Authors

Stefanie Aschenbrenner

Financial AnalystDan Hartzheim

Financial AnalystRichard Jamieson

Financial AnalystRenee Pederson

Financial Analyst

Anna Stagg

Communications Coordinating Editor

Article Highlights

- PPPLF supports lenders who provide forgivable PPP loans to the smallest businesses impacted by COVID-19

- Nonbank PPP lenders reach small businesses without traditional banking relationships

- Small business lending companies share their journey through PPP lending

In 2020, the Minneapolis Fed was given a special assignment in response to the COVID-19 pandemic—to set up and lead one of the Federal Reserve System’s emergency lending facilities. The Paycheck Protection Program Liquidity Facility, or PPPLF, was created jointly with the U.S. Treasury for the purpose of supporting lenders who provide even the smallest businesses with forgivable loans through the Small Business Administration’s Paycheck Protection Program, or PPP.

Emergency lending in action

First, a quick review of the PPP: the Small Business Administration (SBA) started the PPP at the beginning of the pandemic once the program was established by the CARES Act. The PPP provides payroll support to small businesses. PPP loans are guaranteed by the SBA and are forgivable if loan proceeds are used to keep employees on the payroll or pay related expenses. The first round of PPP funding was available from April to August in 2020.

To increase the effectiveness of the PPP, the Federal Reserve established the PPPLF as an emergency lending program, with the Minneapolis Fed at the helm.1 The PPPLF was designed to supply liquidity to SBA-approved PPP lenders in order to increase their lending capacity and confidence to make PPP loans. The PPPLF is similar to other emergency lending facilities set up during the 2007-08 financial crisis that provided backstop funding to a wide variety of markets.

On April 16, 2020, the PPPLF began operations by making advances to banks, savings associations, and credit unions. On April 30, 2020, the Federal Reserve expanded the PPPLF to include nonbank PPP lenders, such as community development financial institutions (CDFIs) certified by the U.S. Department of the Treasury, small business lending companies licensed and regulated by the SBA, agricultural credit associations that are members of the Farm Credit System, and some fintech firms.

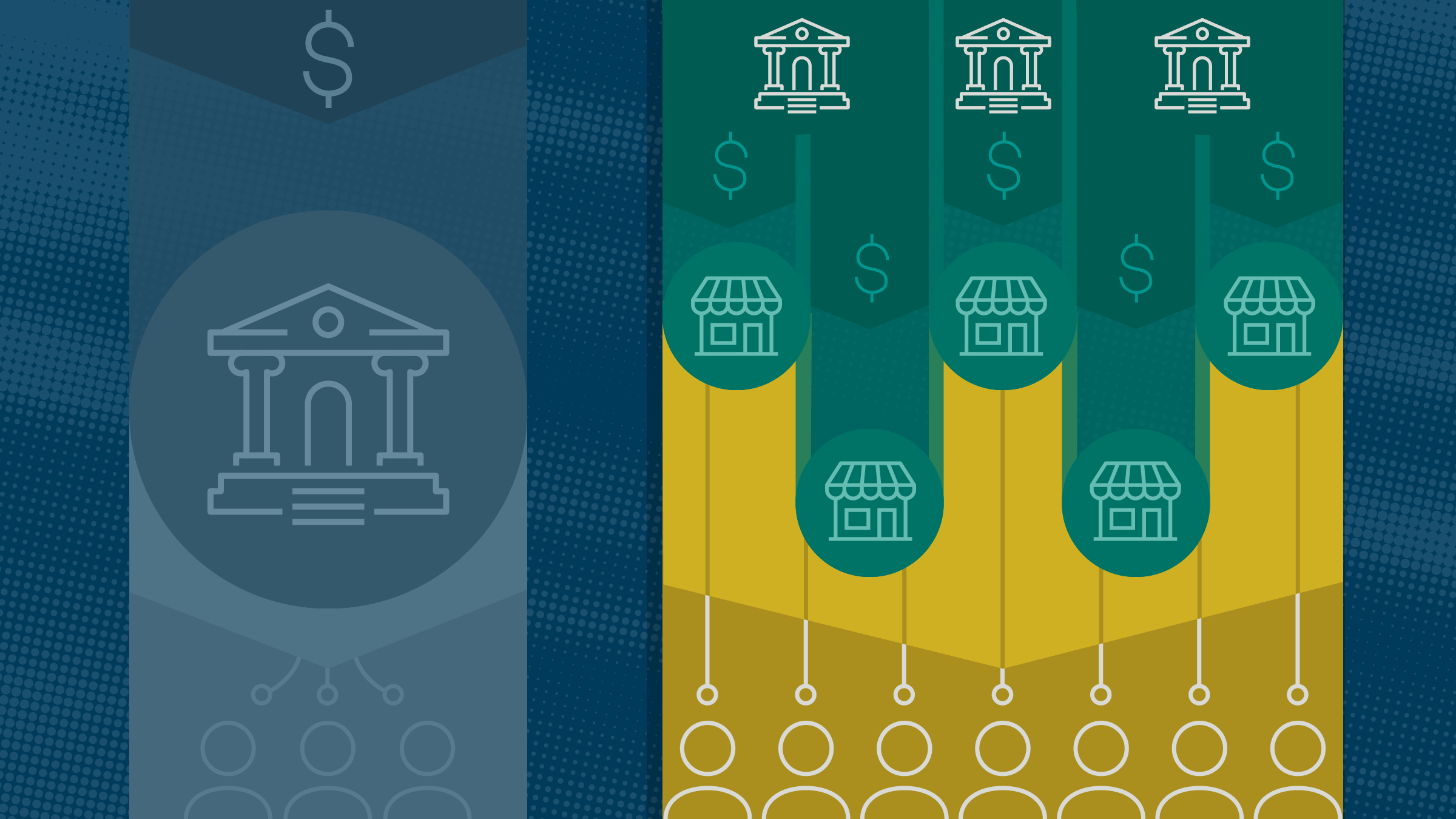

The image below depicts the relationships between the small business owners, PPP lenders, and the Federal Reserve.2

How the PPPLF works

A second round of PPP funding, established by the Economic Aid to Hard-Hit Small Businesses, Nonprofits, and Venues Act, was available from January to May of 2021. Through May 31, 2021, the SBA had approved 11.8 million PPP loans totaling $800 billion.

Among banks that have participated in the PPPLF, community banks (those with $10 billion or less in assets) received more than 90 percent of total PPPLF advances.3 One of those community banks that is also a certified CDFI is Sunrise Banks of St. Paul, Minn. When asked about Sunrise Banks’ participation, Chief Executive Officer David Reiling said that “this is an opportunity that represents a ‘bigger than us’ moment. We’re being called to serve our country and get these funds out the door so we can keep people employed and keep our economy running. Together we need to save Main Street.”

PPPLF volume overview

As of May 2021, north of $80 billion in liquidity was extended to PPPLF participants. For nonbanks, their participation in the PPPLF has steadily increased as the figure above shows. Nonbanks frequently reached small businesses that may not have traditional banking relationships. The average PPP loan originated by nonbanks was significantly smaller than that of banks.

How PPP lenders helped meet the need

PPP lenders who borrowed from the facility each had specific reasons to participate. We asked a few participants about their journey through PPP lending and how the facility has helped them better serve their customers. Here’s what they had to say:

Brian Choi, chief financial officer, speaking for Centerstone SBA Lending Inc., Los Angeles, Calif.: The PPP has impacted our organization in a very positive way, from allowing us to provide the much-needed assistance to our existing 7(a) borrowers as well as to provide PPP loans to new borrowers, allowing them to continue operations and, more importantly, to continue to pay employees in these uncertain times. As we transitioned to PPP round two in 2021, we were able to expand our PPP borrower base from approximately 900 to over 1,800, representing approximately $109 million and $160 million in total PPP funding, respectively. The two rounds of PPP not only assisted the thousands of small business owners by providing the extra liquidity needed to continue to fund payroll and keep businesses open, but it also helped our organization through origination fees earned for each PPP loan funded.

Without the Federal Reserve’s PPPLF, our organization would not have been able to fund the number of loans (volume and dollar amount) that we did, as we are not a depository institution and heavily rely on our warehouse line with our banking institution to fund our loans. That we had access to credit with the PPPLF’s lower interest rate made originating PPP loans economical for our organization. We would not have been able to help the thousands of small business owners without the PPPLF.

Throughout this process, we were able to forge close relationships with our borrowers. We received many words of praise and appreciation from our borrowers, and we were happy that we could play a part, however small, to assist small business owners during this time.

Chris Hurn, chief executive officer, speaking for Fountainhead SBF LLC, Lake Mary, Fla.: The PPP enabled us to help a tremendous number of small businesses in their time of need. We sacrificed a significant amount of our time and resources to help out, but we were honored to be in a position to contribute so much to so many. The turmoil of the time also had the added benefit of bringing our team much closer together, despite most working from home. We sometimes say that we squeezed 10 pressure-packed years into that time period (since last April), which improved all of our skills immeasurably.

As one of the very first (if not the first) small business lending companies to utilize the PPPLF, we knew how important this access to liquidity would be for us and our ability to fund more small businesses. Without it, we simply wouldn’t have been able to be as impactful as we were. The PPPLF was a critical piece of our operations.

This has been a tremendous public-private partnership in the truest sense, and we’re very grateful to have been a part of it.

Luke Lahaie, chief investment officer of ACAP, speaking for the Loan Source Inc., New York, N.Y.: The PPP has been a catalyst of growth for our organization. By focusing on the PPP, we have been able to establish and grow one of the largest SBA-focused servicing companies (ACAP) in the U.S., as well as help the Loan Source become one of the country’s largest nonbank SBA lenders.

The PPPLF has been the key to executing our growth plan for the PPP. Without the PPPLF, we would not even have gotten started with our purchase or origination program. The amount of liquidity needed and low rate of interest on the underlying loans prevented us from obtaining third-party funding for PPP loans. The Fed’s program to establish the PPPLF was the difference maker for us to participate (we now have originated over $11 billion in loans), and from my discussions around the industry, it’s been instrumental for banks and nonbanks alike to participate in the program. Without the PPPLF, I think the entire PPP effort would have been smaller scale and only participated in by larger banks. Additionally, there would not be a secondary market. The secondary market has proven valuable for banks that were able to originate loans but don’t have the infrastructure and/or desire to service the loans for two to five years.

Mark Schmidt, chief executive officer, speaking for Fund-Ex Solutions Group LLC, Syracuse, N.Y.: The PPP had a profound impact on our small and relatively new company. We were just starting to hit stride when the pandemic arrived in March. After a few weeks of uncertainty about whether to participate and to what extent (primarily due to funding constraints), the PPPLF solved our funding issues, and we pivoted quickly to PPP. We threw almost all of our company’s resources at the PPP—along with about 40 staff members that were “borrowed” from our parent company.

The rapidly evolving nature of the PPP and the overwhelming immediate needs of small businesses posed many challenges, but we were able to meet those challenges thanks to the tireless efforts and incredibly long days, hours, and weeks on the part of FSG staff. We also focused heavily on customer service and provided hands-on assistance to a large majority of our PPP borrowers. We are proud to say that our young company has advanced over $220 million in PPP loans to over 1,400 small businesses with about 20,000 total employees.

Without the PPPLF, we would have had extremely limited means with which to finance PPP loans, especially given the 1 percent interest rate on those loans. We most likely would have made very few PPP loans and focused primarily on our existing small business 7(a) borrowers. In other words, PPPLF made all the difference for FSG and is the sole reason we were able to participate in the PPP.

From my perspective, the PPP was a resounding success. That could not have happened without the tremendous efforts of all who contributed—including the SBA, Treasury, Federal Reserve, and lending staff. Despite the time pressures and uncertainties—especially in the early days of the program—many thousands of businesses and employees were helped during this particularly difficult and unprecedented crisis.

Minneapolis is honored to play a part

From banks to nonbanks, PPP lenders were able to reach more borrowers, keep more employees on the payroll, and ultimately decrease COVID-19’s negative impact on many more businesses and individuals than would have been possible otherwise. The Minneapolis Fed, on behalf of the Board of Governors, is honored to be part of this public-private partnership through our role supporting the liquidity and stability of the U.S. financial system.

Endnotes

1 The PPPLF was established with approval of the Secretary of the Treasury, under section 13(3) of the Federal Reserve Act.

2 See also Conversations with the Fed session presentation by Christine Gaffney, "Paycheck Protection Liquidity Facility: Supporting American Workers in a Time of Crisis," April 6, 2021.

3 Board of Governors of the Federal Reserve System, Financial Stability Report, May 2021, p. 33 (accessed June 18, 2021).