Author

Ann Harrington

Senior Writer

Ever since the financial crisis of 2008, academics and policymakers have been trying to prevent such a catastrophe from happening again. Economists have focused on reducing the probability of public bailouts, which are costly and deeply unpopular with taxpayers. Moreover, by signaling “too big to fail” banks that they won’t bear the full cost of high-risk investments, bailouts encourage even more risk-taking.

The Federal Reserve Bank of Minneapolis has been at the forefront of such preventive efforts,1 including the Ending Too Big to Fail initiative that culminated in the Minneapolis Plan. The Plan’s key element: higher capital requirements. Specifically, the Plan recommends that the biggest U.S. banks (those with assets equal to or greater than $250 billion) be required “to issue common equity equal to 23.5 percent of risk-weighted assets.”

Not surprisingly, the banking industry has been cool to such proposals, which would cut into profit margins. Banks contend that 10 percent capital (a substantial increase over precrisis norms of around 4 percent) should be sufficient. But the Minneapolis Plan cites evidence from international financial crises to show that such levels would do little to reduce the chances of a bailout in the next century.

Now a new staff report from the Minneapolis Fed—using different methods and data—strengthens the case for more capital. “Capital Requirements and Bailouts” (SR 554) by Fabrizio Perri, a monetary adviser at the Minneapolis Fed, and Georgios Stefanidis, a research analyst, uses historical data on major U.S. financial institutions to measure the losses suffered by these institutions during the crisis of 2008 and to assess how higher capital requirements might have helped. Their main conclusion is that losses suffered by these institutions during the crisis were very large and, as a consequence, a modest increase in capital levels would have done little to prevent widespread failures. They argue that raising capital levels to the 20 percent to 30 percent range is necessary to forestall future bailouts in the event of another severe financial crisis.

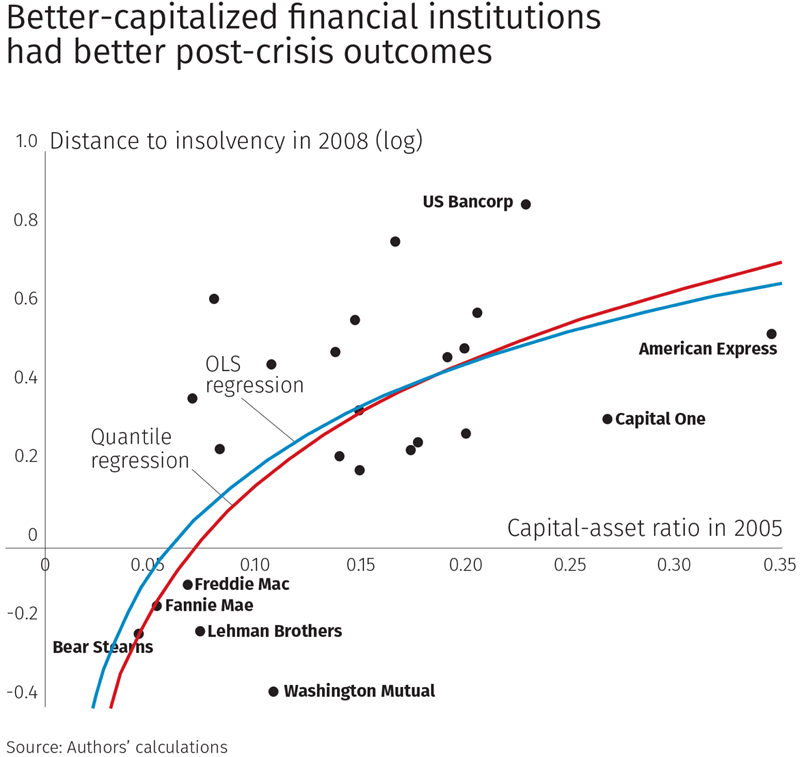

Capital counterfactuals

The economists perform two experiments, with separate sets of data, to measure the losses suffered by the nation’s biggest financial institutions during and after the crisis and to estimate the impact of higher capital requirements. The first exercise uses balance sheet data collected by the Federal Reserve on the 25 largest bank holding companies in the United States from 2001 to 2015. They show that the financial crisis caused a large and persistent drop in returns for these banks, and they then model a counterfactual scenario: What would have happened if the same banks had been subject to higher capital requirements? The second exercise employs stock market data for a somewhat different group of large financial institutions to examine the distance to insolvency during the heat of the financial crisis and assesses how higher capital could have lessened this threat and reduced the risk of taxpayer bailouts.

Both sets of data have an important advantage over the international data used in the Minneapolis Plan: They can show the impact of the financial crisis on individual banks, not just as aggregate losses. Using the balance sheet data, the economists calculate that during the financial crisis, the majority of the country’s biggest banks experienced losses that exceeded more than half their capital. But if those same big banks had been subject to a 30 percent capital requirement, the economists show, the losses would have been far less debilitating. The trade-off, of course, is that banks would be more profitable in bad times but—with less capital to invest—not as profitable in good times.

The balance sheet data have one serious limitation, though. Because the economists wanted to follow companies from 2001 to 2015, they chose companies that were in the sample the entire period. But many big players failed or were acquired during those years. By including only survivors, the authors acknowledge, the method may underestimate losses.

The second exercise has no such downside, as it is based on stock market data during the crisis. It purposely includes companies like AIG and Washington Mutual that were among those hardest hit by the 2008 crisis. Some of these companies went bankrupt; others were acquired or propped up by bailouts. The authors look at two measures: the leverage that each company employs (a ratio of its capital to its assets) and the riskiness of those assets. The more leveraged a company is, and/or the riskier its assets, the less likely it will be able to pay its liabilities.

Using stock market data of each company’s returns from September 2008 to April 2009, the economists show how the combination of low precrisis capital levels and/or risky assets made Bear Stearns, Lehman Brothers and Fannie Mae extremely vulnerable (see chart). They also show how higher capital levels made American Express, Capital One and US Bancorp better positioned to weather the storm.

With more capital, companies are better able to withstand losses, and the need for a bailout dissipates. But how much capital is enough?

The price of stability

Under current regulations, the chance of a bailout in the next 100 years is 67 percent, according to the Minneapolis Plan. Perri and Stefanidis estimate that reducing that probability below 50 percent would require boosting capital levels to nearly 20 percent. Lowering the chances to one in three would require capital levels of about 30 percent. In other words, history shows that the likelihood of another severe financial crisis in the next 100 years is very high. The report argues that if U.S. financial institutions go through a crisis with only marginally higher capital requirements, 2008 will happen all over again. If instead those institutions are required to hold a much higher capital buffer, they are much more likely to withstand the losses from a crisis without triggering systemic financial instability and the need for a public bailout.

The authors acknowledge that they don’t consider the costs of higher capital requirements or the possibility that banks could reduce the riskiness of their investment choices in other ways. Their aim is simply to assess how higher capital requirements could improve the stability of the financial system. Their report may not settle the debate, but it strengthens the case for higher capital requirements.

Endnote

1 Too Big to Fail: The Hazards of Bank Bailouts by Gary H. Stern and Ron J. Feldman was first published in 2004, when the co-authors were, respectively, president and senior vice president of the Federal Reserve Bank of Minneapolis.