Author

Kristina Martin

Quantitative Analyst

Over the past 10 years, the composition of the wholesale lending portfolio at the median Ninth District bank has been more volatile than and somewhat different from the composition at the median national firm. The trends in growth and shrinkage of the median wholesale portfolio in the Ninth District have largely tracked with national trends, though the troughs have been deeper and the peaks shallower in the Ninth District. A deeper dive into the data around wholesale lending over the past decade reveals ways in which the Ninth District follows and differs from national trends, and which Ninth District states drive this behavior.

Wholesale lending comprises loans from banks to businesses, which make up a considerable portion of total bank portfolios. Businesses of all sizes take out loans for construction or purchasing new facilities, corporate expansion, and other expenses. In the last quarter of 2018, wholesale lending comprised about 48 percent of the loan portfolio at the median national bank and about 42 percent of the loan portfolio at the median Ninth District bank. In general, wholesale lending falls into two categories: commercial real estate and commercial and industrial. CRE loans include financing of land development, construction, or purchase of residential properties and nonfarm, nonresidential properties. C&I loans include any other loans to businesses that are not secured by real estate.

| Proportion wholesale loans to total loans in Q4 2018 | Net change in wholesale proportion from Q1 2009 to Q4 2018 | |

|---|---|---|

| National | 48.2% | 0.0% |

| Ninth District | 41.8% | -1.5% |

| Minnesota | 42.7% | -1.5% |

| Montana | 49.9% | -2.7% |

| North Dakota | 26.0% | -2.0% |

| South Dakota | 25.6% | -1.0% |

Table 1 shows the share of total lending made up of wholesale loans in the last quarter of 2018 at the median bank nationally, in the Ninth District, and in each of the four core Ninth District states: Minnesota, Montana, North Dakota, and South Dakota. The wholesale lending program at the median bank in the largest Ninth District state, Minnesota, is a similar size to the median Ninth District bank, at about 43 percent and 42 percent, respectively. But there is more variation in the smaller Ninth District states. Wholesale lending at the median bank in Montana accounted for about half of total lending, while at the median banks in both North and South Dakota, wholesale lending accounted for about a quarter of total lending. The median Ninth District firm is distinct from the median national firm with respect to change in the proportion of total loans comprising wholesale loans over the past 10 years. Table 1 also shows that from the first quarter of 2009 to the last quarter of 2018, the median national firm saw no change in the relative size of its wholesale lending portfolio, while the median Ninth district firm saw a 1.5 percent shrink.

| Wholesale portfolio composition in Q4 2018: Median C&I/Median CRE | Five-year net change in wholesale portfolio composition | 10-year net change in wholesale portfolio composition | |

|---|---|---|---|

| National | 27% / 73% | +0.8% CRE | +1.4% CRE |

| Ninth District | 35% / 65% | +1.4% CRE | +2.5% CRE |

| Minnesota | 35% / 65% | +0.6% CRE | +2.3% CRE |

| Montana | 28% / 72% | +1.9% CRE | +0.7% CRE |

| North Dakota | 44% / 56% | +3.8% CRE | +10.2% CRE |

| South Dakota | 43% / 53% | +2.3% CRE | +2.5% CRE |

Table 2 shows the composition of wholesale lending portfolios at the median bank nationally, in the Ninth District, and in Ninth District states in the last quarter of 2018. Wholesale lending at the median Ninth District bank has been more concentrated in C&I lending than at the median national bank. In the last quarter of 2018, C&I loans comprised 35 percent of the wholesale portfolio at the median Ninth District bank, compared with 27 percent at the median national bank. Nonetheless, both in the Ninth District and nationally, CRE loans account for the significant majority of wholesale loans, at 65 percent and 73 percent, respectively. The picture is more nuanced when looking at individual Ninth District states. The ratio of median C&I to CRE loans in Minnesota tracks the Ninth District ratio, while the Montana ratio is closer to the national ratio. North and South Dakota are distinct from both the median national and Ninth District firms, with both states having a higher median share of C&I loans at about 44 percent. At all levels of granularity, there has been a shift in the median wholesale portfolio from C&I to CRE loans. Table 2 shows the net change over the past 10 years and over the past five years in median C&I and CRE proportions. Over the past decade, the median firm nationally, in the district as a whole, and in Minnesota, Montana, and South Dakota all saw 1 percent to 3 percent of their wholesale portfolios shifting from C&I to CRE loans. North Dakota saw a much bigger swing, with about 10 percent of the wholesale portfolio at the median firm moving from C&I to CRE loans.

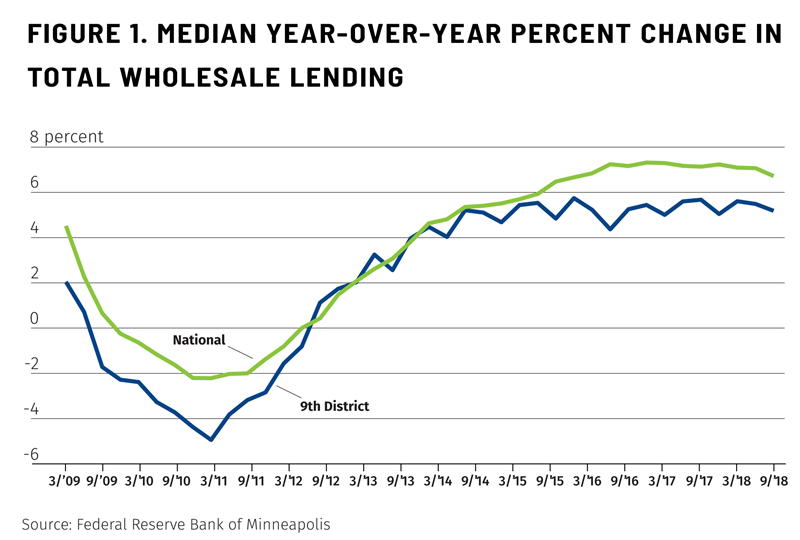

We can draw another comparison by measuring the growth of the wholesale lending market over time. A good way to measure the progression is to consider the year-over-year percent change in the size of the loan portfolio at each bank. The median year-over-year percent change, shown in Figure 1, gives a sense of the typical firm behavior and is not heavily swayed by a few firms having a high concentration in a particular business line. Both nationally and in the Ninth District, we see a shrink in wholesale lending in the years following the financial crisis. Though the Ninth District followed a similar path to the national trend, the District trough was more pronounced: The minimum change was a 5 percent shrink in 2011, when the national minimum change was a less than 3 percent shrink. Wholesale lending began to expand both nationally and districtwide in approximately 2012. Since 2015, wholesale lending has been largely flat, with more volatility in the Ninth District than nationally. Wholesale lending at the median Ninth District firm has grown more slowly over the past 10 years than at the median national firm. One source for this divergence is the observation made in Table 2, that Ninth District banks tend to have larger exposures to C&I lending and less exposure to CRE lending than the typical bank outside the district. C&I lending has grown more slowly than CRE lending, and the larger exposure to the slower-growing category contributes to the lower growth in total wholesale loans.

The median Minnesota and Montana banks closely follow the district trend. The median South Dakota bank tracks more closely with the median national bank, though with more volatility. The median North Dakota bank has followed a distinct pattern over the past decade, with a much smaller shrink after the financial crisis followed by steeper growth. While change in wholesale lending at the median firm in other Ninth District states leveled out around 2016, wholesale lending at the median North Dakota firm started to shrink at that time. North Dakota has seen a recent recovery in wholesale lending, with expansion starting around 2018.

A comparison of national, Ninth District, and state-level data exposes the ways in which the median Ninth District firm behaves similarly and how it differs from the median national firm. The data show that the composition of the median Ninth District wholesale portfolio has moved closer to the composition at the median national firm. Year-over-year growth is smaller in the Ninth District than nationally, but not dramatically so. A view of the state-by-state growth is more nuanced and indicates that while the biggest Ninth District states have driven district trends, the smaller Ninth District states show distinct behavior. A view of the data at all of these levels of granularity gives a rich picture of the evolving trends in wholesale lending over the past decade.