Authors

Jing Zhang

Federal Reserve Bank of Chicago

Economic Policy Papers are based on policy-oriented research produced by Minneapolis Fed staff and consultants. The papers are an occasional series for a general audience. The views expressed here are those of the authors, not necessarily those of others in the Federal Reserve System.

Executive Summary

Long-term interest rates have a crucial influence on virtually all major financial decisions faced by households, businesses and governments. This paper reviews several decades of data on long-term rates internationally, explores several factors that determine them and discusses implications of this evidence.

The data indicate declining long-term rates since the 1980s, converging internationally at very low levels. This implies that the rate decline is not due to the Great Recession or to the early 2000s downturn. It further suggests a higher likelihood than before of hitting the zero bound on nominal interest rates as well as sustained rate convergence as global financial integration proceeds.

Furthermore, evidence of a downward trend in global fixed investment, coupled with the main finding of declining long-term interest rates, suggests that forces leading to declining global investment demand may be more important than those leading to increased saving in explaining current trends in long-term rates.

Introduction

The single most important price in an economy may well be the real (inflation-adjusted) interest rate. It affects household decisions on mortgages and car loans, shapes business choices on building factories and investing in capital and influences both fiscal and monetary policymaking. In short, the real interest rate is a critical factor in almost every decision faced by households, businesses and governments about whether to spend now or later.

This policy paper provides a short review of data on long-term real interest rates and highlights two key forces that help determine them. A follow-up paper provides a deeper exploration of underlying determinants .1

This initial review of data and determinants shows that long-term real interest rates have declined since the 1980s—nearing their 60-year low—and that rates have converged among major economies. This indicates that rates were declining well before the Great Recession as well as the 2001 recession and suggests a higher likelihood of reaching the zero lower bound than predicted prior to the Great Recession. The sustained increasing rate trend prior to the 1980s, however, shows that the current pattern could reverse. Finally, evidence of a downward trend in global fixed investment since the 1980s, coupled with declining interest rates, suggests that forces leading to a decline in investment demand have been relatively more important in determining rates than factors leading to increased desired saving (i.e., global saving glut).

Background

The real interest rate is determined by a number of underlying forces. Some of these are transitory and have relatively short-term influence on interest rates. These include movements in oil prices, shifts in monetary and fiscal policy, and wage adjustment. Other factors are more fundamental, and these are of greater interest to policymakers (and economists) because they determine the long-run real interest rate. Estimates of the long-term rate are important to fiscal policymakers when they determine the optimal amount and maturity structure of government debt issuance each year.

The long-term rate is also important for monetary policymaking. In the United States, a key Federal Reserve policy tool is the federal funds rate, the rate it charges banks for overnight loans. Estimates of the long-term real interest rate help policymakers in determining the optimal fed funds rate. They also help economists understand the implications of monetary policy models, such as the Taylor rule, and can shed light on the probability of hitting the zero lower bound in the long run.

This paper presents evidence on the long-run behavior of real interest rates for 20 countries over periods as long as 60 years, reviews a simple framework to highlight two key forces behind long-run rates and then provides evidence on these two factors.

Evidence on long-run real interest rates

This section presents estimates of the long-run real interest rates for up to 20 countries between 1955 and the present. These include the world’s largest economies, measured by 2014 dollar GDP. (See appendix for list and dates.) Our measure of the long-run real interest rate is the long-run average of the real interest rate on a short-term (risk-free) asset.2

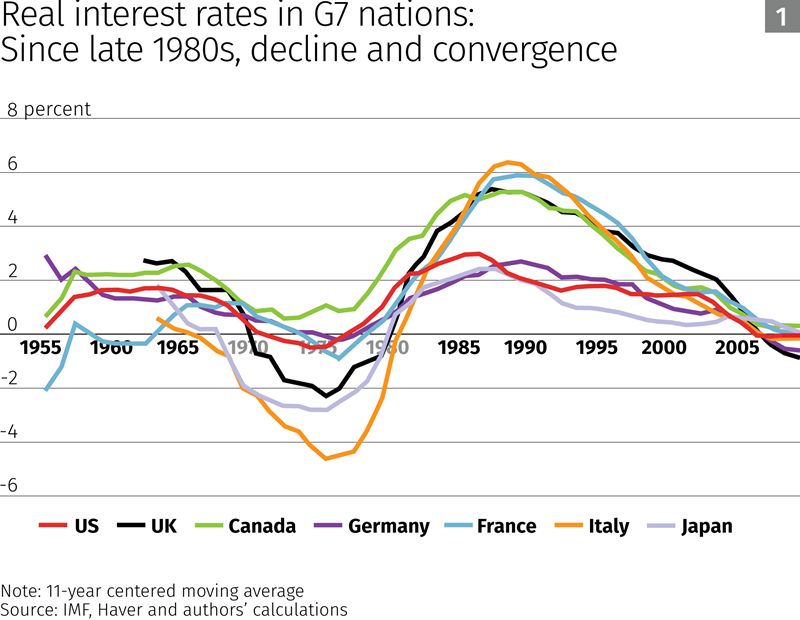

Figure 1 presents long-run real interest rates for the G7 countries. Two patterns are apparent. First, G7 real interest rates are now quite close to each other, especially in recent years. Second, there have been three broad trends since the early 1960s: (a) a decline extending until the mid-1970s, (b) an increase until the late 1980s, (c) a decline since the late 1980s.3

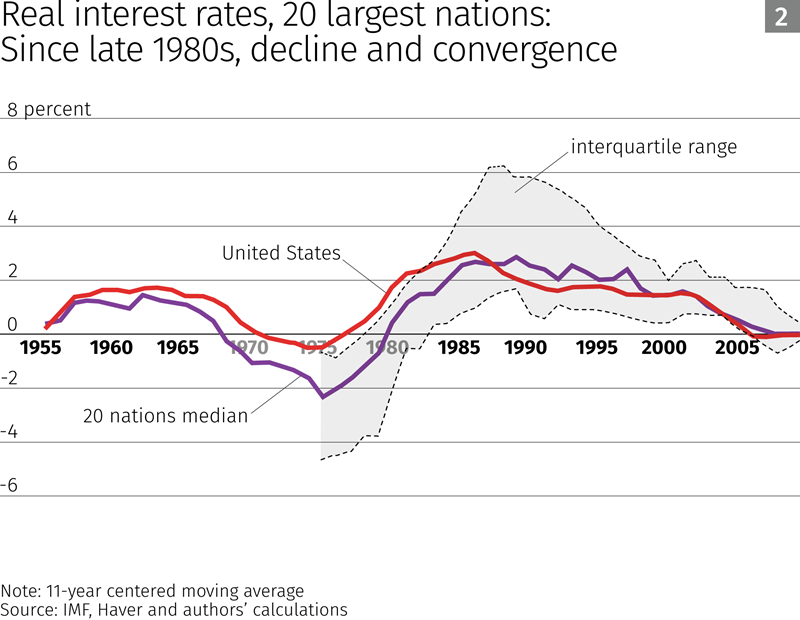

Figure 2 shows the median (purple line) of the long-run real interest rates across our full sample of countries for each year.4 The median follows the same three broad trends as the G7 nations: decline to the mid-1970s, rise until the late 1980s, followed by decline. The median closely tracks the U.S. rate (red line). The magnitude of the trend movements in the median is quite large—on the order of 4 percentage points from its low to its high. The shaded area (between the two dashed lines) shows the interquartile range for the period 1975 to the present; this range has declined substantially since the late 1980s from about 5 percentage points to about 1 percentage point.

Conceptual framework for long-run real interest rates

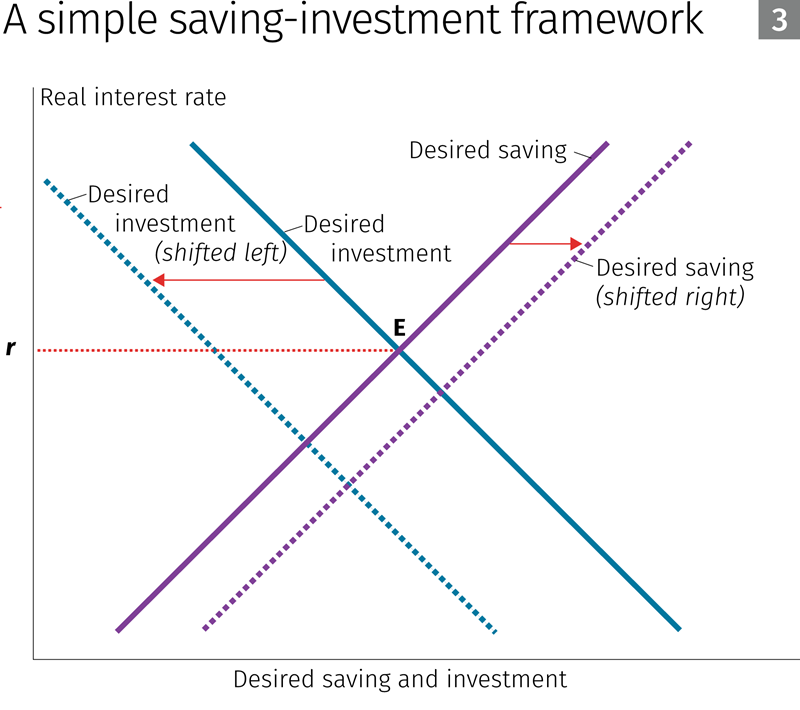

Many of the main forces affecting the long-run real rate can be highlighted with a textbook saving-investment framework that describes supply and demand curves for funds.

Figure 3, a simple diagram of saving and investment curves, shows that desired saving and investment are, respectively, positively and negatively related to the real interest rate. That is, people will want to save more at higher interest rates and invest more at lower interest rates. The real interest rate that leads desired investment to equal desired saving is the intersection of these curves: the equilibrium real interest rate (r).

In the global context—and in the absence of frictions such as information asymmetry or restrictions on capital flows—there will be a single (risk-adjusted) real interest rate that clears the global market for saving and investment. Fundamental forces that change global desired saving and desired investment will shift the relevant curves, thus leading to a new equilibrium interest rate.

One fundamental saving force is the “global saving glut” hypothesis offered by former Fed Chairman (then Governor) Ben Bernanke (2005). In that story, the Asia financial crisis and increased earnings by oil-producing nations increased desired saving by many emerging-market countries. In Figure 3, this would show up as a shift of the saving curve to the right, leading to lower long-run real interest rates, higher equilibrium investment and saving and, as a byproduct, increased capital inflows into countries like the United States. A second, related example is the increased integration into the global economy of high-growth, high-saving and financially underdeveloped economies like China. Its high desired saving rates coupled with a shortage of domestic saving instruments exceeds profitable investment opportunities in these economies, thus leading to a lower equilibrium interest rate in the advanced economies.5

Many forces can shift desired investment as well. For example, if the productivity of (future) capital decreases, desired investment will decrease: The curve shifts to the left. Also, if the perceived riskiness of capital expenditures increases, all else equal, this will lower investment demand, and the curve will shift left.

Evidence on global saving and investment

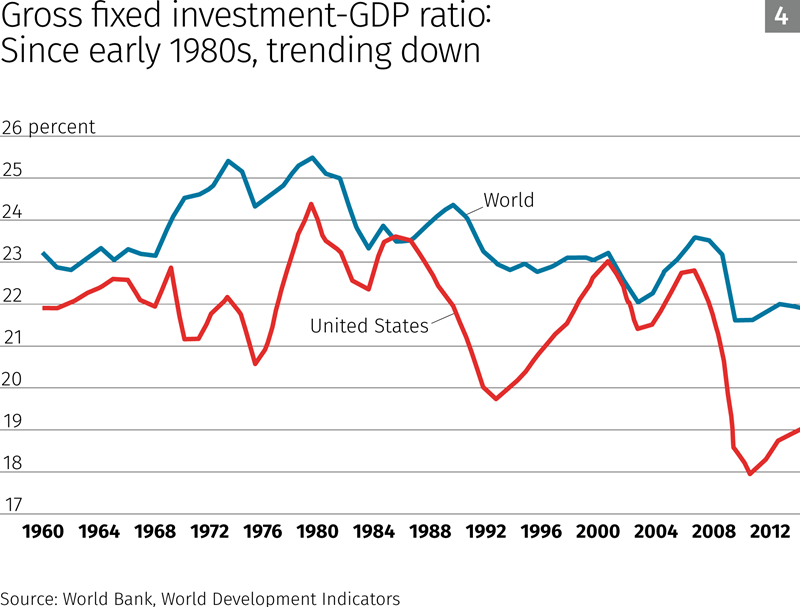

Turning from measures of interest rates to the equilibrium amount of saving and investment, Figure 4 shows the global gross fixed investment-to-GDP ratio from 1960 to the present.6 The U.S. ratio is included for comparison. The figure shows a broad increase in the global ratio until the late 1970s and a fairly steady decline since then. One exception is the early 2000s, when it increased, consistent with the global saving glut hypothesis. The United States has a similar pattern, although the recent decline is more pronounced. The overall declining trend since the early 1980s, coupled with the declining trend in long-run interest rates since the late 1980s, suggests the importance of a downward shift in the global investment demand curve.

Summary and conclusions

Real interest rates since the 1960s have been characterized by three broad long-run trends: (1) rates have declined across numerous countries since the 1980s, (2) long-run average real interest rates are near their low for the 60-year period we examine and (3) over the past quarter century, long-run interest rates have converged internationally, consistent with an increasingly financially integrated world.

These findings have four implications.

First, real interest rates were declining long before the global financial crisis of 2007-09 and its aftereffects and well before the fizzling of the IT boom.

Second, the likelihood of nominal interest rates hitting the zero lower bound has increased compared with the likelihood prior to the Great Recession.

Third, increasing financial integration may lead to even closer international rate convergence.

Fourth, there was a sustained increasing trend in long-run real interest rates prior to the 1980s, which suggests that the current downward trend could also reverse.

Finally, since the 1980s, the trend in global fixed investment is downward. Coupled with our main finding of the declining long-run real interest rates, this suggests that forces leading to lower investment demand have been relatively more important than those leading to increased desired saving. Put differently, while our evidence is not inconsistent with the global saving glut hypothesis, it indicates that in addition to a saving glut, there must have been forces that reduced global investment demand, and these forces must have been more important.

Appendix

Construction of long-run real interest rates

We follow the procedure of Hamilton et al. (2015). We use annual interest rate data. Our nominal interest rate variable is typically the central bank policy rate at the end of the year. For Brazil, France, Indonesia and Mexico, it is an annual average short-term market rate. For China, it is an end-of-year deposit rate. The interest rate data came from Haver or the International Monetary Funds’s International Financial Statistics (IFS).

We compute the inflation rate as the December-to-December consumer price inflation rate (for Australia it was the Q4/Q4 inflation rate). The price level data came from Haver or the IFS. For inflation expectations, since Atkeson and Ohanian (2001), it has been known that it is difficult to outperform a random walk inflation model in out-of-sample forecasts. For this reason, we set expected inflation next year as the inflation rate this year. The real interest rate equals the difference between the nominal interest rate and the inflation rate expected for the next year. To compute long-run real interest rates, we take 11-year centered moving averages.7

Country List

We study the 20 largest economies as measured in current dollar GDP, excluding Russia and Saudi Arabia owing to limited data. Our countries include Australia (1969-2014), Brazil (1980-2014), Canada (1950-2014), China (1985-2014), France (1950-2014), Germany (1950-2014), India (1963-2014), Indonesia (1970-2014), Italy (1958-2014), Japan (1958-2014), Mexico (1978-2014), Netherlands (1958-2014), Nigeria (1961-2014), South Korea (1956-2014), Spain (1958-2014), Sweden (1950-2014), Switzerland (1950-2014), Turkey (1970-2014), the United Kingdom (1957-2014) and the United States (1950-2014).

Endnotes

1 Part two will be published by the Federal Reserve Bank of Chicago. Several recent papers also discuss this long-run interest rate downturn. See, for example, Hamilton et al. (2015), Holston, Laubach and Williams (2016) and Obstfeld and Tesar (2015).

2 To be clear, this is distinct from the “real long-term rate,” which is the real return on long-term bonds. The main rationale underlying this concept is that movements in real interest rates owing to sluggish adjustment of prices and wages, as well as short-run movements in productivity, oil prices, monetary and fiscal policy, and other forces, “wash out” over time, leaving only trends in fundamentals driving the real rate over the long run. This concept is time varying, and it attempts to capture something that is inherently unobservable and thus must be inferred by statistical and/or economic methods. Our methodology for measuring these real interest interests broadly follows Hamilton et al. (2015). See appendix for details.

3 Hamilton et al. (2015) and Obstfeld and Tesar (2015) also document these trends.

4 The number of countries is not constant in each year. This applies to all subsequent charts with medians and interquartile ranges.

5 Caballero et al. (2008) and Mendoza et al. (2009) develop formal models of this story. A third example of a global saving force is that, as a consequence of the Great Recession, there has been a persistent or even permanent increase in uncertainty, which could induce, for precautionary reasons, increased desired saving. This force would also shift the long-run desired saving curve to the right—also leading to lower long-run real interest rates.

6 Gross fixed investment includes private and government fixed investment. The global ratio is constructed by calculating a weighted average of each country’s (nominal) fixed investment-GDP ratio, where the weights are based on nominal GDP using current market exchange rates.

7 We assume that 11 years is long enough for short- and medium-term shocks to die out. To the extent that shocks are long term or permanent, averages of past data may not be the best metric for future long-run real interest rates.

References

Atkeson, Andrew, and Lee E. Ohanian. 2001. Are Phillips Curves Useful for Forecasting Inflation? Federal Reserve Bank of Minneapolis Quarterly Review (Winter): 2-11.

Bernanke, Ben. 2005. The Global Saving Glut and the U.S. Current Account Deficit. Speech at the Sandridge Lecture, Virginia Association of Economists, Richmond, Va., March 10.

Caballero, Ricardo J., Emmanuel Farhi and Pierre-Olivier Gourinchas. 2008. An Equilibrium Model of “Global Imbalances” and Low Interest Rates. American Economic Review 98 (1): 358-93.

Hamilton, James, Ethan S. Harris, Jan Hatzius and Kenneth D. West. 2015. The Equilibrium Real Funds Rate: Past, Present and Future. Manuscript.

Mendoza, Enrique G., Vincenzo Quadrini and José-Víctor Ríos-Rull. 2009. Financial Integration, Financial Development and Global Imbalances. Journal of Political Economy 117 (3): 371-416

Obstfeld, Maurice, and Linda Tesar. 2015. Long-Term Interest Rates: A Survey. Manuscript. Washington: President’s Council of Economic Advisors.