Author

“Few decisions shape an individuals’ life more,” declare Princeton University economists Adrien Bilal and Esteban Rossi-Hansberg.

That fateful choice? Where to live.

Whether you stay in your hometown, move to a less-expensive city, or aspire to something better has enormous consequences, both short- and long-term. Location “determines job opportunities, social interactions, schooling and entertainment options.”

And, ultimately, the location decision transforms the course of one’s life—income, health, longevity, and family well-being, including future generations. “Prospects for a kid growing up in Palo Alto are staggeringly different than those for someone growing up in central Detroit, even if they come from similar backgrounds,” write Bilal and Rossi-Hansberg in “Location as an Asset,” a working paper released by the Minneapolis Fed’s Opportunity & Inclusive Growth Institute.

Move to opportunity?

The obvious question is, Why do so many people live in towns with bad housing, poor schools, and meager employment prospects rather than move to locations with better conditions that would likely improve their lives? Customary explanations—high moving expenses and exorbitant living costs—aren’t plausible, contend Bilal and Rossi-Hansberg, who argue that data on actual moving costs don’t bear this out, and affordable options are available even in expensive locales if one is willing to live in a small apartment or endure a long commute.

Instead, they suggest, think of location choice as an investment decision. A person without savings who loses his or her job can survive the shock by moving to a less-desirable city, “borrowing” from that location to pay current living expenses. In contrast, someone benefiting from a positive shock—an inheritance, say—might “invest” in a good location and enjoy sustained payoff from its better housing, schools, and employment.

Either decision involves an “intertemporal transfer of consumption”—choosing whether to consume now or save for rainy day. And the fact that anyone, rich or poor, can make that transfer—by moving—is what makes location a special asset.

Is the theory tenable? Yes. The economists’ mathematical model generates theoretical results consistent with the hypothesis, and it tests well against French data. They find that individuals who move from poor locations to good ones receive higher wages immediately and then continued increases, just as financial assets pay off steadily. The model and data also show that individuals who experience negative shocks tend to move to poorer locations, particularly if they’re financially constrained—no savings or loans. In essence, they’re “borrowing” from their future prospects by moving to a less-desired location where food and shelter are cheaper.

There are clear implications, say Bilal and Rossi-Hansberg; one of the strongest is that development strategies to improve locations—so-called place-based policies—could harm the well-being of those who need to borrow by moving to inferior locations to cope with negative shocks.

Location assets—theory and fact

To arrive at these conclusions, Bilal and Rossi-Hansberg create a “simple” model that incorporates individuals with different skill levels, incomes, and savings, and a continuum of locations classified by the skills of those who live in them combined with returns from those locations. They distinguish between those constrained by lack of savings or borrowing ability and those who are unconstrained.

The model’s key mechanism is that individuals make location choices after positive or negative shocks based in part on whether they are financially constrained. If financially constrained, they can still “borrow” by moving where costs are lower. If unconstrained, they’ll be less likely to move. Regardless of constraint, lucky people receiving a positive shock can “invest” in a city with high-paying jobs. They’ll experience an immediate wage bump and ongoing returns from a location with brighter financial promise.

The economists then apply the theory to French data—workers between 1994 and 2007 from over 35,000 municipalities. They determine which locations are more or less financially attractive by calculating the average income in each. And because the database doesn’t include assets or savings, they assign individuals an asset rank according to relative wage percentile at their location and confirm results with a measure that infers savings relative to income.

Two tests

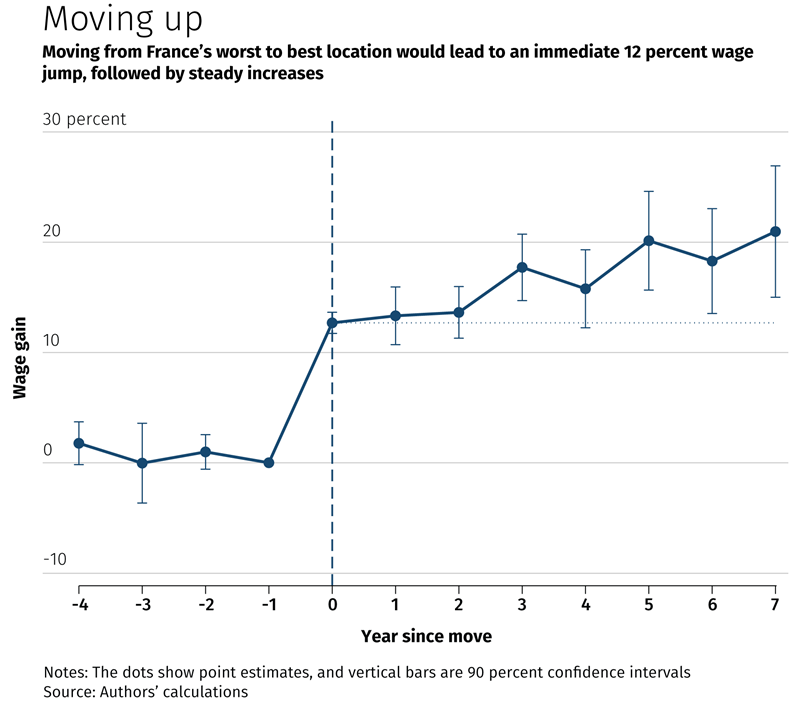

The economists first investigate what happens to wages of French workers who moved to better locations. They find that the average worker moving to the best municipality from the worst enjoyed an immediate 12 percent wage boost. More important for the “location as an asset” hypothesis, the move continued to pay off. “The return to migration almost doubles after 7 years,” they write. “Wages are then 21% higher.” (See figure.) It’s a crucial finding: “We conclude that location in fact has a payment structure that resembles an intertemporal asset.”

The stronger test of theory is whether location decisions differ between people who are and aren’t financially constrained. “The main implication of our model is that individuals with a low income rank in their original location (and therefore presumably financially constrained) should downgrade their location relative to [less-constrained] individuals in the same location.”

Their regression equation evaluates which factors best explain location decisions of workers who move after losing their jobs and finds that inability to self-finance or borrow is a very powerful explanatory variable. Workers in the bottom income rank—the most constrained—choose locations that rank almost 15 percent lower than the highest-income ranked workers in their home location, “a large effect that indicates very different mobility patterns across individuals.”

Recognizing that a number of other explanatory factors, such as commuting costs or local amenities, could “threaten” their interpretation, the economists control for several such factors. Their results stand: Faced with a negative economic shock, financially constrained workers are more likely than unconstrained workers to move to poorer locations.

Location is an asset.