Author

Alison Phillips

Senior Quant Analyst – Capital Markets

Familiar kinds of consumer debt such as mortgages, car loans, and credit cards—as well as home equity loans, other revolving credit plans, and other single-payment and installment loans—make up the retail lending portfolio for banks. In the last quarter of 2018, retail loans accounted for 42.2 percent of banks’ total loan dollars in the Ninth District and 40.5 percent in the United States as a whole.

Broadly speaking, there are four major categories of retail loans. Residential loans consist of mortgages secured by 1- to 4-family residential properties, home equity loans, and home equity lines of credit. Credit card lending consists of the reported outstanding balance on all extended credit card accounts. Auto loans are the balances of any loans extended for the purchase of new or used consumer vehicles. Other loans, the final retail loan category, include revolving lines of credit that are not accessible through credit cards, loans for educational and medical expenses, loans for the purchase of household goods such as furniture or appliances, loans for personal debt consolidation or taxes, and loans for various other personal expenditures as long as they do not fit into one of the preceding loan categories.

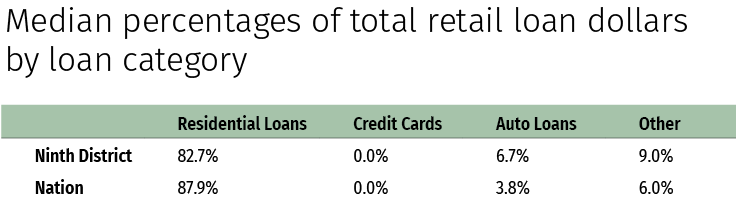

Within the typical bank’s retail loan portfolio, mortgages and home equity lines of credit accounted for the majority (over 80 percent) of loan dollars at the end of 2018. The median percentages of total retail loan dollars by retail loan type are shown in the table. The Ninth District retail lending portfolio looks similar to that of the nation, though we do see a slightly higher share of auto and other lending and a corresponding lower share of residential loans.

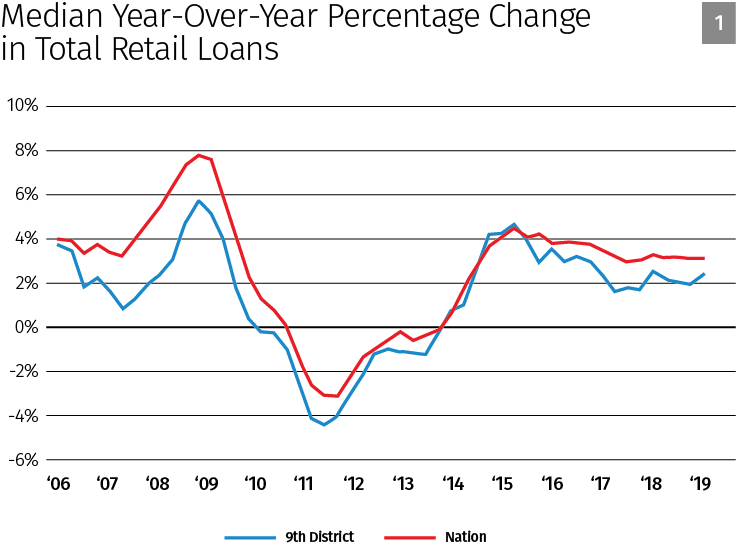

Quarterly changes in retail lending balances are predictably cyclical in nature. Looking at year-over-year changes in retail lending helps remove the complicating factor of seasonality from the picture. Additionally, banks within the Ninth District vary greatly in terms of both size and retail lending portfolio composition. Using median values to examine growth in lending gives a better representation of trends at a “typical” bank in the Ninth District.

With cyclical seasonality and bank dominance accounted for, we can see in Figure 1 that retail lending for the typical Ninth District bank has followed the path of retail lending at the typical bank nationwide, with slightly slower rates of growth. After the 2007-2008 financial crisis, Ninth District growth in retail loans slowed for about a year before turning negative in 2010. Beginning in about 2014, median rates of retail lending began to increase again, both in the Ninth District and nationally.

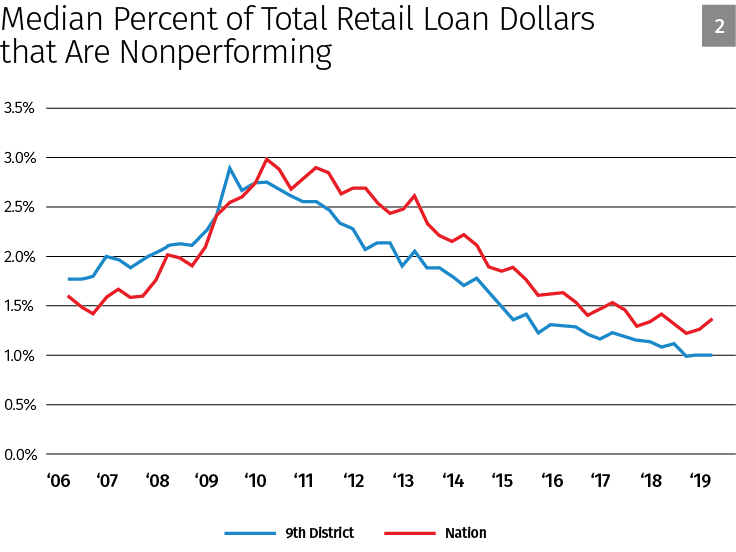

Another dimension of retail lending health is the extent to which retail loans are past due. In Figure 2, nonperforming loans are those that are greater than 30 days past due and/or are no longer accruing interest. Before and heading into the crisis, the typical Ninth District bank had a greater proportion of nonperforming retail loans than the typical U.S. bank, and the proportion of nonperforming loans was on the rise. However, the Ninth District saw a shift in trend around the end of 2008. Since the crisis, the typical percentage of nonperforming retail loans has steadily decreased in the Ninth District and has stayed below the typical U.S. bank’s percentage of nonperforming retail loans. A review of disaggregated Ninth District nonperforming retail loans shows that the different types of retail lending follow similar paths.

Size and performance data suggest that the Ninth District’s retail lending portfolio is relatively healthy. Though growth in retail lending at the typical Ninth District bank is positive, it is not outpacing growth at the typical bank nationwide. Moreover, the median Ninth District bank’s ratio of nonperforming retail loans to total retail loans is below that of the median bank across the nation and continues to be on a downward trajectory.