Author

Though harvests in some areas were stalled by heavy late-season rains, crop production this year was strong, hitting records in some Ninth District states. But low crop prices and trade woes dealt a financial blow to farmers from July through September 2018, according to the Federal Reserve Bank of Minneapolis’ third-quarter (October) agricultural credit conditions survey.

Land values were stable on average across district states, and interest rates on loans rose modestly from the previous quarter. The outlook for the fourth quarter is similar, with lenders in the district generally expecting farm incomes to decrease further.

Farm income, household spending and capital investment

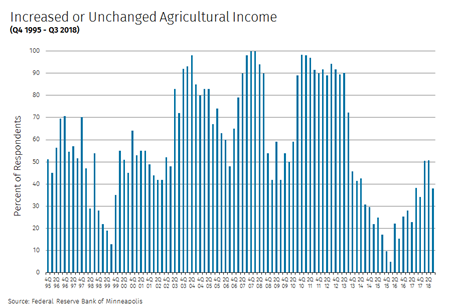

"Price is still a challenge, but yields will make up some of the difference," a South Dakota banker commented, characterizing the general mood of survey respondents. A majority of district lenders surveyed (62 percent) reported that farm incomes decreased in the third quarter of 2018 from a year earlier, while most of the remainder reported that incomes were unchanged (see chart). Household spending was down on balance as well, with 34 percent of lenders reporting that it fell, while only 4 percent said it increased.

Farms also spent less on buildings and equipment-60 percent of lenders reported decreased capital spending, and 3 percent said it increased.

Unlike much of the Ninth District, where growing conditions were generally good, parts of Minnesota suffered from heavy rains and flooding this year. Perhaps as a consequence, the state had the highest portion of any in the district of lenders reporting decreased farm incomes-at an impressive 91 percent-with none reporting increased income.

In Montana, by contrast, two-thirds of respondents said incomes were unchanged from a year earlier, with the balance split equally between those reporting increases and those reporting decreases.

Loan repayments and renewals

Reflecting tighter budgets for farm households, the rate of repayment on agricultural loans fell on average, while renewals increased slightly. Compared with a year earlier, loan repayment rates decreased for 37 percent of respondents, while 63 percent reported that rates were unchanged. One-third of lenders stated that the number of renewals or extensions increased, while most of the remainder said renewal activity was unchanged. Fewer than 2 percent reported decreased renewals.

Demand for loans, required collateral, and interest rates

Falling incomes also drove increases in demand for loans by farm households in the third quarter. While slightly more than half of respondents indicated that loan demand was unchanged from a year ago, 41 percent noted increased loan demand. Collateral requirements have increased, according to 21 percent of lenders surveyed, with the balance reporting no change. Fixed and variable interest rates for operating, machinery, and real estate loans all increased modestly from the previous quarter.

Cash rents and land values

Following a pattern from the most recent quarterly surveys, the third-quarter results generally pointed to a moderate increase in farmland values, in a reversal of the previous trend of steady, but moderately declining, land prices after a long period of soaring growth. The average value for nonirrigated cropland in the district actually increased by slightly less than 1 percent from a year earlier, according to survey respondents. Irrigated land values increased slightly less, while ranch- and pastureland increased a little less than 3 percent on average.

In contrast, the district average cash rent for nonirrigated land dropped 1.5 percent, reflecting continued low crop prices. Rents for irrigated land decreased about 1 percent, while ranchland rents increased 2 percent.

However, land values varied across the region. Prices fell slightly in South Dakota and Minnesota compared with a year earlier, while Wisconsin land prices rose 3 percent and North Dakota prices climbed nearly 8 percent. Cash rents declined more consistently across the region, falling the most in Minnesota at 2.5 percent, but they increased a little more than 1 percent in Wisconsin.

Outlook

“Trade war needs to be resolved to provide stability for customers,” predicted one Minnesota banker, echoing numerous comments about the consequences of tariffs.

The outlook for the fourth quarter of 2018 was downbeat. Across the district, 61 percent of lenders expected farm income to decrease, while only 4 percent expected increases. The forecast for capital spending was similar, with 63 percent of respondents expecting decreases, but only 35 percent expecting farm household spending to fall.

Almost half of respondents projected loan demand to increase in the final three months of 2018, while a similar portion expected loan repayment rates to decline, and 44 percent forecast increased renewals and extensions. Nearly a quarter of respondents thought that the amount of required collateral on loans would increase.

State Fact Sheet Q3 2018

Percent of respondents who reported decreased levels for the past three months compared with the same period last year:

|

MN |

MT |

ND |

SD |

WI |

Ninth District |

|

| Rate of loan repayments |

29

|

-

|

35 | 52 | 50 | 37 |

| Net farm income |

81

|

17 | 47 | 67 | 67 | 62 |

| Farm household spending |

55

|

17 | 24 | 29 | 33 | 34 |

| Farm capital spending |

81

|

17 | 35 | 70 | 67 | 60 |

| Loan demand |

10

|

- | - | - | 17 | 4 |

Percent of respondents who reported increased levels for the past three months compared with the same period last year:

|

MN |

MT |

ND |

SD |

WI |

Ninth District |

|

| Loan renewals or extensions |

33

|

- | 47 | 29 | 50 | 34 |

| Referrals to other lenders |

16

|

17 | - | 5 | 17 | 9 |

| Amount of collateral required |

20

|

-

|

24 | 29 | 17 | 21 |

| Loan demand |

43

|

17

|

47

|

43

|

33 | 41 |

State Fact Sheet Outlook Q3 2018

Percent of respondents who expect decreased levels for the next three months:

|

MN |

MT |

ND |

SD |

WI |

Ninth District |

|

| Rate of loan repayments |

58

|

-

|

50

|

58

|

25

|

49

|

| Net farm income |

80

|

17

|

53

|

65

|

50

|

61

|

| Farm household spending |

55

|

17

|

18

|

29

|

50

|

35

|

| Farm capital spending |

81

|

17

|

47

|

70

|

50

|

63

|

| Loan demand |

5

|

20

|

0

|

-

|

-

|

3

|

Percent of respondents who expect increased levels for the next three months:

|

MN |

MT |

ND |

SD |

WI |

Ninth District |

|

| Loan renewals or extensions |

58

|

-

|

50

|

37

|

50

|

44

|

| Referrals to other lenders |

22

|

20

|

8

|

16

|

-

|

16

|

| Amount of collateral required |

17

|

-

|

19

|

39

|

25

|

23

|

| Loan demand |

53

|

20

|

44

|

53

|

50

|

48

|

Note: The Upper Peninsula of Michigan is not part of the survey.

Appendix:

Joe Mahon is a Minneapolis Fed regional outreach director. Joe’s primary responsibilities involve tracking several sectors of the Ninth District economy, including agriculture, manufacturing, energy, and mining.

{kind=link}