Author

In the ten years following the global financial crisis, the US labour market has largely recovered, with the unemployment rate falling from a peak of 10 per cent in 2009 to 3.9 per cent today, an 18-year low. US firms widely report difficulty finding qualified workers to fill job openings.

As in other advanced economies, the US recovery took place after the Federal Reserve undertook extraordinary monetary policies, including keeping interest rates unusually low and quantitative easing bond-buying programmes.

While some economists predicted these policies would lead to runaway inflation, the opposite has happened: inflation and wage growth have been surprisingly low. Despite the tight US job market, total pay is only growing at 2.7 per cent annually, compared to 3.5 per cent before the crisis. Similarly, inflation has now finally reached the Federal Open Market Committee’s target of 2 per cent, after consistently undershooting it for the past six years. We on the FOMC estimate that the economy is running at full potential when the unemployment rate is around 4.5 per cent. With unemployment even lower now, why is wage growth so low?

Labour markets in other advanced economies shed some light on what is happening in America. The headline US unemployment rate captures only those who are actively looking for work. For example, it ignores people who are out of the labour force because they have given up looking for a job. Apparently, the Great Recession was so traumatic that it pushed many Americans out of the labour force altogether.

However, as the economy has slowly recovered, we have seen people return to work years after losing their jobs. It could be that the 3.9 per cent measure doesn’t capture the true slack in the labour market and that additional, hidden slack explains today’s modest wage growth.

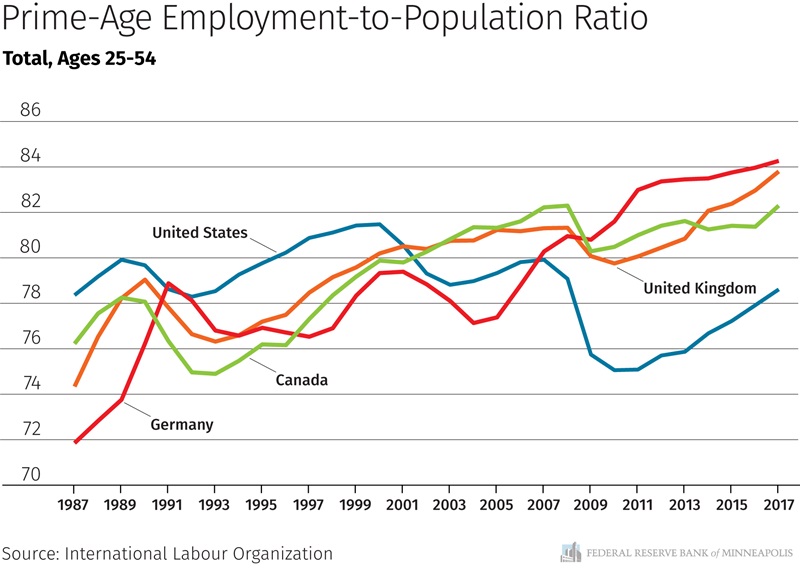

A better measure of labour market tightness appears to be the employment-to-population ratio of prime-age workers, those age 25 to 54 years old. By focusing on prime-age adults, this measure of how many people are actually working helps adjust for demographic trends such as ageing. Today the US prime-age employment-to-population ratio is 79.2 per cent, down from 80.0 per cent in early 2007. That drop suggests that approximately 1m additional prime-age Americans would be available to work if the US labour market recovered to its pre-recession strength.

But if you look at international comparisons, there is an astonishing contrast between the US and other developed economies. The percentage of prime-age Americans who are working has been trending down over the past few decades, while the same ratio has climbed to new highs in the UK, Canada and Germany. Each of these countries is experiencing falling fertility rates and an ageing population just like the US. Why is American employment falling while it is climbing elsewhere?

Economists offer various theories to explain this. Some are specific to the US: many Americans are addicted to drugs; too many have criminal records; workers don’t have the skills needed for the available jobs. Alternative explanations, such as the rise of Chinese manufacturing and of automation, should affect other advanced economies as much as they do the US, and those hypotheses would suggest that employers lack demand for workers, rather than that people are unwilling to work.

As the American job market has tightened, many companies are taking extra steps to attract workers, such as providing training, or eliminating drug and criminal background checks for certain positions. The truth is, we don’t know how much slack still remains in the US labour market. But international labour markets offer a hopeful sign that many more Americans might choose to work if wages picked up.

People are already responding to a strong job market in positive ways. The number of working-age Americans who reported not being able to work because of a disability increased steadily for 20 years until 2014, when, remarkably, the numbers began rapidly falling. People who were once thought lost from the job market returned to work. A continuation of these trends would be positive for both workers and the US economy as a whole, and it would mean that a rapid rise in inflation is further away than we might believe.

This analysis has important implications for monetary policy. It suggests that as we return interest rates to normal levels, we should shift only to a neutral policy stance, and not move too quickly, until we see more evidence that wages are climbing and that we really are at maximum employment.

See Neel Kashkari's Op-Ed in the Financial Times.