Author

Despite years of research, the economic effects of unemployment benefits are poorly understood. While intuition (and some early studies) might suggest that providing financial aid to people who lose their jobs would discourage them from seeking new jobs, recent research has found that extending benefits has little effect at the individual level. But the impact on broader economic outcomes such as unemployment rates, employment levels, job vacancies and worker earnings is unresolved and—particularly in light of the Great Recession when benefits in the United States were extended from 26 weeks to as long as 99 weeks—highly contentious.

Some economists, like Harvard’s Robert Barro, have argued that by making unemployment relatively more attractive, generous benefits lowered job search efforts and had a negative impact on the economy at large by delaying the recovery of the labor market. Others, including former Treasury Secretary Larry Summers, have suggested that extending benefits would provide a significant economic stimulus by increasing incomes and spending.

Getting a solid answer to the question has proven difficult, however, in part because of a mechanical correlation between unemployment rates and unemployment insurance (UI) duration. Federal law dictates that the duration of benefits extends in periods of higher unemployment, which automatically creates a positive relationship between UI duration and the unemployment rate. Distinguishing between this legislated relationship and any possible economic effect that benefit extensions may have on macroeconomic outcomes is a challenge.

In “The Limited Macroeconomic Effects of Unemployment Benefit Extensions” (WP 733, April 2016; also NBER working paper 22163), Minneapolis Fed economist Loukas Karabarbounis and Harvard economist Gabriel Chodorow-Reich develop a novel empirical design and combine it with a standard labor market model to shed light on the policy question. They conclude that “the extension of benefits has only a limited influence on macroeconomic outcomes.”

Clever technique

To disentangle signal from noise—the actual macroeconomic effect of UI extension from the legislative artifact—the economists take advantage of the measurement error inherent in gauging unemployment rates. Real-time estimates of unemployment are often inaccurate and frequently revised as better data are gathered over time.

Consider Louisiana and Wisconsin. Louisiana’s April 2013 real-time estimate of the unemployment rate was 5.9 percent, allowing a 14-week extension of unemployment benefits. But by 2015, better data provided a more accurate estimate of 6.9 percent unemployment, meaning that the state’s unemployed should have received an additional 14 weeks, as they did in Wisconsin, which recorded 6.9 percent unemployment in both periods and provided a 28-week extension in April 2013.

The “UI error” seen in Louisiana versus Wisconsin reflects mismeasurement of the states’ economic fundamentals rather than actual differences “and, therefore, provides exogenous variation to estimate the effects of UI benefit extensions on state aggregates.” Such errors are common. From 1996 to 2014, Karabarbounis and Chodorow-Reich find over 600 cases in which duration of benefits using revised data differed from the actual duration resulting from real-time unemployment rate estimates.

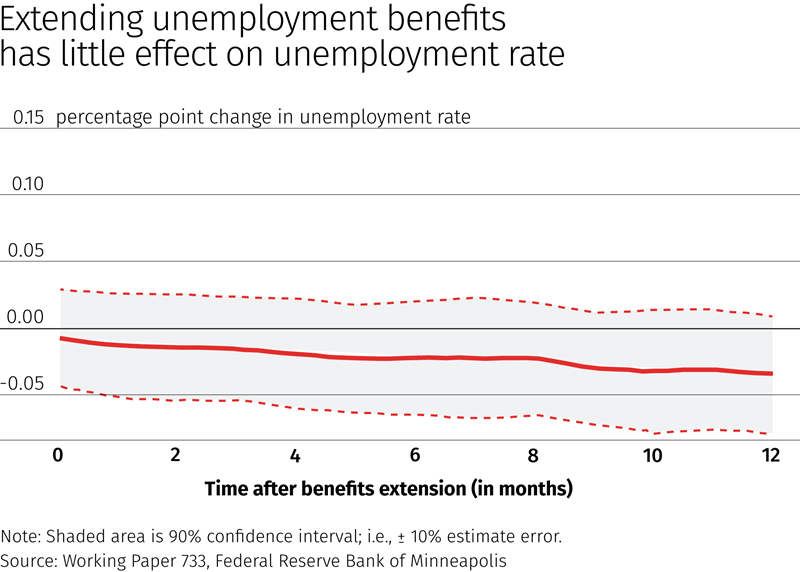

Using this data set, the economists estimate that a one-month extension in UI benefits “generates at most a 0.02 percentage point increase in the unemployment rate.” The accompanying figure illustrates this graphically, with the solid red line showing the unemployment rate change that UI extensions of increasing lengths are estimated to generate and the shaded area describing upper and lower bounds of those estimates.

The national debate over unemployment insurance has focused on a far longer extension, however, to nearly two years. Extrapolating the upper bounds of their estimates, the economists find that “extending benefits from 26 weeks to 99 weeks increased the unemployment rate by at most 0.3 percentage point.” Estimated effects on other macroeconomic variables such as the fraction of workers claiming UI, job vacancies, employment levels, labor force participation and earnings showed similarly negligible effects from UI extensions. “Collectively, these results provide direct evidence of the limited macroeconomic effects of increasing the duration of unemployment benefits.”

Why so small?

The economists move beyond this empirical analysis to understand why extending benefits seems to have such negligible influence. Using the standard labor market model developed by Diamond, Mortensen and Pissarides (DMP) in Nobel-winning research, augmented with an unemployment insurance policy, they conclude that low opportunity costs are probably the reason. “Viewed through the lens of a standard DMP model,” they write, “this small response is consistent with a low opportunity cost of giving up benefits for the average unemployed. A low opportunity cost means that even large extensions of benefits have limited influence on labor market variables.”

Other research on this topic, they point out, has assumed relatively high opportunity costs, but because the empirical results from this study suggest they’re quite low, it makes sense that UI extensions have little macroeconomic impact. “Together, our empirical and theoretical results imply that the unprecedented increase of benefits during the Great Recession contributed at most 0.3 percentage point to the increase in the unemployment rate.” While other economic factors and channels could play a role, they acknowledge, “our results simply suggest that concerns about large negative macroeconomic effects of UI are not warranted.” Nor, it would seem, are hopes that extending UI would provide much stimulus.