This is not unlike the challenge doctors regularly face with a sick patient who has multiple, often conflicting, symptoms. If the patient is sick enough, doctors don’t have the luxury of doing nothing until they are certain about the underlying cause. They must act—and will try different treatments, starting with those that have few side effects, in order to help the patient recover.

Given how important it is to the future well-being of our society that the economy returns to strong growth, it could be very costly if policymakers wait until the economics profession reaches consensus about which diagnosis is right before taking action or if they simply wait for the economy to heal itself. The purpose of this essay is to build upon Mankiw’s framework first by identifying the range of possible diagnoses for why the recovery has been so slow, then by considering potential policy responses for each diagnosis and, finally, by evaluating the downside to those policies if it turns out the diagnosis was wrong. Ideally, we can come up with some policy solutions that have limited downside risk.

I must acknowledge up front that most of the policy prescriptions I will identify are outside the scope of monetary policy. Monetary policy is largely doing what it can to support a robust recovery, and what remains are fiscal and regulatory policies. If we are able to apply our research expertise to identify potential solutions, I believe it is appropriate to do so and then leave it to other branches of government to decide whether or not to pursue them.

The Symptoms

Some of the troubling symptoms we are observing are global, showing up in several advanced economies at the same time, while some are local to the United States. As I will explain in the remainder of this essay, it is difficult to find a single diagnosis that can explain all these various symptoms and why they are showing up where they are showing up.

The advanced-economy symptoms include: (1) Much slower growth than was enjoyed precrisis. (2) Much slower productivity growth in the past several years than had been experienced before 2007.3 (3) Very low real interest rates (partially a result of common policy actions of central banks, but primarily due to neutral real rates that have been falling since around 1980).4,5 (4) Low inflation, or even bouts of deflation, despite aggressive monetary accommodation.

Symptoms specific to the United States include: (1) Low investment in recent years.6 (2) Increased personal savings rate since the crisis.7 (3) Reduced business dynamism since at least the mid-1980s.8 (4) Low compensation growth.9 On the positive side, the United States has experienced strong job growth since the end of the Great Recession.

In addition, some important global factors are worth keeping in mind: (1) The adoption of technology is often a global phenomenon (regardless of where it is invented). (2) Demographics are generally trending in the same direction in major advanced economies: Populations are growing more slowly than in prior decades, families are having fewer children and, as a result, populations are aging. Japan is furthest ahead in this trend, followed by Europe, with America headed in the same direction, just further behind.

Possible Diagnoses and Corresponding Treatments

1. Mismeasurement

The first possible diagnosis is mismeasurement of GDP: Perhaps the economy is growing more quickly than we realize because innovation is increasingly taking place in sectors that are hard to accurately measure, such as information technology and health care. It is hard for economists to capture the fact that apps like Google Maps are tremendously valuable to consumers, yet don’t cost them anything. Or that new medical treatments that cost the same as older treatments are helping people live longer than they did before. Could such mismeasurement be increasingly happening at a scale that would account for a significant share of the measured slowdown in growth? It’s not impossible, but it doesn’t seem likely to me. It’s hard for me to see how this diagnosis could explain the slowdown in U.S. investment and the falling neutral real interest rates globally. And, unfortunately, there isn’t an obvious policy response for this diagnosis even if we thought it were right. Government economists are always working to improve national economic statistics. They should continue that work regardless of current economic conditions.

2. Slowdown in Innovation

The second possible diagnosis is a slowdown in the rate of innovation, or perhaps in the usefulness of the innovations developed in recent years. This theory was put forward by Northwestern University economist Robert Gordon, who argues that the major technology breakthroughs of the past (running water, the internal combustion engine, the airplane, electricity, the integrated circuit) dwarf modern innovations such as social media and email. It’s hard for me to argue against that view. I doubt Twitter and Facebook are net productivity enhancers. Nor is Pokémon GO. (Note: I am fairly active on Twitter, so can speak with some authority.) My view is that the technologies powering the sharing economy (such as Uber and Airbnb) likely do enhance productivity by increasing the utilization of assets such as cars and homes, but, again, they are trivial compared with the introduction of electricity. In short, current innovations seem to me much less likely to generate the type of future growth that we enjoyed from past innovations.

The strongest argument against this view is that no one knows what technology breakthroughs are around the corner. That is true, and I certainly hope there is some revolutionary new technology we are all about to benefit from. But rather than just hoping, is there anything policymakers can do to increase our chances?

Here are four categories of policy responses that could increase the rate of innovation in our economy, but they all work on a time scale of years or even decades and would need to be implemented and maintained for many years to show results. That’s the nature of technology development: It is virtually impossible to predict, and real breakthroughs are difficult.

-

Increase government funding of basic research. The U.S. government currently funds approximately $33 billion per year of basic research via agencies such as the National Science Foundation, National Air and Space Administration, National Institutes of Health and Defense Advanced Research Projects Agency10—less than 0.2 percent of the total economy (GDP). Even a doubling of government-sponsored basic research is small compared with other spending programs such as proposals to increase infrastructure investment (see Secular Stagnation below).

-

Improve education. It is well-understood that a highly skilled workforce is more innovative than a low-skilled workforce. Myriad education reforms are being tried across the country that show promise, from early childhood education to K-12 reforms to more access to higher education and innovative delivery models via technology. Improving education will help not only the students who benefit directly, but also the economy as a whole. Importantly, not all of these reforms require increased spending.

-

Increase high-skilled immigration. In addition to improving the skills of our own workforce, attracting the most talented people from around the world has been a competitive edge for the United States over the past century. According to the nonpartisan National Foundation for American Policy, 51 percent of all billion-dollar high-tech start-ups in America were founded by immigrants.11 Reforming immigration laws to make it easier for high-skilled immigrants to come to America, and for immigrants who receive advanced training to stay here, should lead to a higher economic growth rate and more jobs here at home.

-

Reduce barriers to investment and migration. A number of barriers make it harder for the economy to adjust to and take advantage of changes in the marketplace, which impedes economic growth. For example, some land-use policies make it challenging for workers to move to higher-growth regions where their skills might be put to better use. There are also barriers to new business formation. Measures of job reallocation and firm dynamism in the United States have fallen since before the Great Recession.12 Some of these frictions are imposed at the local and state level, making them harder to fix nationally but nonetheless worth pursuing.

3. Secular Stagnation

The third possible diagnosis is secular stagnation, as recently put forward by another Harvard professor, Larry Summers. He argues that the economy is essentially stuck in a low-growth mode, driven by a convergence of demographic trends, technological changes and frictions in the economy, leading to inadequate aggregate demand. Given the nominal zero lower bound, interest rates can’t fall far enough for saving and investment to balance, and we end up with excess savings, insufficient investment and no automatic way to bring them into balance. There are at least three broad categories of policy responses to secular stagnation: more government spending, an increased supply of safe assets and a new monetary policy framework.

-

Increase government spending on infrastructure. Advocates for the secular stagnation hypothesis see a shortage of aggregate demand, and given that government borrowing costs are at record lows, they recommend that the government issue more debt to fund more spending. Infrastructure investment in airports, mass transit and so on is usually at the top of the list. The conventional wisdom is that U.S. infrastructure is terrible, a view so pervasive that I find myself saying it too. In fact, in my 43 years, I can’t remember a time when I didn’t hear how underinvested we are in infrastructure; I remember hearing this in elementary school. Is it really true?

I have lived across much of our country: Ohio, Illinois, Pennsylvania, Maryland, throughout California and now Minnesota. Everywhere I have lived, I’ve been within 45 minutes of an airport where I could travel anywhere in the world. I was always able to drive wherever I needed to go on pretty good roads. Yes, many cities have bad traffic, but name a large city in the world that doesn’t. Yes, some countries’ airports are palatial. But are palatial airports necessary to support a strong economy, or are good airports good enough? It doesn’t seem like traffic and nonpalatial airports are reliable indicators of an infrastructure system that is impeding economic growth. I think those examples illustrate why it is hard to reach consensus on new infrastructure projects.

What seems clearer to me is that we do have significant deferred maintenance of our existing infrastructure that must eventually be addressed. The American Society of Civil Engineers estimates that infrastructure investment of $3.3 trillion is needed between now and 2025.13 As an engineer myself, I know engineers are as good as anyone at advocating for their own self-interest. So if we apply an engineer’s adjustment to the engineers’ estimate and divide it by pi, we still have a need of more than $1 trillion to maintain our existing infrastructure. There doesn’t seem to be much downside to such investment, since we will need to do this anyway and borrowing costs are at record lows today.

-

Increase the supply of safe assets. There is an argument that the increase in demand for safe assets around the world has created a chronic lack of demand for goods while pushing down the natural real rate and lowering nominal rates to zero across the developed world. A potential policy response could be for the government to increase the supply of those assets by increasing the amount of U.S. government debt outstanding. Rather than using the proceeds from such issuance to fund spending (such as infrastructure noted above), it could be invested in financial assets in what would essentially be a U.S. sovereign wealth fund. This policy option raises many questions about what risks U.S. taxpayers would be exposed to and how investment allocations would be decided.

-

Raise the inflation target. Given the constraint of the effective zero lower bound, the Federal Reserve can’t lower short-term real interest rates much further through open market operations and asset purchases. The primary way to meaningfully lower real rates from here is to raise inflation expectations, and some academics and policymakers are advocating for consideration of raising the inflation target (from 2 percent to, say, 3 percent) or changing from an inflation target to a price level or nominal GDP target. These are all ways of trying to raise inflation a modest amount or for a limited period of time without losing control of inflation and having expectations take off. If these policies were successful, they would have the effect of lowering real interest rates, which are the rates that ultimately matter for investment, thus stimulating the economy further.

However, there are significant downside risks with these policy recommendations that I believe must be carefully considered before being adopted. First, the Federal Reserve is struggling to hit its current target of 2 percent and has come up short for four years. Market forecasts and expectations about our ability to hit 2 percent have fallen. If we announced a new higher target, it isn’t clear why anyone would believe that we could hit it. The Federal Reserve’s credibility could be weakened. To say it another way: Had Japan announced a higher inflation target a decade ago, would it have made much difference? I doubt it, because Japan too faces nonmonetary challenges.

Second, a number of important questions about the efficacy of addressing low growth right now with a change in the inflation target must be understood. For example, it takes several years or even a decade or more to anchor inflation expectations. If we announced a new target, it might take years or more for the target to sufficiently anchor expectations at the new level and have the desired effect of easing monetary conditions. That’s an enormous policy lag. By the time it had its desired effect, the economic environment might be very different. Would policymakers at that future date want to stick with the new target? What if economic conditions at that time called for a different target? Should policymakers update the target regularly? How effective an anchor would an adjustable target be?

4. Psychological Scarring from the Crisis

The fourth possible diagnosis is psychological scarring from the crisis. The 2008 financial crisis was global in nature, and it is very possible that people around the world who lived through the crisis, myself included, remember how frightening it was and better understand that major negative economic shocks are possible, especially when times seem good. Scarring affects people’s willingness to take risks: to borrow to buy a house or a car, to change jobs, to start a new business. I have increased my own savings as a result of the crisis and now pay down debt as fast as possible. Scarring can last years or, some argue, even a lifetime.

Whether this is a public policy problem is unclear. If the scarring is not irrational, but is a more accurate assessment of economic risks, then such a change in behavior could be prudent and good for the economy in the long term. Perhaps we were underappreciating the risks before the crisis, leading to too much spending and not enough savings. However, if the scarring is irrational—people like me, potentially millions of us—are simply being too risk averse, then it could explain some of the reduced investment, slow growth and low interest rates we are seeing around the world. It is hard to know what is right, and even harder to design policy solutions for this diagnosis. Policies to mitigate systemic risk could help people have more confidence that big downside shocks are less likely. Regulators’ (and the Minneapolis Fed’s) work to address too big to fail could help, but it’s hard for me to see them fundamentally changing the risk tolerance of consumers and investors in the near term. Perhaps a positive psychological shock could come from some new technological breakthrough or human achievement (such as the moon landing in the 1960s), but these would be exceptionally difficult to predict. It’s a little like hoping for a miracle cure.

5. Changing Demographics

As noted above, aging workforces and slowing population growth are important contributors to lower economic growth. A number of demographic trends in the United States are working against strong economic growth: The baby boom generation is beginning to exit the workforce and head into retirement. Our workforce grew in part from women entering it in large numbers over the past few decades, but that growth is tapering off and likely won’t be a big contributor going forward. Also concerning is that men have increasingly been leaving the workforce for reasons not fully understood. The one strong positive for the United States is that immigration has helped offset some of those challenging demographic trends. Our attractiveness as a destination for immigrants has been a key advantage we have had relative to most other countries, helping our workforce and populations to continue to grow more quickly than those of other advanced economies. However, since the financial crisis, immigration into the United States has slowed, reducing some of that advantage.

Some question whether these trends are really concerning at all: People are living longer, and women are now big contributors in our workforce. Maybe we are just adjusting to a new demographic equilibrium. In fact, we do not really know how an aging population may affect the ability of an economy to keep innovating and improving the living standards of its citizens. More research is needed in my view but, assuming we want to return to a growing workforce and population, is there anything policymakers can do about it?

-

Correct remaining disincentives to work generated by welfare programs. Proposals exist to update welfare and disability insurance programs to provide help to those who need it while encouraging those who can work to do so. Programs such as the earned income tax credit are designed to achieve those objectives, and proposals have been put forward to update and expand them.

-

Increase the population growth rate. There are two ways to achieve this goal: (1) Offer families incentives to have more children. Some other advanced economies have implemented a range of policies, such as tax incentives, subsidized child care and generous family leave policies to accomplish this. These policies likely require significant long-term spending to be effective. (2) Reform immigration policies. Broad immigration reform that provides our economy the workers and the consumers it needs could support economic growth and offset the challenging demographic forces we face.

6. Policy Mistakes

Some have argued that regulations and poorly designed policies are holding back economic growth. For example, complex tax policies that discourage investment, overlapping and inconsistent federal and state regulations that drive up costs for businesses and drive down productivity, and uncertainties about the regulatory policy environment going forward are all possible contributors to the slow economic recovery. One counterpoint to this view is that these policies are local to the United States. Poor tax or regulatory policies in the United States can’t explain the low growth, low inflation and low productivity that many advanced economies around the world are experiencing at the same time. Nonetheless, improving the tax and regulatory environment in the United States should help improve economic competitiveness and growth over time.

-

Improve the tax code. Simplifying the tax code and making it more consumption-oriented (while still preserving its progressivity) could boost incentives to invest in new equipment and technologies.

-

Reduce the costs of regulatory compliance. Rationalizing overlapping and inconsistent regulations could improve productivity. Eliminating needless licensing could help new businesses form and help more workers find better jobs at higher wages.14

Neither of these policies has meaningful downside risks. While the specifics may be hard to reach consensus on, they are nonetheless sensible for policymakers to consider. However, it is unclear how easily policymakers today could reduce uncertainty about the future policy environment.

7. Debt Overhang

The final possible diagnosis is that we are experiencing a debt overhang. Some argue that the high consumption and aggregate demand growth the United States enjoyed leading up to the crisis was driven in part by increasing accumulation of debt and increasing borrowing from abroad—a process that proved unsustainable. Even with record low interest rates, businesses and consumers understand that eventually the debt they borrow has to be paid back, so they are reluctant to take on even more. Such an overhang could explain some of the lower investment and higher savings rates we are seeing in the United States. A counterargument is that debt levels for homeowners, for example, are much more manageable today than a few years ago as home prices have bounced back, so the potential benefits of addressing this issue would not be as strong now.15

The policy options to deal with this potential diagnosis include the following:

-

Increase inflation to reduce debt burden. This is a policy that could do serious harm to the long-term health of the U.S. economy by weakening the independence and credibility of the Federal Reserve. A surprisingly high inflation rate would reduce the burden on current borrowers, but it comes at great cost in terms of the ability of the Federal Reserve to achieve low and stable inflation in the future.

-

Write down private sector debt. The cost of such a program could be very large, and it would likely be difficult to reach agreement on who would fund any such write-downs.

Conclusion

We have come up with seven diagnoses and, like Mankiw, we don’t know for sure which ones are right. But looking at the symptoms, both domestic and global, suggests to me that we are likely seeing a confluence of three fundamental causes all combining to slow the economic recovery: (1) challenging demographics, (2) psychological scarring from the crisis and (3) lackluster technological innovation. Unfortunately, these headwinds aren’t likely to reverse anytime soon on their own.

The good news is that we, as a country, aren’t powerless to address these fundamental causes. We have identified a series of policy responses that could be effective over time and have little downside risk.

An obvious way to spur innovation and entrepreneurial activity is to increase government funding of basic research. Another promising policy is immigration reform, especially for high-skilled workers. Over the longer term, policies that improve education, streamline regulations and make the tax code more efficient should allow the United States to retain its dynamism, creativity and willingness to take risks.

Given today’s low borrowing costs, there is a strong case for increased government spending on deferred maintenance of infrastructure that will be necessary to sustain our economy. However, I am skeptical that a large-scale expansion of government spending by itself is the best way forward, since larger fiscal deficits will lead to higher expected future taxes, which could further undermine private sector confidence. Chronically weak demand might have been an important part of the diagnosis for the U.S. economy in the depths of the recession, when many workers and factories were idled. By 2016, however, the labor market appears closer to normal, which limits how much can be achieved by boosting demand to increase employment further.

We at the Minneapolis Fed will continue to look for evidence to confirm which diagnoses are right and to consider additional policy solutions (both monetary and nonmonetary) that could help improve economic growth over the medium and long term. It is important that all parts of our government use their respective tools to improve economic outcomes for the country. I wrote this earlier, but it is worth repeating: Small changes in a country’s long-term growth rate result in enormous changes in outcomes for its people.

Endnotes

1 See Mankiw 2016.

2 I thank the entire Research Department of the Minneapolis Fed for feedback as we explored the issues discussed in this essay. I especially thank Manuel Amador, Javier Bianchi, Ron Feldman, Terry Fitzgerald, Jonathan Heathcote, Jim Lyon, Jenni Schoppers and David Wargin for their specific contributions. The views presented here are my own and not necessarily those of the Federal Open Market Committee or the Federal Reserve System, and I take responsibility for any errors in this essay.

3 The Conference Board Total Economy Database provides one measurement of slower productivity growth. The May 2016 Summary Tables document the notable decline in output per person in the United States and “Other Mature Economies.” For example, labor productivity fell from 2.4 percent in 1999-2006 to less than 0.5 percent in 2013-2015. For the same time periods, productivity fell from 1.5 percent to 0.6 percent for the euro area and 2.9 percent to 1.2 percent in “Other Mature” economies (see table 5).

4 See Bean et al. 2015.

5 Holston, Laubach and Williams (2016) document large declines in trend GDP growth and natural rates of interest that have occurred over the past 25 years in Canada, the United States, the United Kingdom and the euro area economies.

6 Private domestic investment as a share of GDP fell to 13 percent in 2009 and slowly increased to 16.9 percent in 2015. This compares to an average investment share of 18.2 percent in the 30 years prior to the Great Recession.

7 The personal savings rate has averaged 6 percent over the last five years compared to 4.2 percent for the decade prior to the Great Recession.

8 See Haltiwanger 2015.

9 For example, the compensation component of the Employment Cost Index for civilian workers has averaged 2 percent annual growth over the last five years compared to 3.6 percent growth in the decade prior to the Great Recession.

10 See documentation at https://www.whitehouse.gov/sites/default/files/omb/budget/fy2017/assets/ap_19_research.pdf.

11 See policy brief at http://nfap.com/wp-content/uploads/2016/03/Immigrants-and-Billion-Dollar-Startups.NFAP-Policy-Brief.March-2016.pdf.

12 See Haltiwanger 2015.

13 See the press release at http://www.asce.org/templates/press-release-detail.aspx?id=20935.

14 See Kleiner and Krueger 2013.

15 For example, the percentage of mortgaged homeowners underwater has fallen notably over the last four years. See the report at http://www.zillow.com/research/q2-2016-negative-equity-report-13046/.

References

Bean, Charles, Christian Broda, Takatoshi Ito and Randall Krozner. 2015. Low for Long? Causes and Consequences of Persistently Low Interest Rates. Geneva Reports on the World Economy.

Haltiwanger, John. 2015. Top Ten Signs of Declining Business Dynamism and Entrepreneurship in the U.S. Kauffman Foundation New Entrepreneurial Growth Conference. Online at http://econweb.umd.edu/~haltiwan/Haltiwanger_Kauffman_Conference_August_1_2015.pdf.

Holston, Kathryn, Thomas Laubach and John C. Williams. 2016. Measuring the Natural Rate of Interest: International Trends and Determinants. Working Paper 2016-11. Federal Reserve Bank of San Francisco. Online at http://www.frbsf.org/economic-research/files/wp2016-11.pdf.

Kleiner, Morris, and Alan B. Krueger. 2013. Analyzing the Extent and Influence of Occupational Licensing on the Labor Market. Journal of Labor Economics 31 (2): S-173-S202.

Mankiw, N. Gregory. 2016. One Economic Sickness, Five Diagnoses. New York Times, June 17. Online at http://www.nytimes.com/2016/06/19/upshot/one-economic-sickness-five-diagnoses.html?_r=0.