Author

If public infrastructure were a student, it would appear to be the kid who couldn’t quite hack it.

If public infrastructure were a student, it would appear to be the kid who couldn’t quite hack it.

The American Society of Civil Engineers (ASCE) regularly grades the condition of many types of infrastructure nationwide, and it’s not pretty. In the latest report in January, solid waste infrastructure got the best grade at C+, and things only got worse from there—three other C’s and 11 D’s, including a D– for such critical matters as drinking water, roads and wastewater.

But like the kid in real life, infrastructure didn’t get to this lousy performance on its own, or on purpose. Call it the public-sector kid who fell through the cracks—lots of potential, but didn’t get the attention needed to perform well. Reports abound regarding the critical importance of infrastructure, its deteriorating condition and the desperate need to do something about it. Headline-grabbing failures of infrastructure—the collapse of the Interstate 35 bridge in Minneapolis, the flooding of New Orleans—bring pointed attention to the matter, but little change in overall direction, strategy or committed investment.

Government, for its part, nods knowingly about the infrastructure problem and pulls out its empty pockets in a mea culpa. Maybe next year we’ll find some money. Oh, wait, there’s a recession and huge budget deficits. Lemme get back to you.

In the midst of this quagmire, there has been growing support and activity for a new model of infrastructure investment, nondescriptly called a “public-private partnership,” or PPP. This general model is not exactly new—governments have long worked with private firms to provide public goods and services. But the perceived crisis in infrastructure has created opportunities for even greater private involvement, giving private firms de facto ownership and the chance to reap profits through good management and innovation, or bear losses for poor performance.

PPP is currently more active at the international level, but slowly gaining traction in the United States. Despite their growing popularity, PPPs don’t necessarily offer an inherently better model for infrastructure than traditional government procurement. But PPPs offer a new source of capital and a way around the endless political tussle for funding that is responsible for much of the infrastructure problem. The upshot: PPPs can help government address infrastructure needs faster.

There are trade-offs, of course—most notably, higher user costs. PPPs also require a certain leap of faith: Though research suggests that PPPs can deliver on performance promises, the movement is still immature in many respects. The most innovative approaches come with considerable risk and are not yet time-tested, particularly in the United States.

Men not at work

One element almost everyone agrees on is the poor condition of the nation’s public infrastructure. (The term “public infrastructure” carries many connotations; its use here refers to goods whose efficient marginal user price is zero to promote maximum use and benefit for all citizens. As a result, public infrastructure is produced and maintained by government because the private market cannot generate a profit at such a price and therefore produces too few of these goods. Stick that definition in your memory cache; I’ll come back to it because it has a direct bearing on the PPP trend.)

Amid all those failing grades, the ASCE estimates that $2.2 trillion in investments are needed over just the next five years to bring U.S. infrastructure to a healthy level. Some argue that such figures amount to nothing more than a wish-list of gold-plated roads and bridges. Regardless of the exact figure, there is widespread agreement that the nation’s infrastructure needs attention, badly.

Though most of the attention is paid to roads and bridges, the infrastructure problem is much broader. The nation’s electricity grid is bottlenecked. Prisons are overcrowded. Many cities are exposed to floods, and New Orleans still isn’t protected from the next Katrina. The latest figures from the Environmental Protection Agency show a need for more than $200 billion over 20 years to control wastewater pollution and another $277 billion over a similar time frame to comply with drinking water regulations.

The United States arrived at this deficit slowly, the gradual result of how public infrastructure systems are funded and maintained. Traditional funding mechanisms for roads and bridges, for example, are not keeping pace with demand. The federal Highway Trust Fund, a key funding mechanism for highways nationwide, could have a negative balance as early as 2012. According to 2008 projections by the Congressional Budget Office, federal gas tax receipts are expected to increase by just 20 percent (to $45 billion) by 2018—well below the typical rate of inflation over such a period, never mind the expected increases in overall traffic and transport tonnage.

Distribution of those highway funds is not particularly efficient either, at least if the goal is economic growth. Thanks to funding distribution formulas, gas and motor vehicle taxes paid by drivers in growing cities like Houston, Las Vegas and Atlanta often benefit drivers in Montana or Alaska, where projects affect considerably fewer people. Supposedly “dedicated” state transportation funds are often raided for other priorities.

In a report last year, the Federal Highway Administration (FHWA) acknowledges “a growing recognition in the United States that traditional approaches to funding and procuring highway and transit projects are failing. … Governments across the country are having a difficult time keeping up with the demand for transportation investment. Scarce transportation resources are increasingly misallocated for political or special purpose spending. … Advancing a major project from concept to completion often takes well in excess of ten years, making it extremely difficult for the public sector to respond to transportation priorities.”

The federal stimulus package passed earlier this year might give the impression that at least roads and bridges are seeing some necessary investment. But the final package includes not quite $50 billion for transportation projects. For argument’s sake, say that money is split equally among states. That $1 billion in California “might buy you a five-mile segment of highway. In Virginia, it might get you some HOV lanes,” said Leonard Gilroy, director of government reform for the Reason Foundation, a free-market think tank. “It’s not going to do a thing to (overall) infrastructure needs.”

Now stir in the fact that the federal government faces the prospect of ongoing, trillion-dollar deficits. Go down one level, and you’ll find that states had a cumulative mid-year budget gap for fiscal year 2009 of about $50 billion. Next year’s gap is projected to be even higher. State aid to local government will undoubtedly get pared back as a result, compounded by lower local property tax revenue from a devastating housing slump.

The invisible helping hand?

Problems like these have many thinking there might be—indeed, must be—a way out of this enormous pothole. And that’s where the discussion segues to public-private partnerships.

PPP can mean many things. Some basic forms of PPP are quite familiar. Government has long outsourced or otherwise contracted certain services to the private sector. The Department of Defense spends tens of billions of dollars on weapons procurement from private firms like Lockheed Martin; states pay construction firms to design and build bridges and roads; many cities contract with private companies to collect and dispose of garbage; social services are often handled by nonprofit firms.

For public infrastructure, the underlying model is being expanded by offering private firms more control and de facto ownership of assets. In this “concession model” of PPP, government leases control of an asset—say, an existing or proposed bridge—for a fixed period of time, anywhere from 10 to 99 years (though the real envelope-pushing is occurring in the longer contracts). In exchange, the private firm (or firms, typically) is allowed to recoup investments and ongoing operating costs through concessions—most often user fees, like freeway tolls. Government typically retains legal ownership of the asset, and sets the conditions and standards for the ultimate return of that asset to the public sector.

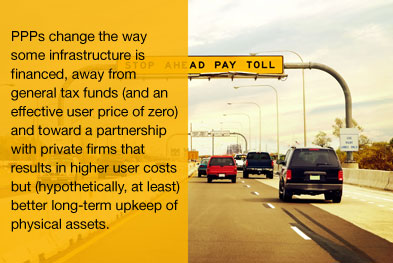

In a nutshell, concession-based PPPs change the way some infrastructure is financed, away from general tax funds (and an effective user price of zero) and toward a partnership with private firms that results in higher user costs but (hypothetically, at least) better long-term upkeep of physical assets. From a theoretical standpoint, the PPP concession model holds no real advantage over the traditional government financing model. But PPPs are gaining attention because of the reality of short-term government budgeting decisions and their cumulative effect on infrastructure maintenance. A deep pool of available private investment gives PPPs the added attraction of being able to tackle improvements in high-demand areas much more quickly than traditional procurement.

No joke: Bridge for sale

Governments across the country—indeed, the world—are kicking the PPP tires, often because there are financial incentives for handing over the infrastructure keys. This concession model undergirds the sale (lease, actually) of such major public assets as the Indiana Toll Road, a 157-mile stretch of freeway in the northern part of the state, which fetched $3.8 billion from private investors in 2006 in exchange for toll proceeds for 75 years.

Texas is a PPP hot spot for a number of reasons. In 2007, it approved a major tollway project with the Spanish firm Cintra for a congested highway near Dallas, and a significant pipeline of PPPs was reportedly getting organized. But people were queasy with the overall pace of PPPs, and the state put a moratorium on new toll roads. The state later pulled out of the Cintra deal.

The moratorium has since been lifted, and this past January, a private group (NTE Mobility Partners) was conditionally awarded the initial work on a multistage project for the 36-mile North Tarrant Express, also in the Dallas region. Under the 52-year agreement, $2 billion in funding (most of it private) will be used to design, construct, operate and maintain a new highway system (with toll and nontoll roads) that will double capacity by 2015. Tolls will vary from $1.20 to $6.50, depending on traffic congestion, and proceeds will be shared between the state and its private partners. NTE will also develop master plans for the rest of the corridor.

“Our legislators have seen that [PPP] is another fundamental tool to provide [infrastructure] improvements sooner,” said Jodi Hodges, a public information officer with the Texas Department of Transportation. The estimated cost for improving the entire corridor is about $5 billion. But annual highway construction letting (those projects authorized to seek bids) is only $2 billion for the entire state of Texas, she said. “So already you see a disparity.” Using PPPs, the North Tarrant Express will be upgraded much more quickly than through traditional procurement, which Hodges said “would be years, years.”

Governments at all levels are entertaining PPPs for different types of projects, like seaport improvements in Oakland and the Port of Virginia. Last year Florida saw the construction and opening of its sixth and largest private prison. Since 2005, long-term concession toll roads have been either proposed or closed on in at least 13 states, according to the FHWA.

Chicago is a veritable PPP test tube: In 2005, it leased the Chicago Skyway, an 8-mile freeway, for $1.8 billion with a 99-year lease. A year later, it leased 9,500 city-owned parking spaces for $563 million for 99 years. It followed that up in 2008 with the 99-year lease of 35,000 parking meters and several municipal parking lots for $1.2 billion. (Whether governments in Chicago and elsewhere are pursuing PPPs for the “right” reasons is another debate entirely. Oftentimes PPPs are done for short-term budget reasons—to raise cash to close budget deficits or fund other government priorities—rather than to address infrastructure needs. But an analysis of how these upfront payments are used by governments is outside the scope of this article.)

Get your hands off my infrastructure

Critics believe such partnerships are heresy to the very notion of public infrastructure. These opponents of PPPs are uncomfortable with the perceived sale of public assets to private interests (in reality, these transactions are leases, not outright sales). Private firms then stand to make a profit by charging users (taxpayers) for access to something they previously used for free and believed was already paid for.

But the reality is more complicated than that criticism suggests. Ultimately, both the infrastructure problem and the PPP opportunity stem from how government has historically viewed the cost and subsequent pricing of infrastructure. One of the reasons government builds highways, the theory goes, is that private markets will not do so when user charges are effectively zero and there is no opportunity for profit. But government, as history reveals, is not particularly efficient or effective at maintaining either infrastructure assets or a system’s overall performance.

For example, all public infrastructure systems have capacity limits that can quickly get overwhelmed when user costs are zero. In populated areas, congestion is taken for granted, but it’s an inefficient outcome. The ASCE estimates that 45 percent of urban highways are congested, and Americans spend 4.2 billion hours a year stuck in traffic, costing the economy some $78 billion a year, or $710 per motorist. At the same time, governments are hard-pressed to come up with the funds necessary to expand capacity. And when user prices are zero, there are no pricing mechanisms available to smooth demand and make better use of existing capacity.

Even more problematic in the long run, governments neglect maintenance. When new projects are planned, the only thing that goes on the books is the upfront capital expenditure, giving little or no upfront funding to substantial maintenance needs over the lifetime of an asset. Instead, maintenance costs are assumed to be funded by future budgets. While some maintenance funding is included in every budget, it is typically insufficient for proper long-term upkeep. That’s because in the real world of government budgets, elected officials arm-wrestle over short-and long-term needs. When that happens, immediate needs like health care, disaster recovery and education typically win over mundane long-term needs like road patching.

According to a 2007 needs assessment by the National Surface Transportation Policy and Revenue Study Commission, just 19 percent of the $147 billion spent on roads and bridges by all levels of government in 2004 went for maintenance; 48 percent went to capital expenditures, and the remainder went for things like traffic operations, highway patrol, department administration and debt payments.

The problem is that over the life span of a road, maintenance costs are significant and worsen if neglected, making catch-up costs exponentially higher. If you own a house, you know the problem: Fail to fix your roof in a timely manner, and you’ll soon have many more things to repair. Neglected maintenance eventually turns minor repair into costly replacement—which, ironically, is often marketed as a more efficient investment of scarce infrastructure dollars. According to the NST study, slightly more than half of all capital expenditures for transportation in 2004 went toward “system rehabilitation” rather than new or expanded roads.

Without proper maintenance, a road might have a life span of just 20 years, when it should be 60 to 80 years, according to Daniel Dornan, a director at the accounting firm KPMG, in Orlando, Fla., and a widely consulted expert in infrastructure valuation and PPPs.

“The problem is time,” Dornan said. He compared infrastructure maintenance to dental visits. “If we only lived for five years, we’d never go.” But the incentive to maintain oral health rises significantly if you believe you’ll live a long life. The same mentality holds for infrastructure: Policymakers have a short-term budgeting perspective and don’t see the need for the regular care of jackhammers and crack filling for infrastructure. The incentives in the public sector are “spend it now. Don’t worry about the future. We’ll get more money later,” said Dornan, echoing a theme voiced by others.

There’s no U.S monopoly on such budget challenges, either. In Canada, government “doesn’t have trouble getting money to build things. But the hardest thing was to see us build something and then not have the money to do maintenance,” said Jane Peatch, executive director of the Canadian Council for Public-Private Partnerships. (In Canada, PPP is referred to as P3.)

Peatch came out of the public sector herself, having previously worked as a city planner and infrastructure adviser. She points out that elected officials are aware of life-cycle costs and the need for maintenance, and some try to do the right thing. “No government willingly says, ‘We’re going to let that road fall apart.’ But politicians have so much pressure on them” to react to immediate needs.

Peatch became a believer in P3 because she “could see no way of practicing the theory” of proper infrastructure maintenance. “[P3] seemed like a more certain model—you weren’t struggling anymore” to properly manage assets for long-term use, Peatch said. There are still political fights, she said, but the P3 fight is short term and focuses on the utility of P3 and getting the terms of a P3 contract right. “But then for 35 years, you don’t have to come back and fight every year for money” to maintain that asset.

Peatch acknowledges that if governments were able to properly budget for life-cycle costs, “you’d have a harder time proving that the [long-term P3] contract is better. … [But] government doesn’t have the discipline.”

Many are skeptical that PPPs can induce a life-cycle focus, particularly through the involvement of private firms, where the lure of short-term profits might convince firms to cut corners. But firms have to follow maintenance and performance requirements outlined in contracts—standards that are often higher than those required of public agencies, according to accounts from both the FHWA and Government Accountability Office.

Firms also respond to incentives, Dornan and others say, and PPPs have the ability to reward firms for keeping their eye to the future. When entering into long-term agreements, for instance, firms will do things upfront—“you’ll design it right, inspect it closely”—so it ages well, cutting down on maintenance needs while maintaining performance (and thus revenue), according to Dornan. Firms also will not put off maintenance because the only way to turn a profit in a decades-long PPP is to avoid costly replacement, Dornan says. “That’s where the magic occurs.”

However, the arguments both for and against concession-based PPPs are still mostly theoretical; for example, whether concessionaires can meet high standards over a lengthy contract is still to be determined, because the handful of concession-based PPPs in the United States are just out of their contract starting gate.

But PPPs already face a public relations problem as user costs rise under them. Tolls for motorists on the Chicago Skyway have increased from $2 to $3, and the contract authorizes regular hikes to $5 by 2017. Costs on the Indiana Toll Road went from $4.65 to $8 for a car traveling the entire road; semitrailers saw their tolls almost double.

A new U.S. import

Although some might see the trend in concession-based PPPs as a major leap into a privatized abyss, in reality it has evolved rather slowly.

Part of the reason that the United States hasn’t had to deal with infrastructure problems until fairly recently is because much of the nation’s infrastructure was built from the mid-1950s through the 1970s and was seemingly functional. But over time, system maintenance needs have grown, congestion has worsened and funding to fix either has become problematic. The search for solutions has led to a gradual movement toward more user fees and private-sector involvement.

A January 2009 report by the FHWA says that toll roads are becoming an important source of highway funding; 235 toll roads have been either proposed or developed since 1992. And as tight budgets put a lid on capital funding, more state and local transportation authorities “are currently considering the use of PPP … than at any comparable time in U.S. history.” Already there are two dozen toll roads with private involvement in nine states. A similar number of recent proposals have the possibility of private involvement. Among 45 toll bridges, 10 had either confirmed or possible private involvement. Neither is this a great departure or exception from past practice; electricity and water infrastructure have significant private involvement.

In fact, the United States is simply catching up with the rest of the world, where various forms of PPP are more mature. Australia, Canada and western European countries have a decade or two of experience. The global headwaters for PPP lie in the United Kingdom, where it’s called the Public Finance Initiative. PFI has been around since the early 1990s and focuses on private-sector involvement in all forms of public infrastructure, including health care facilities, roads and schools. Since 1992, 790 PFI projects have been signed (worth almost 54 billion pounds) and about 500 completed, according to PPP Forum, an industry body representing the UK firms involved in PFI. From a flat-footed position in the mid-1990s, PFI projects now represent 10 percent to 13 percent of all U.K. investment in public infrastructure, according to a 2007 report by Deloitte Research.

Invest in our future (profits)

Behind this growing international trend in PPPs is a simple but fundamental force: private investment money. The National Council for Public-Private Partnerships (NCPPP) estimates that over $400 billion in private funding for infrastructure projects was available as of February 2009.

Over the past few years, investment funds dedicated solely to infrastructure projects became something of a trendy investment, though the shine has come off in the midst of current turmoil in financial markets. The reason for the growing interest is equally simple: Returns were good, generally ranging from 8 percent up to the higher teens. Whether or not those returns hold in the current environment is tough to say. Before the collapse of financial markets, some talked of hypergrowth for infrastructure investment funds—on par with recent growth in real estate and private equity niches—because of documented global infrastructure needs. But there were also whispers of a bubble, with too much money chasing too few serious PPP proposals. The winning bid of $1.8 billion for the Chicago Skyway by the Macquarie Infrastructure Group (MIG) was reportedly $1 billion more than the next-highest bid.

Like other areas of finance, private infrastructure deals had become highly leveraged, and that’s a death knell in today’s market environment. “The outlook for the near term remains grim,” with fewer deals closing and many put indefinitely on hold, according to a December 2008 report by PricewaterhouseCoopers. “Bank debt is simply insufficient and inefficient as a source of long term finance.” That means future PPPs will probably require more equity, which will likely terminate or mothball proposals with borderline or volatile revenue projections. In April, for example, an expected $2.5 billion deal for a 99-year lease of Midway Airport fell through for Chicago when investors could not raise the necessary funding.

Still, according to Seth Miller, NCPPP deputy executive director, the slump in financial markets has slowed, but not stopped, the development of PPPs. “The criteria for equity and debt investment have become more strenuous, but not prohibitive.” He noted that a number of major deals have closed in the past year, including the $2 billion North Tarrant Express in Texas.

Some, like Miller, believe infrastructure investment funds ultimately have good staying power and could benefit from the skittishness in the investment world: Unlike the obtuseness of financial derivatives, PPPs offer a hard asset and a relatively straightforward investment model. Infrastructure serves many users, which should create a steady and relatively predictable revenue stream and a decent investment return. Today’s investors are also more willing to accept modest returns for lower risk than they might have a few years ago, according to Miller. “Considering the experience of the last year, you can see why this shift is now under way.”

It’s not perfect

Empirical evidence is stacking up that PPPs can deliver on promises of greater efficiency. A 2003 U.K. Treasury report found that more than 75 percent of PFI projects were on budget, and a similar percentage were delivered on time. That compares with less than 30 percent on both measures for non-PFI construction projects.

A December 2008 study by researchers at the University of Melbourne looked at 67 transport, water, information technology and social infrastructure projects in Australia, 25 of which were PPPs and 42 traditionally procured. It found that “PPPs delivered projects for a price that is far closer to the expected cost than if the project was procured in the traditional manner.”

Few such analyses exist in the United States, but the Army’s Residential Communities Initiative offers some insight. It contracted with private builders to upgrade and expand 88,000 units of Army housing. A 2008 review found that the program had leveraged about $10 billion in new private capital to tackle the housing problem, cleared a backlog of work estimated at 20 years and built housing in 15 to18 months versus three to five years using the traditional Army approach.

Still, even ardent supporters acknowledge the limitations of PPPs for addressing the nation’s infrastructure needs. “PPPs cannot provide for all public needs. They are simply not a panacea,” said NCPPP’s Miller.

That’s because there are limitations to their applicability, as well as short-term and long-term hurdles to overcome. For example, concession-based PPPs are only realistic for projects that offer high utilization, cash flow and opportunity for profits. That means PPPs are unlikely to be seen much outside of high-use or high-toll projects, at least in the near term. Still, PPPs can theoretically help rural infrastructure by freeing up scarce government resources that would otherwise be spent to address infrastructure problems in high-cost metro areas.

The PPP movement also is likely to evolve slowly because the United States does not have the regulatory or statutory framework necessary to facilitate such projects. The United Kingdom and some other countries have centralized authorities that coordinate a host of PPP activities. But the United States has nothing of the sort, which means local and state governments enter mostly at their own risk. Currently, about half of the states have passed enabling legislation allowing PPPs for transportation projects, according to Miller.

More important in the long run is the ability to establish contracts that produce desired results for all parties—quality service, protection of the public interest and the generation of profits for the firms involved. This is very soft ground for the simple fact that PPPs are young and immature; even among the United Kingdom and other countries with a 10- or 15-year head start, no country has enough experience with concession-based PPPs to be certain of final outcomes, especially amid current economic and political upheaval.

Some recent PPPs are already struggling from the recession. Macquarie Infrastructure Group announced in February that traffic on a number of its U.S. tollways was disappointing; use of the Indiana Toll Road had slumped by 15 percent in the second half of 2008, and cash flows reportedly were barely covering interest payments by the end of the year. In February, MIG announced a half-year loss of $1.7 billion, much it from heavy write-downs on the value of its toll roads.

The very existence of contracts means that PPPs suffer from high transaction costs as government seeks private bidders for services it used to produce on its own and must now supervise to boot. More difficult still, PPPs suffer what economists call incomplete contracts, or the inability of parties to anticipate important matters that might otherwise be included in a contract. This includes things like major contingencies (such as a big shift in demand in either direction, or a natural disaster), knowledge gaps (future advances in technology) and identification of performance criteria that are agreeable and verifiable to both parties (such as safety improvements).

At the same time, these matters do not appear entirely intractable; indeed, the United States could well benefit from being a relative latecomer by avoiding the hard lessons learned by early adopters elsewhere. The experience of PPPs to date also suggests that multistage contracting that renegotiates terms in a planned fashion to incorporate new information—such as unexpected windfall profits or catastrophic losses—can better link the long-term satisfaction of all parties.

Advocates acknowledge that PPPs face many hurdles and a cynical public. They lament that PPPs are typically framed as an either-or choice, as though PPPs are crowding out the public sector. “It’s presented as a false choice—PPP or else,” said Gilroy, from the Reason Foundation. “PPP is not a replacement. It’s supplementing and augmenting [the current system] and stimulating a lot of internal change” regarding the way society thinks about and manages its infrastructure.

Gilroy also notes that more policymakers from both sides of the ideological spectrum are beginning to see the advantages of PPPs, in part because the alternative is to see nothing get done. He believes that public discomfort would change if PPPs could tackle some high-profile projects that have long piqued the public’s interest but seemed politically unlikely or fiscally unfeasible—like making dramatic improvements in transit. In terms of scaling up PPP activity, said Gilroy, “if you could get PPP done [successfully] for transit, forget it, the lid’s off.”

Ron Wirtz is a Minneapolis Fed regional outreach director. Ron tracks current business conditions, with a focus on employment and wages, construction, real estate, consumer spending, and tourism. In this role, he networks with businesses in the Bank’s six-state region and gives frequent speeches on economic conditions. Follow him on Twitter @RonWirtz.

Related Content

Related Content