Author

This essay is also available on Medium.

In the Federal Open Market Committee meeting that concluded on Wednesday of this week, I advocated for a 50-basis-point rate cut to 1.75 percent to 2.00 percent and a commitment not to raise rates again until core inflation reaches our 2 percent target on a sustained basis. I believe an aggressive policy action such as this is required to re-anchor inflation expectations at our target.

Since I became president of the Federal Reserve Bank of Minneapolis in January 2016, I have advocated against interest rate increases because I did not see sufficient evidence that inflationary pressures were building, and I believed there was still slack in the labor market. These views led me to formally dissent against rate increases in March, June, and December 2017. More recently, I supported the Committee’s decision in January 2019 to pause further rate increases.

In the past few months, the job market has slowed, wage growth has flattened, inflation has continued to come in below our 2 percent target, inflation expectations have fallen, and the yield curve has inverted.

Minneapolis Fed economists estimate that long-run inflation expectations are currently around 1.7 percent. While that may seem like a small miss from our 2 percent target, it means we will have less ammunition to respond to a future downturn because real interest rates, net of inflation, drive economic activity.

Long-run inflation expectations are a reflection of the reaction function the FOMC has taught the markets over a number years. I have argued that since formally adopting its 2 percent target in 2012, the Committee has treated it like a ceiling rather than a symmetric target. Such treatment is consistent with long-run inflation expectations of 1.7 percent rather than 2 percent.

With inflation expectations falling further in recent months, I believe the Committee should now take action to re-anchor expectations at 2 percent. To do so, we will need to teach the markets a new reaction function that credibly treats 2 percent as a symmetric target. Given that it has taken years for the markets to learn our current reaction function, I don’t believe a rate cut or two in isolation will do much to boost inflation expectations. That is why I argued we should also commit to not raising rates from the new lower level until we see core inflation sustainably reach our target.

The Committee has consistently been too optimistic in forecasting inflation returning to 2 percent. Core inflation is the best predictor we have of future headline inflation. My proposed strategy keeps rates on hold for as long as necessary until we actually hit our target. I believe such a strong, credible commitment will boost inflation expectations, while not allowing them to drift too high. If economic conditions weaken or if inflation fails to return to target, this strategy does not preclude further rate reductions. This strategy will also support further job growth, stronger wage growth, and continued economic expansion.

In February 2017, I first published the data and analyses I focus on in reaching my monetary policy recommendations. For those interested in a deeper look at my rationale for advocating for a rate cut at this week’s meeting, I have updated the same framework to show how the data have changed in the past two-and-a-half years and how my interpretation of those data has led me to make this policy recommendation.

My Analysis (An Update to the Framework First Published in February 2017)

Let me acknowledge up front that the analysis that follows is somewhat detailed and complex; yet it is still not comprehensive. FOMC participants look at a wider range of data than I detail here. I am focusing only on the data that I find most important to determining the appropriate stance of monetary policy.

As I have done previously, let me begin my analysis by assessing our progress in meeting the dual mandate Congress has given us: price stability and maximum employment.

Price Stability

The FOMC has defined its price stability mandate as inflation of 2 percent, using the personal consumption expenditures (PCE) measurement. Importantly, we have said that 2 percent is a target, not a ceiling, so if we are under or over 2 percent, it should be of equal concern. We look at where inflation is heading, not just where it has been. Core inflation, which excludes volatile food and energy prices, is one of the best predictors we have of future headline inflation, our ultimate goal. For that reason, I pay attention to the current readings of core inflation.

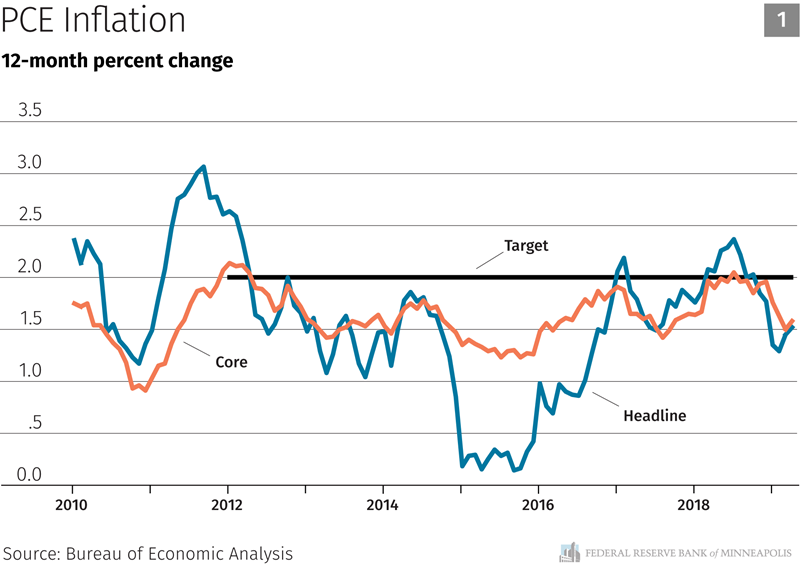

Chart 1 shows both headline and core inflation since 2010. One clearly sees that core inflation has repeatedly approached our 2 percent target only to fall back down. Currently, core inflation is at 1.6 percent year over year and headline is at 1.5 percent, having fallen over the past six months. It is certainly possible that temporary factors are holding inflation down. But we’ve been saying that for years. Looking at this chart, it is not surprising that long-run inflation expectations are below 2 percent, since we appear to never allow core inflation to climb above 2 percent, a point I expand on below.

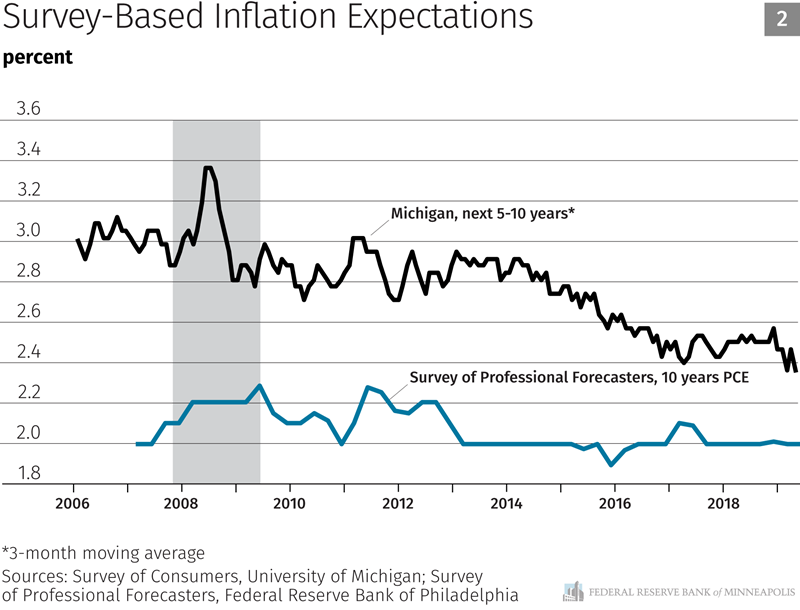

Next let’s formally look at inflation expectations—or where consumers and investors think inflation is likely headed (Chart 2). Inflation expectations are important drivers of future inflation, so it is critical that they remain anchored at our 2 percent target. Survey measures of long-term inflation expectations are flat or trending downward. (Note that the Michigan survey, the black line, is consistently elevated relative to our 2 percent target. What is important is the trend, rather than the absolute level.) The Michigan survey has found inflation expectations trending downward over the past few years, and they recently hit their lowest-ever reading. In contrast, professional forecasters seem to remain confident that inflation will average 2 percent.

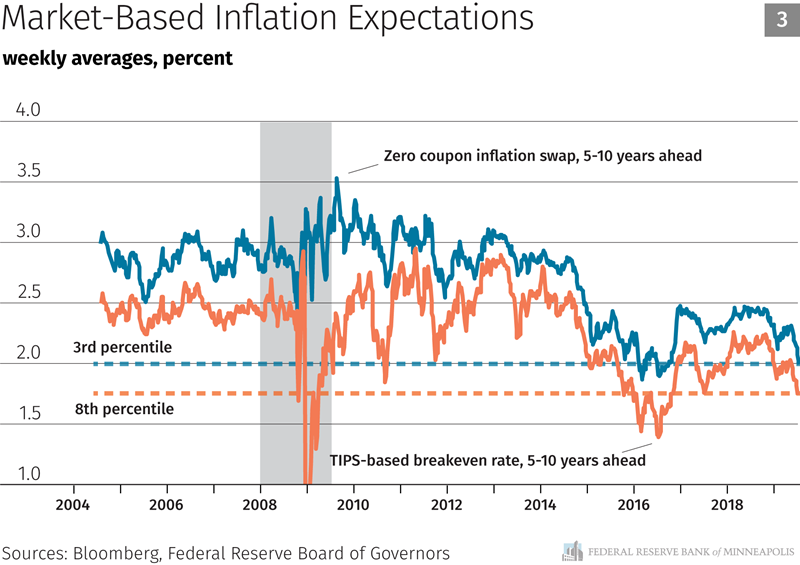

Market-based measures of long-term inflation expectations jumped a bit immediately after the 2016 presidential election. Since then, the markets’ inflation forecasts have moved up and then turned around and have now moved back down. As Chart 3 indicates, market-based expectations remain at the low end of their historical range and have fallen notably in recent months.

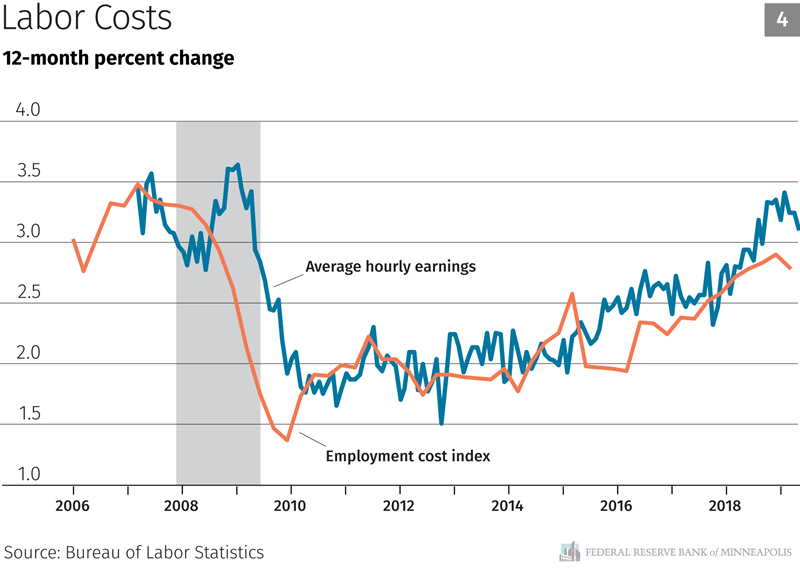

But perhaps inflationary pressures are building that we aren’t yet seeing in the data. I look at wages and costs of labor as potentially early warning signs of inflation around the corner. If employers have to pay more to retain or hire workers, eventually they will have to pass those costs on to their customers. Ultimately, those costs must show up as inflation. But we aren’t seeing strong upward movement in these data. The orange line in Chart 4 is the employment cost index, a measure of compensation that includes benefits and is adjusted for employment shifts among occupations and industries. The blue line is the average hourly earnings for all employees. Both lines have moved up in recent years and are roughly flat over the past year. Importantly, productivity growth has also climbed in recent years, so these higher wage growth levels, net of productivity, still do not signal high future inflation. In short, while the cost of labor is climbing slowly, it isn’t showing signs of building inflationary pressures that are ready to take off and push inflation above the Fed’s target.

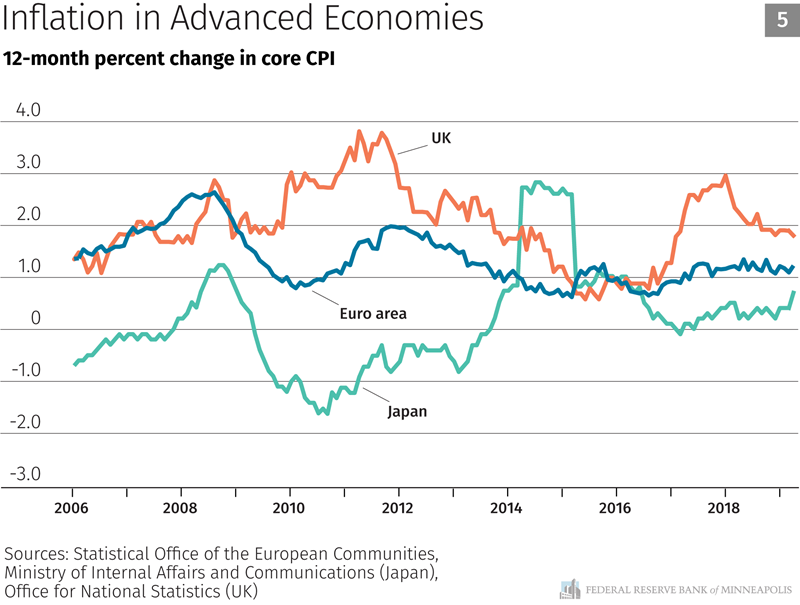

Now let’s look around the world. Most major advanced economies have been suffering from low inflation since the global financial crisis. It seems unlikely that the United States will experience a surge of inflation while the rest of the developed world suffers from low inflation. As you can see in Chart 5, with the exception of the UK, which has experienced high inflation due to currency depreciation resulting from Brexit uncertainty, core inflation rates in advanced economies continue to come in below their targets. Despite aggressive monetary policy strategies, both Japan and the euro area have struggled to achieve their inflation targets.

In summary, inflation has moved further below our target, and market-based measures of inflation expectations remain at low levels and are still falling. Some argue that the decline in inflation this year is transitory, but we don’t know that for certain, and the longer it persists, the more tenuous the transitory factors story becomes.

Maximum Employment

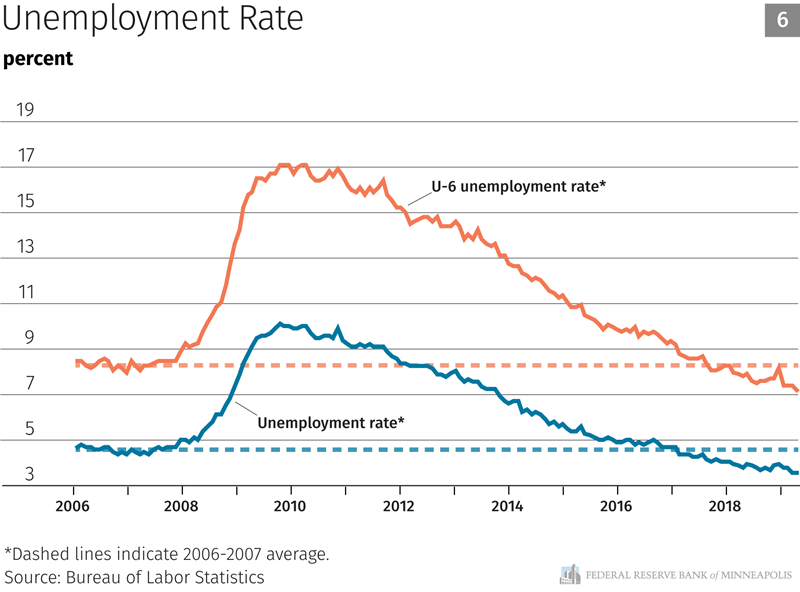

Next let’s look at our maximum employment mandate (Chart 6). One of the big questions I continue to wrestle with is whether the labor market has fully recovered or if there is still some slack in it. Over the past few years, some people repeatedly declared that we had reached maximum employment and that no further gains were possible without triggering higher inflation. And, repeatedly, the labor market proved otherwise. The headline unemployment rate has fallen from a peak of 10 percent to 3.6 percent, below its precrisis level. We also look at a broader measure of unemployment, what we call the U-6 measure, which includes people who have given up looking for a job or are involuntarily stuck in a part-time job. The U-6 measure peaked at 17.1 percent in 2010 and has fallen to 7.1 percent today, also below its precrisis level. But these measures still leave out a large number of people who might prefer to work if better job opportunities were available to them.

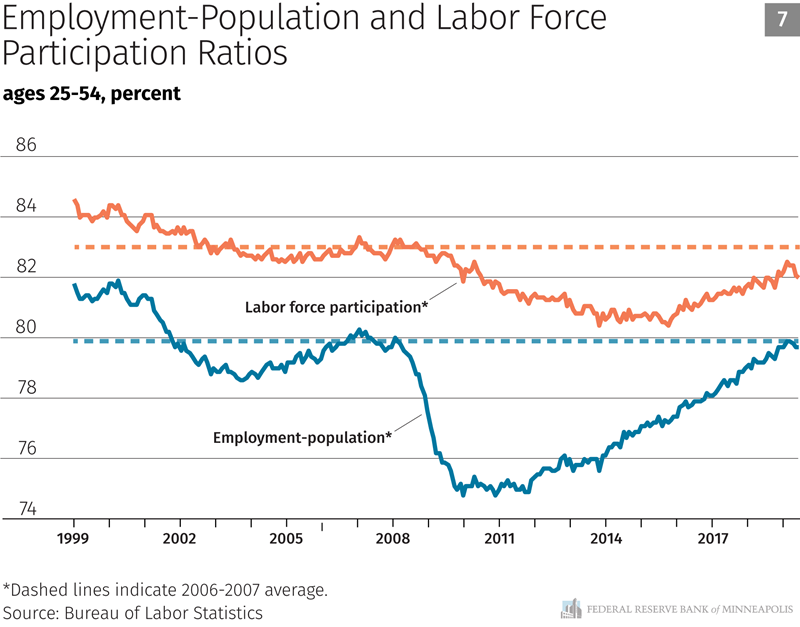

The employment-to-population ratio and the labor force participation rate capture the percentage of adults working or actively looking for work. We know these are trending downward over time due to the aging of our society (as more people retire, a smaller share of adults are in the labor force). To adjust for those trends, I prefer to look at these measures by focusing on prime working-age adults. Chart 7 shows that, with the strong job gains in recent years and the decline in unemployment rates, the labor market appears to have recovered to its precrisis strength but, going back further, there still may be room for improvement.

It is important to note that job growth has slowed in recent months from an average of 223,000 jobs per month in 2018 to 164,000 per month so far in 2019. While that job growth still exceeds the roughly 100,000 per month needed to keep up with population growth, wage growth also appears to have leveled off. If we were reaching maximum employment, I would have expected job growth to slow and wage growth to pick up as firms competed for scarce workers. The fact that job growth and wage growth are both slowing suggests weakening economic growth rather than an economy running out of workers.

The bottom line is that the job market has improved substantially, and we are getting closer to maximum employment. But we likely aren’t there yet. In 2012, the midpoint estimate among FOMC participants for the long-term unemployment rate was 5.6 percent—the FOMC’s best estimate for maximum employment. We now know that was too conservative—many more Americans wanted to work than we had expected. If the FOMC had declared victory when we reached 5.6 percent unemployment, millions of additional workers would have been left on the sidelines.

Given that we simply don’t know how many more people will choose to work if wages pick up further, how will I know if we are at maximum employment? When I see wage growth, net of productivity, of at least 2 percent. That will at least indicate the possibility that we are at maximum employment. That threshold nonetheless ignores the potential for labor’s share of national income to increase, which would allow wage growth to increase further without triggering higher inflation. We should be open to that possibility.

We also know that the aggregate national averages don’t highlight the serious challenges individual communities are experiencing. For example, while the headline unemployment rate today for all Americans is 3.6 percent, it is still 6.2 percent for African Americans and 4.2 percent for Hispanics. The broader U-6 measure, mentioned above, is roughly double the headline rate for each group.

Current Rate Environment

OK, so we are still coming up short on our inflation mandate, and while we are closer to reaching maximum employment, we likely aren’t there yet. Let’s have a look at where we are now: Is current monetary policy accommodative, neutral, or tight?

I look at a variety of measures, including simple rules such as the Taylor rule, to determine whether we are accommodative or not. There are many versions of such rules, and none are perfect.

One concept I find useful, although it requires a lot of judgment, is the notion of a neutral real interest rate, sometimes referred to as R*, which is the rate that neither stimulates nor restrains the economy. Many economists believe the neutral rate is not static, but rises and falls over time as a result of broader macroeconomic forces, such as population growth, demographics, technology development, and trade.

There are a range of estimates for the current neutral real rate. Having looked at them, I have argued in recent years that the neutral rate is in the range of zero to 50 basis points. With the federal funds rate at 2.25 to 2.50 percent, and inflation at around 1.5 percent, that implies that the current real federal funds rate is between 0.75 percent and 1.0 percent, which is restrictive relative to these estimates of neutral. If inflation were running at our 2 percent target, policy would then be in the range of neutral. These estimates are highly uncertain. It seems likely that policy is somewhere between neutral and moderately restrictive. Given the lack of inflation pressures and potential remaining slack in the labor market, I want to make sure policy is not restrictive, and I believe we should err on the side of providing accommodation. This supports my policy recommendation to cut rates.

Financial Stability Concerns

Please see my essay on how I think about monetary policy and financial stability. In short, while some asset prices appear elevated, I don’t see a correction as being likely to trigger financial instability. Investors would face losses from a stock market correction, but it’s not the Fed’s job to protect investors from losses. Our jobs are to achieve our dual mandate and to promote financial stability.

Global Environment

The global economy appears to be slowing with weak growth in Canada, output declining in Mexico, slowing activity in China, and the European Central Bank considering additional stimulus. In addition, trade tensions have added to global uncertainty.

Flattening Yield Curve

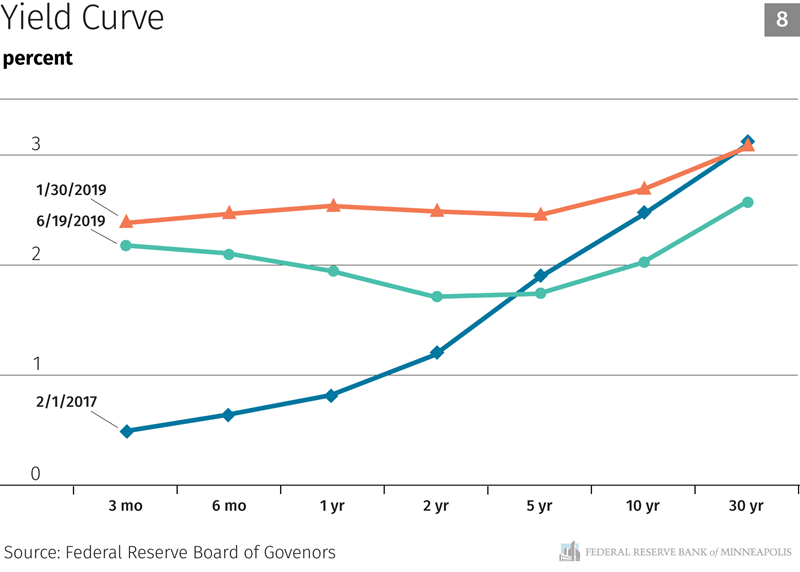

The yield curve has flattened dramatically in recent years and has actually inverted in recent months. An inverted yield curve, where short rates are above long rates, is one of the best signals we have of elevated recession risk and has preceded every single recession in the past 50 years.

I believe the FOMC’s rate increases in recent years have directly affected the yield curve: As the FOMC has raised rates, the front end of the curve has moved up with our policy moves, which is to be expected. But because the Committee raised rates in a low-inflation environment, we were sending a hawkish signal, which was also likely holding down the long end of the curve by depressing inflation expectations. It is important to note that even after the Committee announced its pause of further rate increases in January of this year, long rates continued to come down, further inverting the curve. Those more recent moves were likely driven by the markets expecting a lower R*, slower economic growth, or lower long-term inflation. All of these potential signals suggest that monetary policy may be too restrictive.

Policy Tools

The FOMC’s plan to shrink its balance sheet was well-telegraphed in advance of implementation and is proceeding on schedule—due to end in September of this year. I don’t think the remaining roll-off over the next few months is having much effect on the overall stance of policy. I am agnostic as to whether to end the roll-off earlier than September.

What Might Be Wrong?

What if low inflation really is transitory and surprises us to the upside in a few months’ time? In my view, that will be a high-class problem. If core inflation crosses 2 percent on a sustained basis, my policy proposal allows the Committee to then raise rates at that point. A much more worrying risk is that the slowing job growth and inverted yield curve are signaling further economic weakness and further declines in inflation expectations. In my view, the cost of cutting rates early is much smaller than the cost of cutting too late. If we wait until we are sure the economy is slowing and inflation expectations fall further, it will be much harder for us to reverse those concerning developments and sustain the economic expansion.

Conclusion

Over the past few months, the job market has slowed, wage growth has flattened, inflation has continued to come in below our 2 percent target, inflation expectations have fallen, and the yield curve has inverted. I believe the FOMC should take strong action to re-anchor inflation expectations at our 2 percent target and support strong job growth, higher wage growth, and sustained economic expansion. The best way I can think of to do that is for the Committee to cut rates by 50 basis points and then commit to not raising rates until core inflation returns to our target on a sustained basis.