Author

Article Highlights

- Increasing economic clout of richest Americans is one likely culprit as college tuition more than doubled in past 30 years

- Commentators point to rising expenditures by colleges, but spending is responding to greater demand from the wealthy

- Self-reinforcing cycle might be slowed by assisting smart, low-income students with grants large enough to help them attend better schools

American families don’t need an economist to know that the cost of college is soaring. So is the debt many students carry long into adulthood. Recent research from the Minneapolis Fed shows how growing U.S. income inequality could be driving the trend.

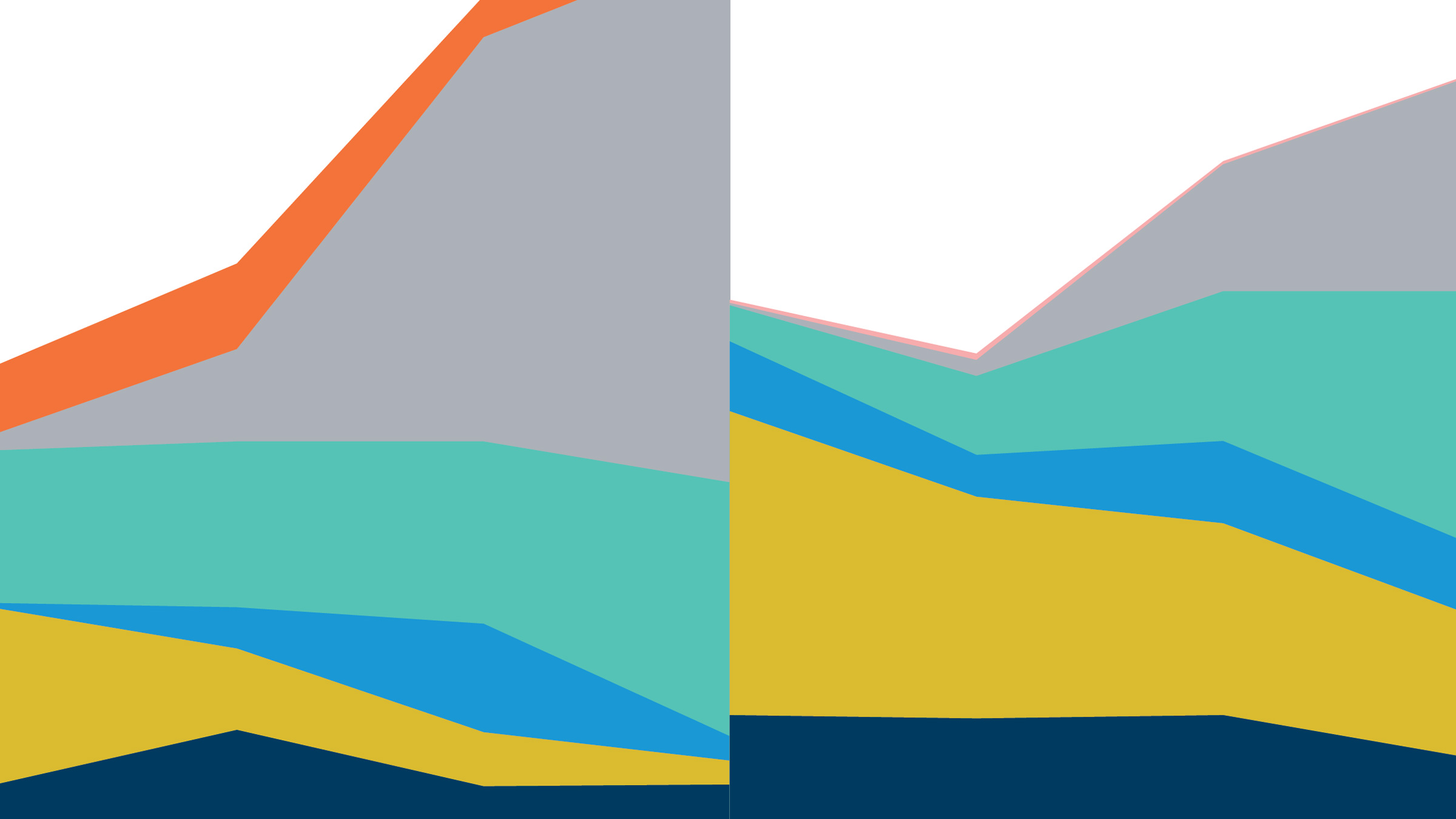

Since 1990, the sticker price of a four-year private college degree has doubled, even accounting for inflation. Public colleges are more affordable, but their price has grown even faster (Chart 1). The net out-of-pocket price that students pay has grown more moderately, but that’s because someone else—taxpayers, for the most part—foots the bill through financial aid. Total awards of Pell grants, the primary federal tool for helping low-income families with college tuition, more than tripled during this same period, with big increases in the average award size and number of recipients. Yet today’s average Pell award—just over $4,000—still lags far behind the escalating cost of a college degree.

In this context, Minneapolis Fed Monetary Advisor Jonathan Heathcote was struck by a chart from a well-known paper on income inequality by economist Raj Chetty and co-authors. The striking, simple graph shows a straight-line correlation between family income and the likelihood of attending college—from just 20 percent of the lowest-income young adults to nearly universal higher education for the richest families. A second set of data points shows an unmistakable relationship between family income and the quality of the college.

“It’s remarkable that there’s such a strong correlation between parent income and where kids are going to college,” Heathcote recalls thinking. “Are there low-income students getting priced out, and is that going to change as income inequality goes up?”

In a Minneapolis Fed staff report (and forthcoming paper in the American Economic Review), Heathcote and Zhifeng Cai of Rutgers University demonstrate that income inequality isn’t just a result of these disparities in higher education. Rather, widening inequality in the United States is itself driving up the price of college. This depresses enrollment by putting college out of reach for some intelligent but low-income students. The inequality effect can also help explain the steep rise in expenditures on financial aid.

Modeling the market for higher ed in an unequal world

Since 1989, American working households at the 25th percentile of the distribution have seen their incomes rise around 8 percent. Incomes of the wealthiest families have grown 44 percent (Chart 2). Crucially, for understanding the market for college, the rich are indeed getting richer. “The top is really where the action is for this paper,” says Heathcote.

Cai and Heathcote construct an economic model where colleges compete for students in a complex environment featuring need-based financial aid, in-state tuition discounts at public schools, the risk of dropping out, and students who vary academically. Their model also incorporates two real-life features that many previous papers have not: First, the quality of colleges is allowed to vary along a continuous spectrum. Second, this quality depends in part upon the quality of a school’s student body—so-called peer effects, which Heathcote considers an essential feature to understand the economics of college pricing.

The economists calibrate their model using data going back to the 1989-90 academic year, from sources including the U.S. Department of Education, the Federal Reserve’s Survey of Consumer Finances, and the National Longitudinal Survey of Youth.

Rising tuition, stunted enrollment, and more financial aid

The paper’s headline finding arises when the economists impose today’s much higher income inequality on the U.S. higher education market of 1989. The increased inequality—with all else held constant—prompts a cascading series of economic effects:

- An increase in sticker and net tuition. In the model, the increase in inequality from 1989 to the present day is responsible for almost 60 percent of the increase in net tuition observed during this period. (The remainder of the increase is attributable to the overall rise in average incomes.)

- A drag on enrollment. While the growth in average incomes does increase enrollment overall, the effects of growing inequality restrain that growth. That’s because …

- More low-income and middle-income families opt out of college or choose lower-quality colleges in the face of rising costs. This action contributes to …

- A lower average quality of student bodies, as high-quality students from lower-income families choose not to attend, and …

- A drop in the number of low-quality (but less expensive) colleges, further restricting options for low-income students, and finally …

- A surge in college spending and government subsidies on financial aid, as colleges compete to attract the shrunken pool of high-quality, low-income students, who need even more financial assistance to attend.

Given underlying economic growth and government subsidies, college enrollment still increases even under rising inequality. However, much of this growth is composed of low-ability students from wealthy families, who have comparatively more money to spend.

Many contemporary theories about the rising cost of college focus on the “supply side.” Popular commentators point to fancy fitness centers or a perceived increase in faculty salaries. Cai and Heathcote instead put the focus—and the blame—back on the demand side, driven by the growing buying power of high-earning American families who also send almost all of their offspring to college.

“Our perspective is that everybody (at the high end) is willing to pay more,” says Heathcote. “So colleges’ costs are going up because they’re spending more on what these students and their parents are willing to pay for.”

Inequality generates higher prices, which increase inequality … and on it goes

The result here is not a market failure or inefficiency. The higher education “producers” are doing what we would expect in a competitive market; consumers are making informed decisions about which college to attend or whether to attend at all. In that sense, there’s nothing to “fix” from a purely economic perspective.

However, it’s a challenge for a society that values fairness and equality of opportunity. This is especially so in light of what we observe about the economic returns to a college degree versus a high-school diploma or from a top college versus lower tiers. If inequality is driving college prices higher, and the returns to a college degree then reinforce income inequality, Heathcote says, “you can think of colleges as perpetuating income inequality across generations.”

Cai and Heathcote don’t include policy indications in their paper. However, one insight is that increasing targeted education grants can slow this effect loop of widening inequality. Under tight competition for quality students, colleges will turn that additional funding into lower tuition or better instruction. Helping high-ability, low-income students to attend high-quality schools would rebalance the market away from the effects described above.

While it provides crucial assistance for more than 7 million low-income students, the relatively inflexible Pell grant program might not be a match for the wider economic effects shaping college affordability. Pell grants have risen slightly faster than inflation, but still cap out at around $6,000. So while those grants do induce some marginal students to enroll in college, they do not help them attend more expensive, higher-quality schools.

Heathcote doesn’t doubt that some colleges genuinely strive for income diversity. However, their efforts are arrayed against powerful macroeconomic forces, and even those with best intentions still need to pay the bills and compete with their peers. He also acknowledges that the market for higher education—like many markets in the real world—is likely replete with economic imperfections, opening avenues for future study and extensions of his model.

“Having a child who is about to apply to college, it’s a little bit hard to get your head around this college experience,” Heathcote says. “It’s unlike any other market you can think of.”

Jeff Horwich is the senior economics writer for the Minneapolis Fed. He has been an economic journalist with public radio, commissioned examiner for the Consumer Financial Protection Bureau, and director of policy and communications for the Minneapolis Public Housing Authority. He received his master’s degree in applied economics from the University of Minnesota.