Authors

Over 20 million Americans, and roughly 800,000 people in district states, have gained health insurance over the past five years. Some of the increase has come from employers offering more jobs with health care coverage in an economy recovering from the Great Recession. But health care experts attribute most of the rise to the Affordable Care Act, also known as Obamacare. The 2010 law enforced minimum standards for insurance policies, provided subsidies through health care exchanges and expanded Medicaid, the government health care program for the poor.

Increased coverage has come primarily through growth in insurance for individuals and increased Medicaid eligibility.

However, the ACA, which Congress has tried to repeal and replace with alternative health insurance legislation, may have had unintended consequences for coverage by small businesses. As health costs and insurance premiums have climbed in recent years, the share of small firms offering insurance to their employees has declined even more so than before passage of the law.

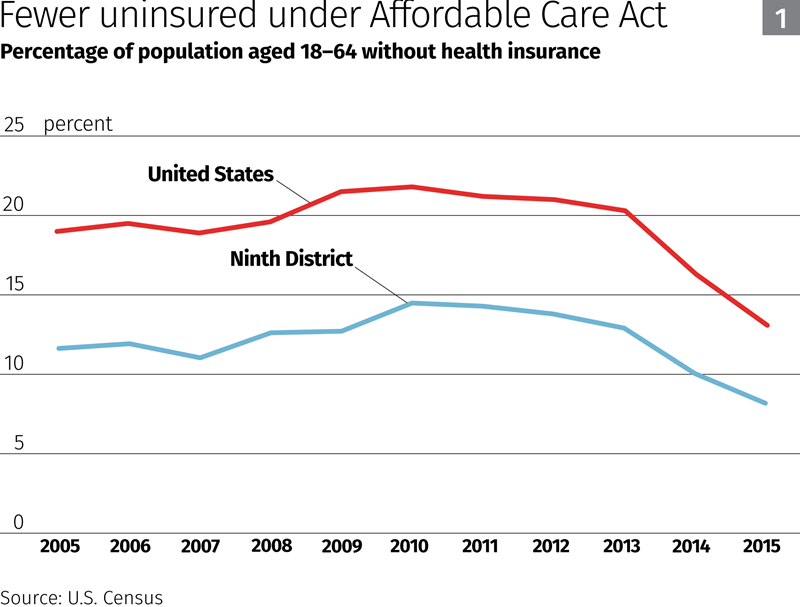

Census data show that before passage of the ACA, the share of people without health insurance was rising, although uninsured rates were lower in district states than in the nation as a whole (Chart 1). The disparity stems largely from higher rates of health care coverage in Minnesota and Wisconsin—home to about 80 percent of the district population—than the national average. Historically, rates of the uninsured have been much higher in less-populated western states in the district, likely because of more stringent rules for Medicaid eligibility and a greater proportion of workers in small businesses.

In Minnesota, low-income adults without children have long received coverage under Medicaid, a program jointly administered by the federal and individual state governments. But childless adults were not covered in Montana, the Dakotas and Wisconsin (which, however, offered more generous coverage for parents than Montana and the Dakotas).

Western states in the district also have a larger share of workers in firms with under 500 employees, which offer health insurance at lower rates than larger firms. In Minnesota and Wisconsin, small- and medium-sized businesses employ about half of all employees, according to the U.S. Small Business Administration. This is in line with the national average. However, in South Dakota smaller businesses account for 60 percent of employment, and in Montana that figure is almost 70 percent.

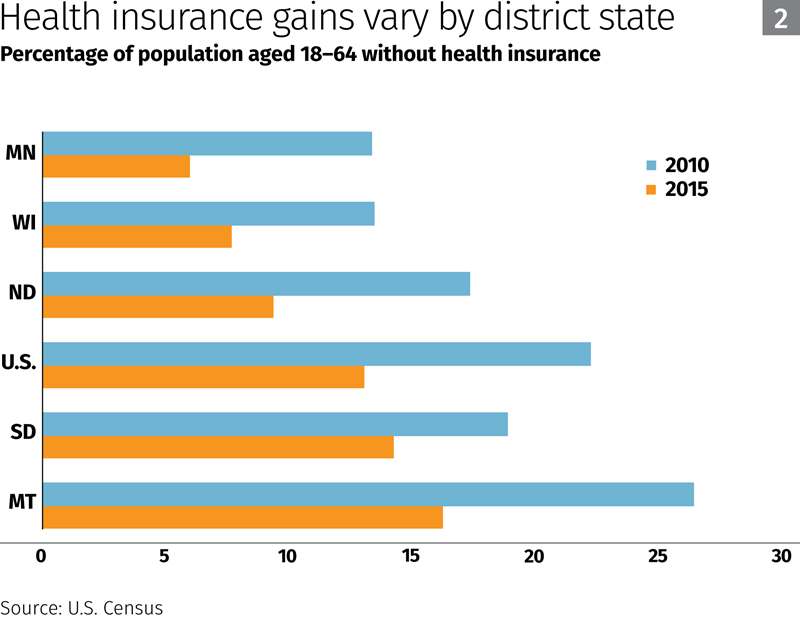

Uninsured rates fell nationwide and in every district state from 2010 to 2015, although some district states have seen greater gains in coverage than others (Chart 2). Uninsured rates dropped more sharply after 2013, when key provisions of the ACA, such as mandatory coverage for individuals and expansion of Medicaid, went into effect.

Subsidies and new Medicaid rules

Under the ACA, people without insurance through their employer can shop for individual policies on health insurance exchanges operated by either states (Minnesota is the only district state that sponsors an exchange) or the federal government. Tax credits to offset premiums are available through the exchanges for individuals with low or moderate incomes.

Before passage of the ACA, the share of the working-age population covered by individual insurance plans in district states was fairly stable, hovering between 9 percent and 10 percent, according to U.S. Census data. From 2011 to 2015, that share rose to 13 percent—an addition of about 380,000 individual policyholders. The bulk of those gains occurred in Minnesota and Wisconsin.

(However, there’s evidence that a sharp increase in individual insurance premiums since 2015 has led to retrenchment in the individual market, at least in some district states; figures released in February by the Minnesota Council of Health Plans indicated that state enrollment in individual plans had shrunk by about 30 percent over the past year.)

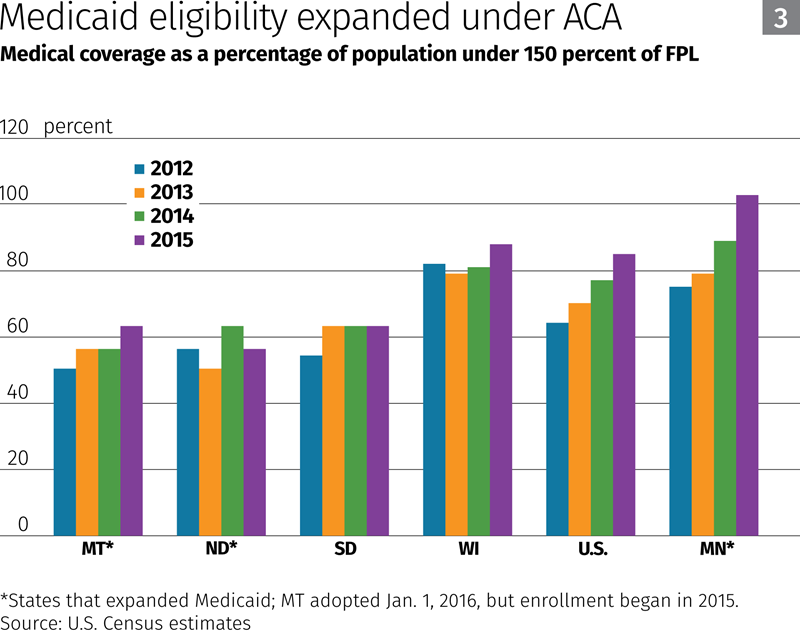

Medicaid enrollment also increased nationwide, and in the district: Medicaid coverage for working-age people in district states increased by about 200,000 people from 2011 to 2015. Minnesota, North Dakota and Montana extended Medicaid eligibility under the ACA to almost everyone with incomes less than 138 percent of the federal poverty level (FPL).

Coverage gains for all lower-income people (Chart 3), based on Census estimates of the number of people with incomes under 150 percent of the FPL, were led by Minnesota and Montana. The share of Medicaid enrollees under that income threshold increased much less in Wisconsin and South Dakota, which didn’t expand Medicaid. (It’s not clear why coverage fell in North Dakota in 2015.)

Hard choices for small firms

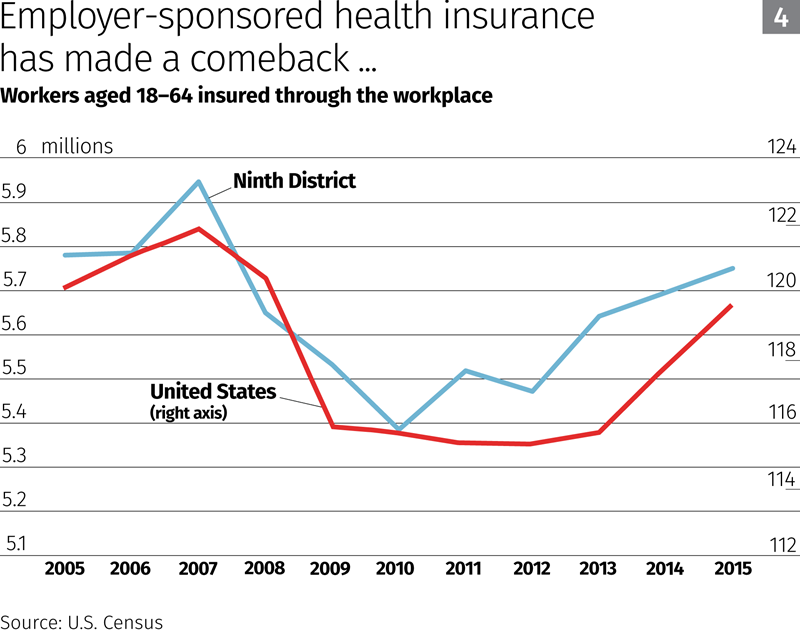

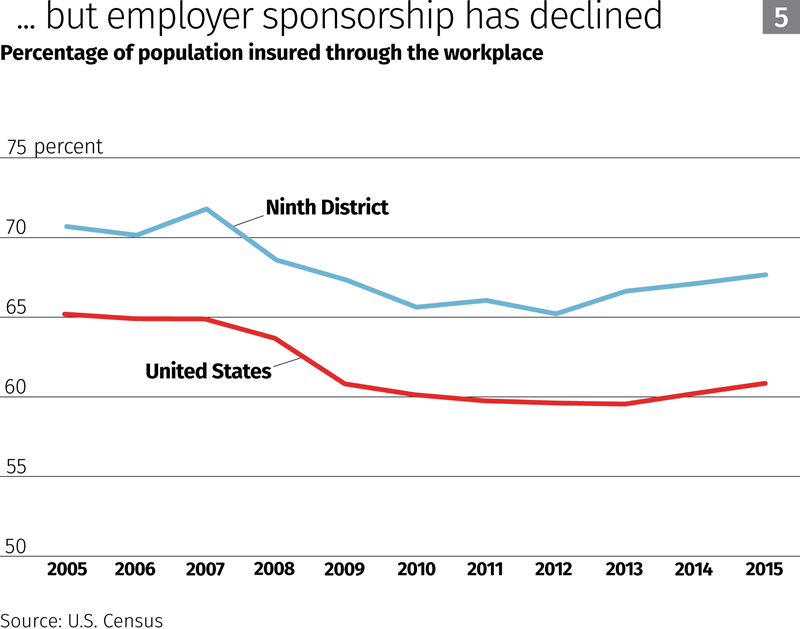

Health insurance coverage through employers fell nationwide and in the district during the Great Recession, but has since rebounded with renewed hiring, although enrollment is still below levels before the downturn (Chart 4). The share of U.S. and district workers in employer-sponsored health plans also dropped during the recession, but as of 2015 remained significantly below prerecession levels (Chart 5).

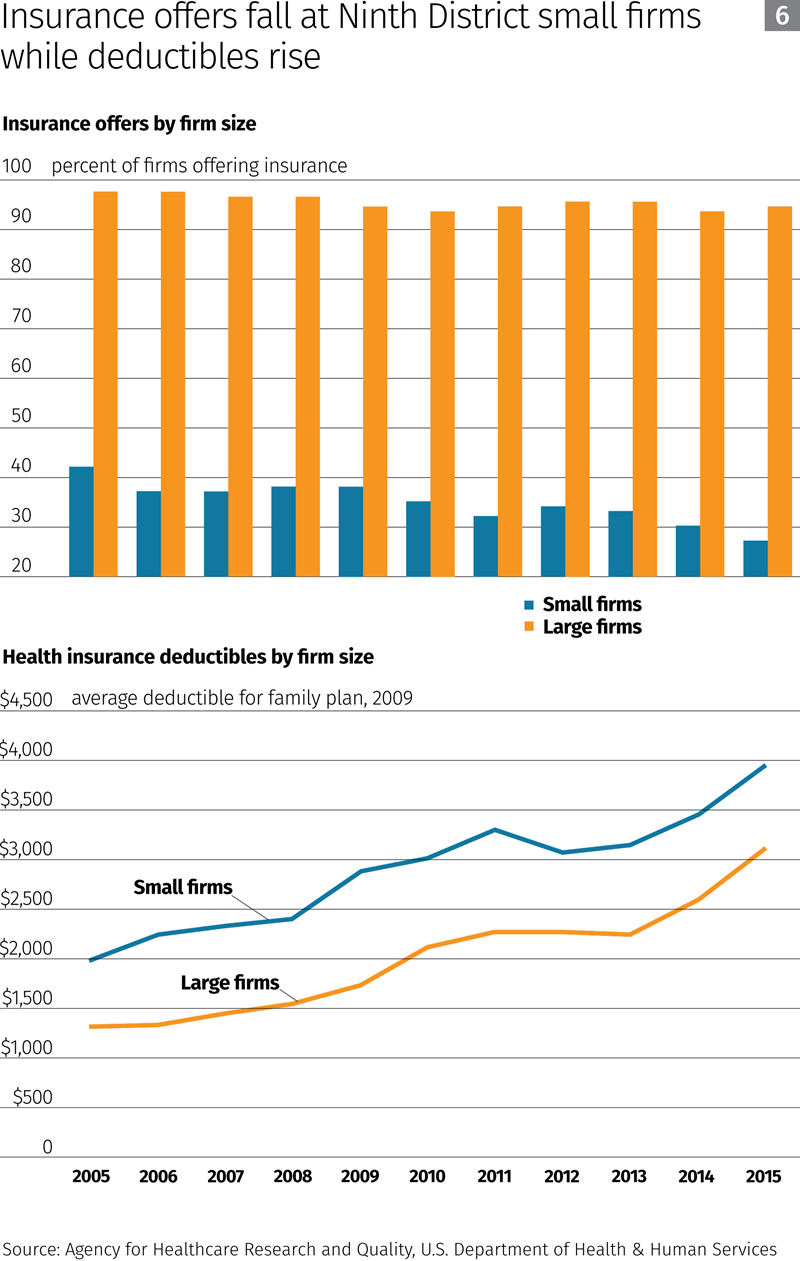

An analysis of employer health insurance offers by firm size suggests that at least some of this falloff in coverage occurred because of a decline in sponsorship by small firms.

The ACA requires employers with over 50 full-time-equivalent workers—which account for about 70 percent of nationwide employment—to provide “affordable” health insurance to their employees. However, most medium- to large-size employers were already doing so before the ACA’s passage, because their size gives them buying power with insurers or allows them to fund their own plans at lower cost than private group insurance.

Little has changed under the ACA for these employers, according to data from the federal Agency for Healthcare Research and Quality. In 2015, the share of medium-to-large firms in the district offering their employees health coverage was only slightly less than it was 10 years before (Chart 6).

In contrast, smaller firms with 50 or fewer workers are not obliged under the ACA to provide health care insurance. The share of small district firms offering their employees health coverage was falling in the United States and in most district states before the ACA, and this dropoff has steepened since the law’s passage.

The decline is likely due to rising health coverage costs that have disproportionately affected small businesses less able than larger firms to negotiate lower insurance rates and self-fund. A 2016 study by the NFIB Research Foundation found that small businesses are struggling to provide health coverage in the face of rising premiums; 52 percent of the 20,000 U.S. small business owners surveyed ranked the cost of health insurance as their most “critical” problem.

To offset escalating premiums, many small firms have sponsored insurance policies with higher deductibles than those provided by large firms. Although deductibles for family plans offered by district employers have increased for both small and large firms, small-firm deductibles have been consistently higher over the past decade.

Rather than offering less-comprehensive coverage, some small businesses may have opted to drop employee insurance coverage altogether. Some analysts have suggested that the ACA has “crowded out” small-business group policies, encouraging small businesses to withhold coverage; firms realized that lower-wage workers eligible for subsidies under the law could obtain cheaper coverage through insurance exchanges for individuals.

Whether increased levels of health care coverage attained since 2010 can be maintained—or raised further—depends to a large degree on the fate of the ACA and the outcome of any future efforts by Congress or district states to rein in rising health care costs and insurance premiums. Key factors that will shape coverage trends include incentives for healthy people to buy insurance, the availability of subsidies for subcribers in the individual market and federal policies on Medicaid eligibility.

The trajectory of health insurance costs in coming years is likely to have a strong bearing on participation by small businesses in insurance markets; lower premiums may slow or arrest the long-term decline in insurance sponsorship by small employers.