Author

“Imagine you want to start a family,” said University of Minnesota economist Victor Ríos, a Minneapolis Fed consultant. “It’s bad news for you if houses are very, very expensive. But it’s good news if the job market is good. We wanted to see which was more important: Is it better to start in good economic times, when labor income is high and houses are expensive, or to start in worse times, when labor income is lower but houses are much cheaper?”

The question—a straightforward explanation of a recent study by Ríos and three other economists—is clear-cut. Arriving at an answer, however, called for a remarkably intricate piece of research into the distributional consequences of severe recessions, resulting in a 75-page paper with seven technical appendixes.

“Intergenerational Redistribution in the Great Recession” (Minneapolis Fed Working Paper 684), by Andrew Glover, Jonathan Heathcote, Dirk Krueger and José-Víctor Ríos-Rull, approaches the problem through the context of a severe economic downturn that affects wages and asset prices not only for young households just starting out, but also for older cohorts who have accumulated wealth over the course of their economic lives. How will these different age groups experience the simultaneous shock to labor markets, on the one hand, and housing, stock and bond markets on the other?

The short answer to the simple question: The young do better. Recessions are hard on everyone, but they’re “much worse for the old,” observed Heathcote, a Minneapolis Fed senior economist. “They’re painful for the younger households, but not so painful.”

The long answer is, well, considerably longer—more nuanced and far more intriguing. The central finding, for example, that the young fare better depends crucially on the assumption that prices of assets (on which older cohorts depend for income) experience a greater than proportional decline than do wages (on which the young most rely). That assumption is consistent with the U.S. experience during the Great Recession of 2007-09, and that is where the economists begin their investigation.

Assets, income and the recession

“I guess the starting point was when we looked at the data,” noted Krueger of the University of Pennsylvania. “It’s not so surprising, but we found a tremendous heterogeneity across age groups in the quantity of assets they hold. For young people, it’s really not much, so they have perhaps not so much to lose [in a recession]. Most of the financial assets and real assets are held by the elderly. So it is to be expected that a recession when asset prices fall a lot would not affect everybody the same.”

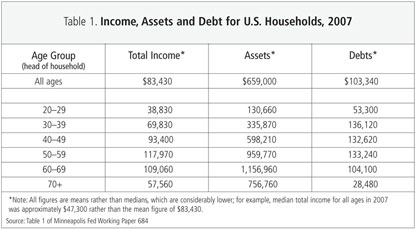

The economists document this heterogeneity with data from the Survey of Consumer Finances (SCF), conducted by the Federal Reserve every three years, including 2007 when asset prices were near their peak. As seen in Table 1, they find that the average annual figures of $83,430 in income, about $660,000 in assets and $103,000 in debt obscure enormous variation among age groups. The youngest households (headed by 20- to 29-year-olds) had $39,000 in average annual income, about a third that of the 60- to 69-year-old households. The assets of the youngest were just 11 percent of those of the senior households, but their debt levels were half as large, leaving them with average net worth just 7 percent of that of the average 60- to 69-year-old household.

Figure 1 depicts this variation graphically with lines indicating life-cycle patterns for labor income and net worth from the youngest to the oldest households. Labor income (including Social Security payments) is actually lowest for the households (headed by those) 70+ years old, slightly below the 20-29 age group, and reaches its zenith for peak earning years in the 50s. Household net worth climbs with age until the 60s and then begins to decline.

But this was the picture in 2007, before the onset of the Great Recession. To estimate its impact on households of different ages, the economists examine asset portfolios of different age groups in 2007, looking at the range of holdings from risky assets like stocks and real estate to less risky holdings like bonds and certificates of deposit. They then estimate quarterly price declines for each element of household net worth and revalue household portfolios accordingly from the second quarter of 2007 to the first quarter of 2009, when asset values bottomed out.

This careful statistical exercise generates a pattern of the recession’s redistributive effect among age groups. The average household saw a net worth decline of $176,000, accounted for mainly by an average decline of $79,000 in stock value and another $77,000 loss from diminished housing net worth. But, again, the heterogeneity of impact was dramatic. “Losses varied widely by age,” observes the working paper. “Younger households lost much less [about $30,000], while those in the 60-69 year age group lost the most: $310,000 on average, or nearly four times average annual income for this age group.”

While their income loss was smaller in an absolute sense, the young lost a huge chunk of their net worth since they tended to be in greater debt than older cohorts (proportionately) in 2007. The youngest lost almost 40 percent of their net worth, but the oldest suffered only a 27 percent drop. Households headed by the 30-39 age group actually suffered the greatest decline, almost 45 percent, due to high real estate leverage and stock portfolios nearly twice as big as those of the 20-29 age group when the recession began.

Figure 2 depicts this pattern for the six age groups at two moments in time: the first quarter of 2009, when asset values and net worth were at their nadirs, and the fourth quarter of 2010, after losses were substantial, but less so. Again, the picture of losses for all, but wide variation by age group, is apparent.

With this, the recession’s impact on asset values and thereby on net worth by age group, the economists have provided an empirical base for their deeper examination. Economic welfare losses were unevenly distributed, but “a more complete analysis requires forecasts for the future evolution of labor income and asset prices,” they write, “and an understanding of how agents will optimally adjust savings and portfolio choice behavior in response to expected future wage and price changes.”

Variations on a model

The picture of decline and variety among generations is clear, but illustrating the key mechanisms behind it requires a mathematical model, and that is the primary focus of the paper—developing a model with several age groups that can examine each generation’s response to economic shocks. And it’s with such a model, in which asset prices adjust in response to a slump in aggregate economic output—that is, a severe recession—that they build a “theoretical link between the dynamics of income, consumption and savings on the one hand and asset prices on the other.”

The data drive the economists’ decisions in shaping their model. First, because age groups vary widely in labor income and net worth, they differ in risk exposure. For quantitative analysis, therefore, the economists need “an overlapping-generations life-cycle model with aggregate shocks.” Second, since portfolio allocations vary widely among generations, meaning age variation in net worth response to shocks, the economists consider models with both risky and safe assets. Third, because younger workers are far more likely to become unemployed during recessions than older workers, and the latter are likely to sustain income flows via Social Security payments, the economists need a model in which recessions change not just the level, but the shape, of the age-earnings profile. It is, in short, a complicated analysis.

And to better understand exactly how the model works, the economists test it through examination of four “example” economies. The process enables them to gauge the importance of various features—including age groups, for instance, or people’s willingness to delay consumption until a later time—all experiments to illuminate the key mechanisms at work. What is it, precisely, that accounts for the magnitude of asset price changes relative to movements in economic output? And what determines how asset price movements translate into welfare effects that vary across generations?

The first economy is quite simple: a “representative agent” economy in which there’s no difference among age groups in their reaction to economic shocks—everyone exhibits the same response. This simple example is a “useful benchmark” for examining the link between gross domestic product (GDP) and asset prices, they note, but “has nothing to say about differential welfare effects across age groups,” their primary interest.

So the economists build three more variations, each incorporating a new feature. In another of their examples, households live through three time periods: young, middle-aged and old. As young households, they begin with no assets, don’t value consumption and buy as many stocks as they can afford. As old households, they sell all their stocks.

In this variation, “only the middle-aged make an interesting intertemporal decision,” write the economists, “trading off current versus future consumption.” And their decision is crucial. In a recession, the middle-aged have to weigh needs in the present against those anticipated as they age. To smooth consumption, they’ll want to sell stocks and spend the proceeds on food, clothing and other living expenses. But as stock prices fall in a recession, they also have an incentive not to sell their stock so that they can gain higher expected returns in the future—when they become old households. These two tendencies—“income” and “substitution” effects—counter one another.

Asset price intuition

Running through this series of examples allows the economists to thoroughly analyze which features are critical to determining the size of asset price declines relative to output and to measure the implications for different generations. And, gradually, this careful exploration of model variations yields the following intuition about asset price movements: Much depends on (a) the share of wealth held by the middle-aged and (b) the willingness of all households to tolerate fluctuation over time in what they’re able to consume or, as economists call it, their “intertemporal elasticity of substitution.”

Why? First recall the assumption that young households begin their economic lives with no assets; this means that all wealth is held by either old or middle-aged households, and the old rely on selling off their assets to provide current income (and therefore consumption). When the middle-aged sell their assets, only the young are in the market, not the old. So, if middle-aged households anxiously sell off their stocks in a recession (to smooth their own consumption flows), stock prices fall, the young scoop up stocks at low prices and the wealth of old households is severely depleted. Thus, the share of wealth held by the middle-aged has a crucial impact on everyone’s well-being after the start of a big recession.

The second critical factor: the intertemporal elasticity of substitution, or IES. The economists write that the logic for asset prices being more sensitive to output declines when this elasticity is low is “familiar and straightforward.” Well, right—maybe if you too are an economist. Basically, the IES is a measure of responsiveness of consumption to price changes. If a small price increase convinces you to not buy something now, or to delay purchases, you have a high IES—you’re flexible in your consumption decisions and quite responsive to price changes. But if it takes a large jump in price to make you stop buying, your IES is low. Algebraically, the IES is the inverse of risk aversion (or to be more technically precise, this is true in utility functions generally used by macroeconomists).

Dirk Krueger, Jonathan Heathcote and José-Víctor Ríos-Rull

Said Ríos: “If you really hate to lower your consumption, the price has to do a huge job to induce you to eat less.” Added Krueger: “If people really do not like their consumption to change over time, then prices have to fall a lot to convince them at dire times not to eat, but to save.” For this analysis, they choose a benchmark figure of 1/3 for the IES (or, conversely, a risk aversion of 3), though some research pegs it closer to 1/2. Why 1/3? In the recent Great Recession in the United States,” says the working paper, “asset prices fell roughly three times as much as output.” Or as Krueger elaborated, “Output fell by 8.3 percent relative to trend. Three times that means the asset price fall would be on the order of 25 percent, which is about where house prices are, and financial prices were not so long ago, relative to their peak values.”

In a nutshell, taking these two decisive factors into account, the economists’ analysis of the impact of a severe recession on asset prices is this: The less willing households are to endure changes in consumption, the more asset prices will decline—relative to output—in a recession. And the higher the share of total wealth the middle-aged hold, the more asset prices will react to changes in aggregate output.

Figure 3 illustrates these findings. It plots responsiveness (or elasticity) of asset prices to output as a function of the share of wealth held by the oldest generation for two values of elasticity of substitution.

First compare the red and blue lines. The red line shows results when households aren’t very willing to put up with consumption variability. In that case, the less wealth held by the old—meaning the more held by the middle-aged—the greater the decline in asset prices. When households are more willing to tolerate consumption fluctuations (the blue line), the middle-aged aren’t so anxious to sell their stocks, and asset prices don’t decline as much.

Then follow either line from left to right, meaning from lower to higher shares of wealth held by the old (and, conversely, higher or lower wealth held by the middle-aged). The richer the middle-aged—the more stocks they own—the more stocks they’ll sell in response to a shock in aggregate output.

Why do middle-aged households have such a big impact? If households aren’t willing to accept variability in consumption, the middle-aged will sell their stocks at fire-sale prices to the young. That drop in stock prices depletes the net worth of the old, who hold the remaining shares of stock. “The larger the share of wealth is in the hands of the middle-aged households relative to the old, the larger is the downward pressure on prices in response to a negative shock,” write the economists, “since the young must buy more extra shares with the same amount of earnings.”

Having developed this understanding of the mechanisms that underlie asset price movements and welfare consequences through a sequence of simple models, the economists move to develop a more detailed model with six age groups. They use it to produce more refined estimates of exactly how large or small were the welfare costs of the Great Recession for different age groups in the United States.

They first calibrate the model to ensure that it can replicate the labor income and wealth profiles seen in U.S. data from 2007. Then they use it to analyze asset price declines in response to a “Great Recession” and the way different generations experience a severe, long-lasting recession in terms of reductions in their income and wealth.

Again, the economists ultimately find that the young suffer less than the old, but in most cases, not even the young are better off starting their working lives during a recession, even though asset prices are low—at a time when “labor income is [lower] but houses are much cheaper,” as Ríos put it.

Now, it’s certainly possible to stack the model’s deck so that the young actually gain from a recession, but “unstacking” by adopting more realistic assumptions—for example, that the young actually do value consumption now, not just in the future—brings about what may seem a more sensible finding: A recession benefits no one to a significant extent. “A model recession is approximately welfare-neutral for households in the 20-29 age group,” write the economists, “but translates into a large welfare loss of around 10 percent of lifetime consumption for households aged 70 and over.” Still, arriving at that conclusion takes several more steps.

Results under two scenarios

Further analysis begins with fine-tuning the model through calibration so that it can closely deliver realistic results—that is, an accurate statistical picture of the U.S. population in 2007 in terms of earnings, net worth and portfolio holdings, as measured by the SCF.

The economists first assume that everyone enters the economy as a 20-year-old and lives for six model periods of 10 years each. They then set figures for risk aversion (or 1/IES), discount factors, labor endowment profiles, a supply of bonds and a profile of portfolio shares allocated to stocks, and, finally, capital’s share of income and a probability picture for productivity shocks over time.

And that’s the simple explanation. Suffice to say, after setting appropriate parameters and calibrating carefully, the economists are able to faithfully reproduce the 2007 U.S. population profile for income, wealth and portfolio allocations in their model.

The next step is to gauge the calibrated model’s response to a large recession, defined as an 8.3 percent fall in output, corresponding to the gap measured between actual and trend GDP per capita (adjusted for inflation) that opened up during the recent 2007-09 recession.

For computational reasons, actually, the economists have to impose a more long-lasting output decline of about 10 years. Future refinements of the model may shorten the recession length, but it’s noteworthy that midway through 2011, the actual U.S. economy remained well below trend. As Heathcote observed in late June, “The actual recession is evolving rather closely to our model. Output fell sharply below trend. While in previous recessions, milder recessions, you tended to see relatively quick recovery, in this one, while the economy is growing again, it’s growing slowly. We’ve been stuck at about 8 ½ percent below trend since the beginning of 2009.”

To see how asset prices change in their model economy and to measure the welfare implications, the economists consider two scenarios. In one, every age group experiences the same proportional drop in income from non-asset sources (labor, Social Security, pensions); in the other, the young suffer a greater relative income decline than the old.

For the latter, instead of assuming that every age group experiences the 8.3 percent average decline in income seen in the economy as a whole, the youngest earners (ages 20-29 years) suffer an 11 percent drop in earnings; the 30-39 age group, −11.9 percent; the 40-49 age group, −8.8 percent; the 50-59 age group, −8.9 percent; and the 60-69 age group, −6.2 percent. Those 70 years and older actually have a slight income increase of 1.6 percent. (These figures on income change for specific age groups were derived from Current Population Survey data, since SCF results for 2010 weren’t available.)

Under both scenarios, the economists consider a range of risk aversion from 1 to 5, corresponding, respectively, to greater and lesser levels of intertemporal elasticity of substitution—that is to say, with more or less willingness to put up with consumption fluctuation—though, again, their benchmark value is 3. They also look at economies in which (a) only stocks are traded, (b) both stocks and bonds are traded, but portfolio allocations are fixed and (c) both stocks and bonds are traded, and allocations can shift in reaction to the recession.

The reporting of analysis and results runs for about 13 pages, but the economists’ key findings can be gleaned from comparison of age group welfare allocations generated by model run-throughs under the two income scenarios: (a) income drops the same proportion for everyone and (b) income drops more for the young. Both are for a model with a fixed portfolio allocation and risk aversion of 3. See Table 2.

The outcome evident under both scenarios is that all age groups suffer losses in economic welfare from a severe recession. But it’s also quite clear that the oldest suffer much more, and the youngest least. If all age groups are assumed to experience the same proportional earnings decline in a recession (−8.3 percent), the youngest have less than a 1 percent decline in welfare, while the oldest undergo a 12 percent decline.

Incorporating the fact that the youngest are most likely to lose their jobs or suffer wage declines nearly doubles their welfare loss (−1.20 percent versus −0.66 percent), and the oldest suffer a slightly diminished blow (−10.7 percent instead of −12.0 percent). Nonetheless, recessions are unambiguously harder on the old.

In fact, if risk aversion is set considerably higher (at 5 instead of 3 as in the benchmark model), meaning that people are less willing to lower consumption in the face of a price rise, and people are allowed to alter portfolio allocations, the youngest can be made even better off—by over 2 percent—because they can buy homes and financial assets at more massive fire-sale prices as older households sell houses, stocks and bonds to smooth consumption. This hypothetical benefit for the youngest comes despite an 11 percent decrease in earnings during the first decade of their economic lives.

Even so, the economists stress that the young would benefit from a recession only under the most exceptional circumstances. “In theory, it’s possible; we discovered some conditions under which it could be advantageous for the young,” said Ríos. “But when we looked at a good representation of the U.S. economy, does it look like it would happen? No, not really. It’s better to be born in an expansion. Recessions are not good for the young.”

Caveats and conclusions

To virtually all of this, of course, there are qualifiers. On the one hand, for instance, the fall in labor income for the young is partly because they work fewer hours, which—for those who happen to enjoy leisure time—can easily be considered a welfare gain. On the other hand, being out of the labor market for a considerable time period can erode job skills and diminish future employability. “If you are unemployed for a few years, there are long-term effects that go beyond the economic recovery,” noted Ríos. “Right,” Krueger added. “What we don’t have yet in our model is the fact that bad outcomes for the young may have longer-run consequences on their earning capacity.”

There are a few other weaknesses in their model, or features yet to be incorporated. “The extent to which the model is capable of replicating actual portfolios is limited,” observed Ríos. The version of the model in which households choose portfolios generates numbers that show the old devoting less of their savings to stocks than they actually do and the young investing more in stocks than reality.

“Empirically observed portfolios do not vary quite enough with age to share risk efficiently across generations,” the economists write. “Older Americans are over-exposed to aggregate risk in the data, relative to what is optimal from the perspective of the model.” So, it might be that this points to flaws in American investment choices, rather than in the economists’ model.

Regardless of remaining work and potential weaknesses, the economists’ analysis provides a clear and intuitive picture. “Overall,” write the economists, “we conclude that … welfare losses increase with age, and the oldest households lose the most from a severe recession. In addition, if the asset price decline is large relative to the fall in output and earnings (as was the case in the Great Recession), then the youngest households continue to benefit from becoming economically active in a recession, despite the sharp decline in labor income they experience.”

The central determinant of what the old could lose and the young might gain is the extent to which asset prices drop, relative to labor earnings declines and slumps in aggregate output. If people have high risk aversion—low elasticity of substitution—the middle-aged will be more anxious to sell off their wealth to maintain their lifestyles. Asset prices will then drop significantly, benefiting the young and hurting the old.

What does all this imply for policy? The economists don’t devote much of their paper to policy discussion. “One thing we could perhaps bring into this analysis is government,” noted Krueger. “We have no fiscal response in our model. It could very well be that policies taken by government will load the younger guys with a lot of debt to be repaid in the future because of government action.”

But the paper does point out that financing a greater share of government spending through debt rather than taxes shifts the burden to the young. And it notes that the large-scale asset purchases by the Federal Reserve, as well as the Troubled Asset Relief Program, both supported asset prices—and therefore were policies that benefited older and wealthier households. “From the perspective of the very asymmetric welfare results documented in this paper,” they write, “a distributional argument can be made in favor of such policies.”

Still, a quantitative exploration of that idea, and other possible elaborations, remains to be done. For now, it’s enough to say that recessions, like many things in life, favor the young over their elders.

{kind=link}

{kind=link}

{kind=link}

{kind=link}