Authors

When there’s trouble on the farm, the producer’s banker is usually the first to know. Farmers and ranchers rely on banks to lend them money for planting crops, purchasing equipment and expanding their operations. When the agricultural economy takes a downturn, as it has in recent years owing to a drop in commodity prices, it’s a call to action for banks that provide credit to businesses and households in local communities.

As Ninth District producers struggle with income loss, community banks have taken steps to protect themselves, declining to extend credit to some operators with questionable capacity to repay loans.

But ag lenders are also working with financially strained producers to keep them in business by giving them more time to pay off loans or restructuring their debt. “Ag bankers are well aware that they need to stick by their borrowers and help them through the rough spots,” said Harold Wolle, president of the Minnesota Corn Growers Association.

In rural areas of the district, agricultural loans account for anywhere from 20 percent to 60 percent of the loan portfolio at community banks; commercial and consumer loans make up the remainder.

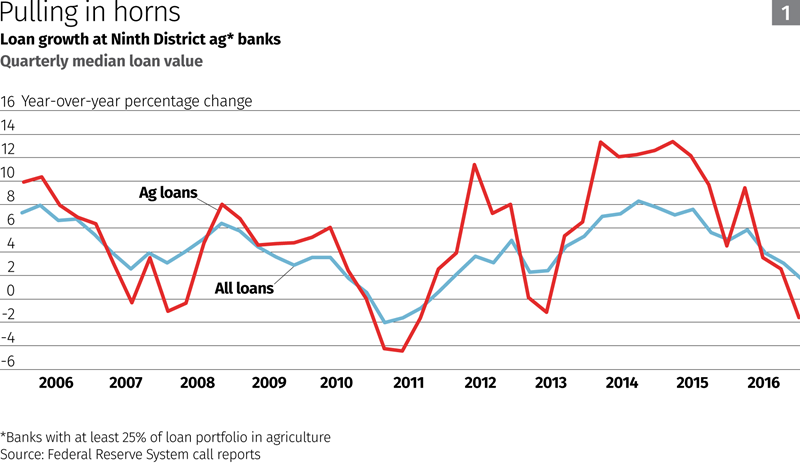

When commodity prices were high, ag producers borrowed freely to increase production and finance expansion. From 2011 to 2014, ag production lending—loans for operating expenses and purchases of machinery like tractors and hay balers—increased at district community banks with significant ag loan portfolios, according to data compiled by the Federal Reserve System (Chart 1).

Production loan value grew faster year over year than total loan volume at community banks—except in the first half of 2013, when growth in ag loans lagged that of overall loans and actually declined. A Midwest drought the previous year sent crop prices and profits soaring, likely reducing demand for farm credit.

Even as farm revenues and profits faltered in 2014, production debt kept rising—possibly due to producers failing to fully pay off their annual operating loans. But since then, farm lending has slowed markedly; in the last quarter of 2016, production debt declined at district banks relative to the same period the previous year. Nationwide, farm lending by community banks has followed a similar downward slope.

Much of this slowdown in ag lending likely stems from lower demand from producers under pressure to cut costs (see Trouble on the Farm).

“Farmers are pulling in their horns,” said Lynn Schneider, president of American Bank & Trust, a community bank with offices in Sioux Falls and seven other locations in central and western South Dakota. “They’re not making the capital-type investments—new buildings, new big tractors and combines. The demand for loans for that has really backed off because they don’t have the cash flow and income to make the payments.”

But there’s anecdotal evidence that loan growth has also cooled because banks are exercising greater caution in lending to the distressed farm sector. “To be honest with you, we’ve been more careful … we’ve tightened it up, made it a little harder [to borrow],” said Peter Scheffert, vice president of commercial and ag business for Community Resource Bank in Northfield, Minn.

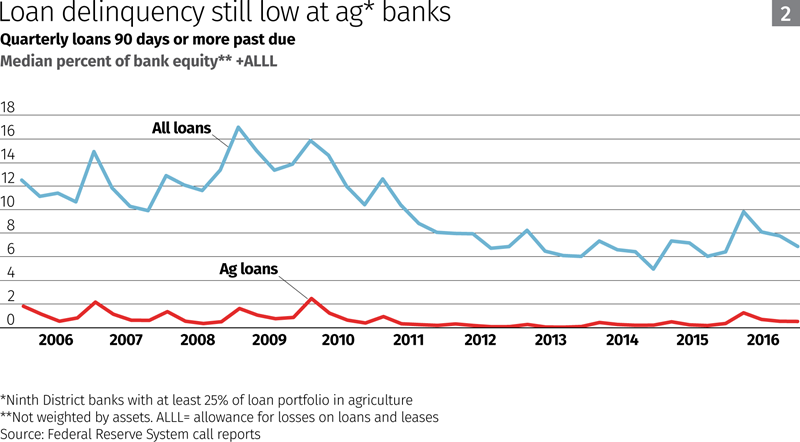

The signs of declining credit health in farm country are subtle yet widespread. Delinquent farm loans haven’t increased much in recent years, and in the last quarter of 2016, rates of ag loans over 90 days past due remained well below rates for all loans at district community banks (Chart 2). But in a fourth quarter survey of 77 district ag lenders by the Minneapolis Fed, 46 percent of respondents said demand for loan renewals and extensions had increased compared with the same period in 2015, and 56 percent said loan repayment rates had declined year over year.

Several bankers interviewed for this story reported an increase in voluntary liquidations—producers selling off assets in order to repay debt. “We’ve had some farmers who have sold some land or some machinery,” Scheffert said. “They could just see the writing on the wall. The best way to deal with too much debt is to sell something, pay down on that debt and live to farm another day.”

And state mediation of disputes between ag debtors and lenders has increased in several district states. In South Dakota, requests for mediation through the state Farm Loan Mediation program more than doubled from 2014 to 2016.

An eye on cash flow

Community bankers are more attuned to ag borrowers’ financial condition than they were a generation ago, when common underwriting practice was to lend on the strength of a farmer’s collateral—land, machinery or animals pledged to support the loan. In the 1980s farm bust, many producers lost their livelihoods to foreclosure when commodity prices crashed and they failed to make good on their debt obligations.

These days, most banks lend on the basis of a producer’s cash flow; loan officers closely monitor their customers’ revenues and expenses to ensure that they have the means to take on new debt or repay their existing loans. Collateral is a secondary form of repayment.

Miles Hamilton, president of Independence Bank in Havre, Mont., said the bank prides itself on being a cash-flow lender to customers, many of them farmers in north-central Montana who have been hit hard by low wheat prices. “We want to see a cash flow that works, because we think that’s in their best interests, and obviously it’s in the bank’s best interest, too.”

This principle has led community banks to take a proactive approach to managing debt in an unforgiving economic landscape for farmers. Banks are taking steps to both reduce the risk of financial loss and maintain long-standing relationships with ag borrowers by easing their debt burden.

Community banks typically manage their ag portfolios on a case-by-case basis, weighing the assets, liabilities and credit of each customer in deciding whether to offer or renew a loan.

Slumping commodity prices have swelled the ranks of producers in dire financial straits—often younger, less established farmers who have drawn down their working capital—and these borrowers are more likely to be denied credit.

Many community banks have also declined to lend to new ag customers with anything less than a rock-solid balance sheet. “We look for new-customer financials to be very strong as a qualification to begin a banking relationship,” said Schneider of American Bank & Trust.

However, a banker who sees a way forward for current borrowers in arrears or at risk of default is likely to work with them to iron out cash-flow problems and help them get back on track.

Showing forbearance by allowing the borrower to delay a payment for a few weeks or months is common. The bank may also opt to reamortize a loan—stretching out repayment over several years on the assumption that the producer will be in a better position to pay off the loan in the future. Sometimes a one-year operating loan is combined with a three- to five-year machinery loan to consolidate debt and extend the repayment schedule—although best practices in managing credit risk call for segregating operating loans from equipment loans.

Keeping them bankable

In an increasing number of cases, stronger intervention is called for, in the form of fundamental restructuring of a producer’s outstanding debt. A banker may suggest refinancing operating loans or machinery notes held by the bank or other lenders to extend repayment for as long as 10 or 15 years. Typically, this reprieve requires the producer to pledge additional collateral—usually land—to back up the loan. (However, falling farmland values due to the ag downturn may make it more difficult for cash-strapped producers to draw upon their equity in the future.)

Main Article

Trouble on the farm

District crop and livestock producers are struggling to cope with a sharp drop in commodity pricesRead more

“You’re seeing a lot of restructuring being done now,” Hamilton said. “We restructured quite a few guys at the tail end of 2016, and now going into 2017. Or you restructure them and use FSA [U.S. Farm Service Agency] guarantees in order to shore up the credit and keep these guys bankable.”

The FSA administers farm loan programs that guarantee loans offered by commercial lenders up to 95 percent against loss. Banks can use them to refinance existing bank loans or extend credit to new customers who otherwise wouldn’t qualify. Lending backed by the agency has risen in response to higher demand from lenders; in district states (excluding the Upper Peninsula of Michigan), FSA loans increased 15 percent from 2015 to 2016.

But leveraging FSA guarantees and restructuring loans “only carries you so far,” Hamilton said. Like producers, community banks are hoping for an upturn in commodity prices; an increase in farm revenues would strengthen borrowers’ finances and reduce the risk of loan losses. It’s unclear when that turning point will come; Hamilton has told Independence Bank borrowers not to bank on higher wheat and barley prices this year.

Schneider said American Bank & Trust has “stepped it up another notch” in analyzing farm cash flows and counseling stressed borrowers, but he wondered how long such efforts can stave off painful losses, for both producers and community banks. “For me, the question is, are we getting past the worst of it, or are there another two, three, four years like this in front of the industry? Then it will be harder and harder to stay ahead of the game.”