Author

This essay is also available on Medium.

Members of the Federal Open Market Committee (FOMC) 1 are trying to understand why inflation and wage growth are low, despite the headline unemployment rate having fallen from a peak of 10 percent during the Great Recession to 4.4 percent today. We would have expected a strong job market to lead to stronger wage growth and then higher inflation as businesses passed their increased costs on to customers. Yet that hasn’t happened. Federal Reserve Chair Janet Yellen offered her thoughts on this topic in a speech last week, and I appreciate her raising this discussion publicly. I draw somewhat different policy conclusions than she did, but I agree that this is an important issue that needs more analysis before we can have confidence in our understanding of why inflation is low.

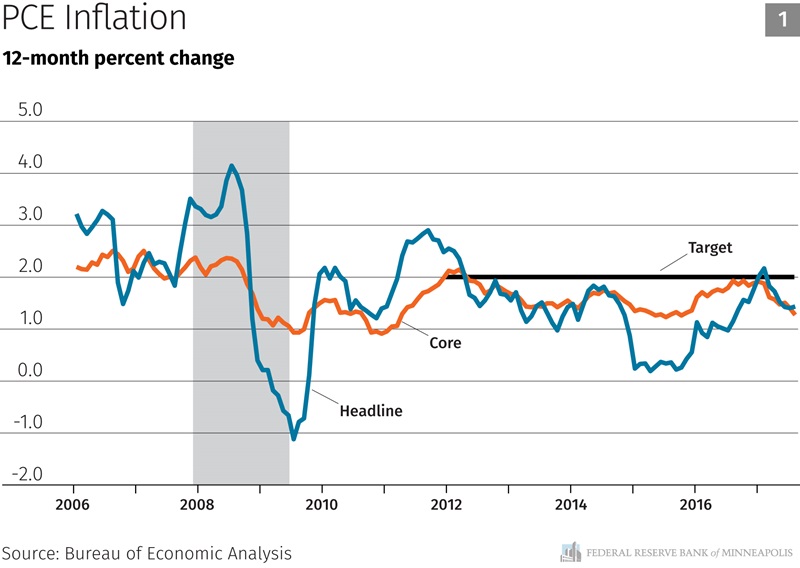

The following chart shows the personal consumption expenditures (PCE) measure of inflation, both headline and core, since 2006. Inflation has been consistently below our 2 percent target over the past five years and, perhaps even more surprisingly, has actually fallen this year.

I believe the most likely causes of persistently low inflation are additional domestic labor market slack and falling inflation expectations. This essay will explore the causes of the latter, falling inflation expectations, and I will argue that the FOMC’s policy to remove monetary accommodation over the past few years is likely an important factor driving inflation expectations lower.

This is not meant to be a criticism of the FOMC’s prior decisions. As I will explain below, we now know that policy was tighter and there was more slack in the labor market than the Committee realized at the time it started removing accommodation. The purpose of this essay is to argue that we should learn the lessons of recent years and proceed with caution before we tighten policy further. If one accepts the conventional view of how monetary policy affects the economy, one must concede that job growth, wage growth and inflation are all somewhat lower than they would have been had the FOMC not removed accommodation over the past three years. In addition, allowing inflation expectations to slip will give us less room to reduce interest rates in response to a future economic downturn because we will hit the effective lower bound more often than if we had preserved expectations at our 2 percent target.

Monetary policy primarily works through expectations

When people borrow money to buy a house, or businesses take out a loan to build a new factory, they don’t really care about overnight interest rates. They care about what interest rates will be for the term of their loan: 5, 10 or even 30 years. Similarly, when banks make loans to households and businesses, they also try to assess where interest rates will be over the length of the loan when they set the terms. Hence, expectations about future interest rates are enormously important to the economy. When the Fed wants to stimulate more economic activity, we do that by trying to lower the expected future path of interest rates. When we want to tap the brakes, we try to raise the expected future path of interest rates.

Three monetary policy tools

The primary tool the FOMC uses to set monetary policy is the federal funds rate (FFR), which is an overnight rate. I said earlier that borrowers and bankers don’t care too much about overnight rates, so why would adjustments of the FFR affect the economy? The answer is primarily through expectations about future interest rates. If the FOMC raises the FFR, it is a signal that rates will likely be higher in the future. If the FOMC lowers the FFR, it sends a message that rates will likely be lower.

The second tool the FOMC uses to set monetary policy is forward guidance. Through our policy statement that we release after every FOMC meeting and through our quarterly Summary of Economic Projections (SEP), we give indications to the public about how we think the economy is likely to perform in the future and the likely path for interest rates. During the Great Recession, once overnight interest rates were effectively lowered to zero, the FOMC provided forward guidance that rates would likely stay low for a long period of time. That forward guidance gave households, businesses and bankers confidence that interest rates would be low for longer and thus, we believe, stimulated more economic activity than had the Committee not provided that guidance.

The third tool the FOMC used in the aftermath of the Great Recession to affect monetary policy was quantitative easing (QE), or using the Fed’s balance sheet. Once the FFR was effectively at zero, the Fed embarked on its QE programs to directly drive longer-term interest rates down by buying longer-term bonds. One of the channels through which QE affects the economy is also expectations—by further signaling the FOMC’s commitment to stimulating the economy through accommodative monetary policy.

Inflation expectations started falling in 2014

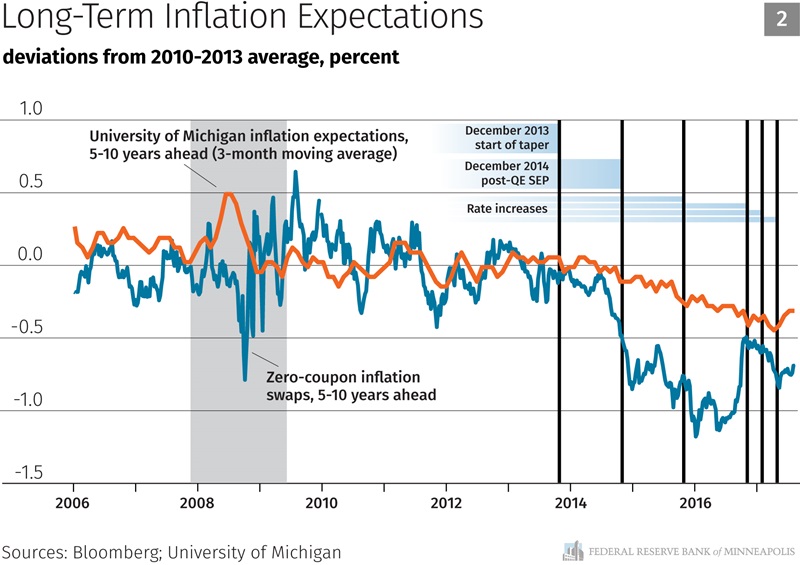

Inflation expectations held up remarkably well during the Great Recession—despite 10 percent unemployment and a terrible financial crisis. I credit the Federal Reserve’s policy responses with keeping inflation expectations anchored and preventing the U.S. economy from falling into a terrible deflationary spiral. But as you can see in the following chart, inflation expectations—as indicated by both market-based measures and the Michigan survey of consumers—did begin to fall in early 2014 soon after the FOMC began to remove monetary accommodation. The actual policy change of tapering QE began in December 2013, while then Fed Chairman Ben Bernanke began discussing the taper in May 2013.

Removing accommodation is a form of tightening

People have asked me: How can you argue that the Fed is slowing down the economy with interest rates still low relative to historical norms? My answer is that the economy would likely have performed better had the Fed not removed accommodation. In my view, the FOMC has taken three types of actions to tighten monetary policy in the following chronological order:

-

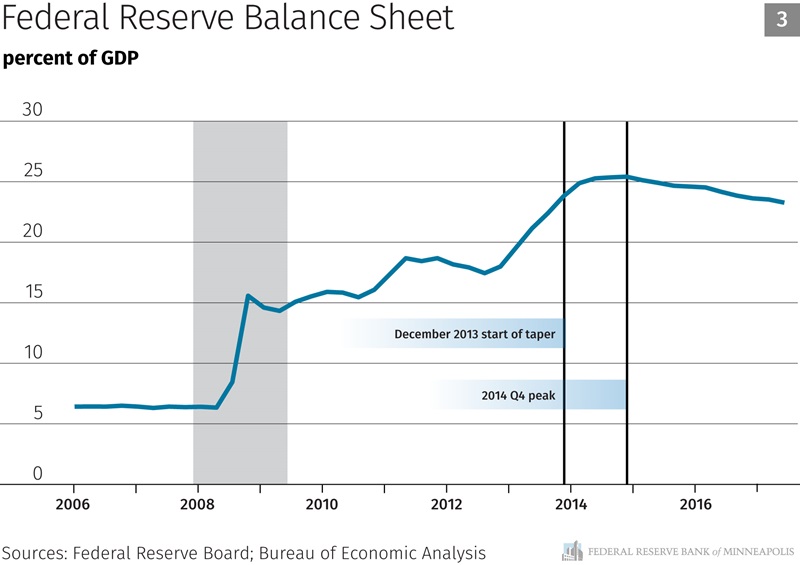

Ending QE. I described earlier how QE affects the economy by driving down longer-term interest rates and through signaling a commitment to maintaining accommodative monetary policy in the future. When the Fed began discussing tapering QE in mid-2013, it effectively began the process of removing accommodation by significantly changing expectations of further QE. And once the taper was complete and the Fed’s balance sheet was fixed at $4.5 trillion, its stimulative effects began to shrink, albeit slowly, relative to the growing U.S. economy. In addition, the end of QE also signaled an end of the commitment of the FOMC to use extraordinary measures to support economic activity at that time. That also would likely have a contractionary effect on the economy through expectations of tighter monetary policy.

-

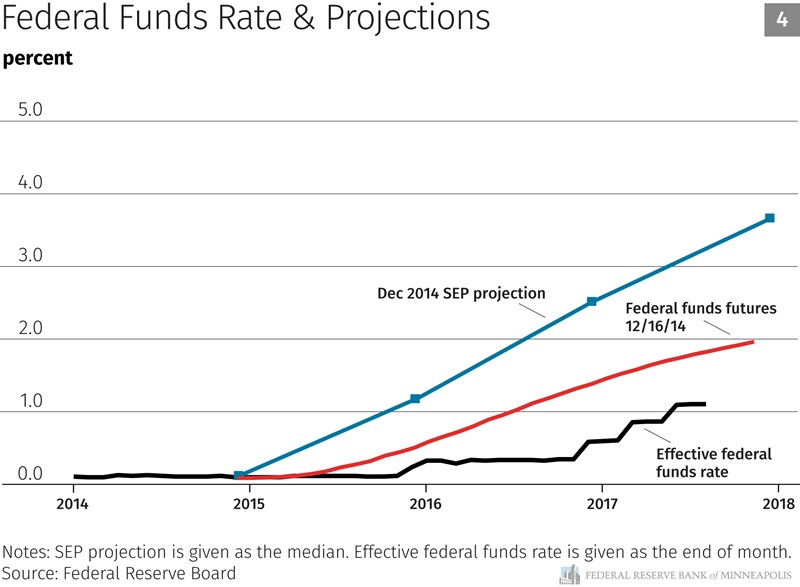

Hawkish forward guidance. For several years, the FOMC, through its SEP, put forward rate paths that were very aggressive compared with what the economy ended up needing (and even higher than what markets had been expecting at the time). For example, in December 2014, the SEP set the expectation that by December 2016, the FFR would be at 2.50 percent, when, in fact, the FFR ended up at only around 0.6 percent. With the benefit of hindsight, this guidance ended up being far too hawkish and likely had a somewhat contractionary effect on economic activity by signaling significantly higher interest rates in the future.

-

Four rate hikes. The FOMC began actually raising the FFR in December 2015 and followed up with three more hikes through June 2017, despite muted wage and inflationary pressures. The signal from this activity suggests a strong desire to raise rates, even with an absence of inflationary pressures.

We know that monetary policy operates with a lag. I believe these actions to remove various forms of accommodation are now having an effect on the economy by lowering inflation expectations. In my view, inflation expectations declined because actual inflation was below target for a long time, and the Fed’s actions to reduce accommodation led to a weakening of confidence that it was serious about bringing inflation back to target in a reasonable time frame.

Reassessing neutral

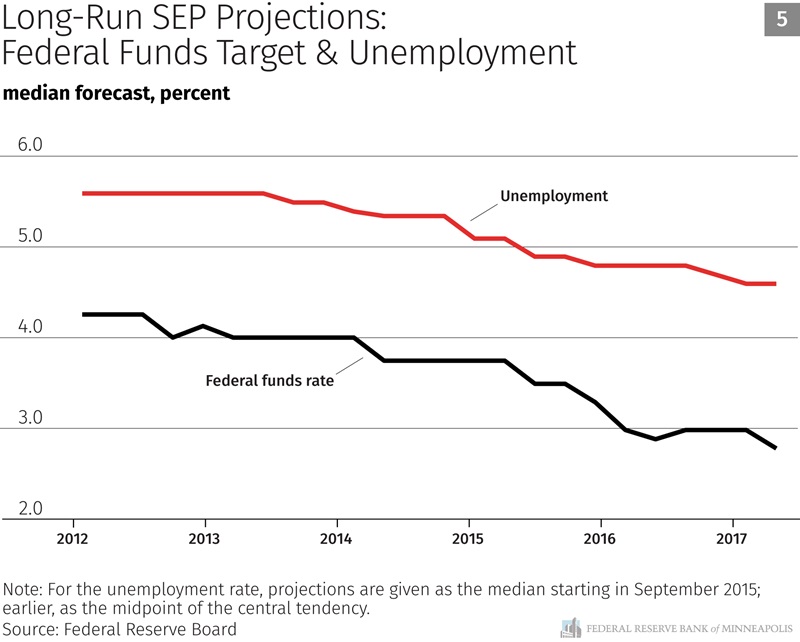

I just argued that FOMC policy over the past few years has likely led to falling inflation expectations and somewhat slower job growth, wage growth and inflation. Why did the FOMC remove accommodation during this time? I believe it is because the Committee thought it was providing more stimulus than it actually was. Members of the FOMC (including me) now believe that both the neutral real interest rate (the interest rate that neither stimulates nor contracts the economy) and the natural rate of unemployment (the rate that represents maximum employment) are lower than we had realized in prior years. The Committee has been gradually lowering its estimates for both over time. Here is a chart showing how the median FOMC participants’ estimates of the long-run FFR and maximum employment have changed. The implication of these revisions, admittedly with the benefit of hindsight, is that monetary policy was less accommodative than we previously thought. And over the past five years, we have overestimated inflation and underestimated how long it would take to return to our 2 percent target.

I believe it is also important to note that even if the short-term policy rate is set at a lower level than the neutral short-term interest rate, overall monetary policy might not be accommodative if the Federal Reserve is simultaneously setting expectations for higher rates in the future.

What might be wrong with my analysis?

A number of explanations for low inflation have been offered by economists and policymakers, including: (1) transitory factors (which essentially mean one-offs that don’t signal an underlying trend), (2) technology development that is driving production costs lower, (3) a global supply of labor that is keeping U.S. wages down, (4) additional domestic labor supply that is not captured by the headline unemployment rate and (5) falling inflation expectations.

It is important to note that many advanced economies have been experiencing low inflation in recent years. It is not simply a U.S. experience. This is important because any explanation for low inflation ought to be able to explain what is happening around the world. This suggests that the transitory factors explanation, such as falling cell phone service pricing in the United States, is not likely a good explanation for consistently low inflation in Europe.

Ongoing technology development is not a new phenomenon, nor is a large group of workers, from China for example, entering the global labor market. So I struggle to see how those factors can explain the recent low inflation. In addition, productivity in advanced economies has been low for some time. It is hard to reconcile low productivity growth with a burst of new technology that is keeping prices low.

So how does my story of FOMC tightening explain low advanced-economy inflation? While advanced-economy central banks are not formally coordinating policy, they do tend to move in the same direction. The Fed, European Central Bank and Bank of England all pursued very low interest rates, hitting their own effective lower bounds at roughly the same time. They have also been signaling a desire to remove accommodation and return to more normal policy.

Another important issue some people point to is that financial conditions as measured by various indexes have strengthened as the FOMC has removed accommodation. Some suggest this indicates that the FOMC has not in fact removed accommodation during this time. I don’t find this argument compelling. I believe that the apparent easier financial conditions are likely a reflection of the market’s own recognition that equilibrium long-term real rates have fallen. A lower future interest rate environment could justify higher asset prices and seemingly easier financial conditions today by virtue of markets’ discounting cash flows with a lower interest rate.

Finally, some argue that inflation expectations haven’t fallen, pointing to the Survey of Professional Forecasters, where inflation expectations have been solidly anchored at the Fed’s 2 percent target for years. I don’t find this survey as compelling as the data I referenced above because it is limited to a very small set of forecasters. We need to understand the expectations underlying millions of individual wage negotiations between employees and employers, which I believe are better captured by broader measures.

Implications for future monetary policy

If I am correct that the Fed’s own actions are an important factor driving surprisingly low inflation and falling inflation expectations, the implication is that our policy should focus on supporting inflation to ensure that we are on track to return to our 2 percent target. My preference would be not to raise rates again until we actually hit 2 percent core PCE inflation on a 12-month basis, unless we have seen a large drop in the headline unemployment rate signaling that we have used up remaining labor market slack, or a surprise increase in inflation expectations.

Of the five possible explanations I mentioned for low inflation, four of them (global labor supply, technology development, more domestic labor slack and falling inflation expectations) all suggest there is no reason to raise rates until we start to see wages and inflation climb back to target. The only explanation that would potentially call for further policy tightening is the transitory factor explanation. But the longer low inflation persists (here and around the world), the more tenuous that story becomes.

Job growth, wage growth, inflation and inflation expectations are all likely somewhat lower than they would have been had the FOMC not removed accommodation over the past three years. Allowing inflation expectations to slip further will mean that we will have less powerful tools to respond to a future economic downturn. I believe these are significant costs that we must consider as we contemplate the future path of policy.

Endnote

1 These comments are my own and do not necessarily reflect the views of other members of the Federal Open Market Committee or the Federal Reserve System.