Author

Economic Policy Papers are based on policy-oriented research produced by Minneapolis Fed staff and consultants. The papers are an occasional series for a general audience. The views expressed here are those of the authors, not necessarily those of others in the Federal Reserve System.

Executive Summary

The Great Recession was particularly severe and has endured far longer than most recessions. Economists now believe it was caused by a perfect storm of declining home prices, a financial system heavily invested in house-related assets and a shadow banking system highly vulnerable to bank runs or rollover risk. It has lasted longer than most recessions because economically damaged households were unwilling or unable to increase spending, thus perpetuating the recession by a mechanism known as the paradox of thrift. Economists believe the Great Recession wasn’t foreseen because the size and fragility of the shadow banking system had gone unnoticed.

The recession has had an inordinate impact on macroeconomics as a discipline, leading economists to reconsider two largely discarded theories: IS-LM and the paradox of thrift. It has also forced theorists to better understand and incorporate the financial sector into their models, the most promising of which focus on mismatch between the maturity periods of assets and liabilities held by banks.

Introduction

The Great Recession struck individuals, the aggregate economy and the economics profession like an earthquake, and its aftershocks are still being felt. Job losses and housing foreclosures devastated many families. National economies were deeply damaged and have yet to fully recover. And economists—who failed to predict either the crisis or the recession—have been struggling to understand why they didn’t grasp the fragility of the financial system and the duration of the recession.

This essay briefly discusses why the Great Recession is considered both “Great” and a “Recession.” It then turns to the emerging consensus about its cause, its duration and the reasons so few predicted it. Finally, it explores the impact of the Great Recession on how academic economists now think about the economy.

“Great Recession”

The economic downturn the United States suffered from late 2007 to the third quarter of 2009 was particularly damaging. Output, consumption, investment, employment and total hours worked dropped far more during the recent recession than the comparable average figures for all other recessions since 1945. Employment, for example, dropped 6.7 percent during the 2007-09 recession compared with an average of 3.8 percent for postwar recessions. Analogous figures for output: 7.2 percent and 4.4 percent; for consumption: 5.4 percent and 2.1 percent. That higher level of severity across the board is why this recession has earned the adjective “Great.”

By the same token, however, this recession was definitely not the worst U.S. downturn on record. Conditions were far worse during the Great Depression. Employment fell 27 percent from 1929 to 1933 (compared with 6.7 percent from 2007 to 2009), output fell 36 percent (7.2 percent) and consumption fell 23 percent (5.4 percent). For that reason, the recent slump, though severe, is rightly considered a recession rather than a full-bore depression.

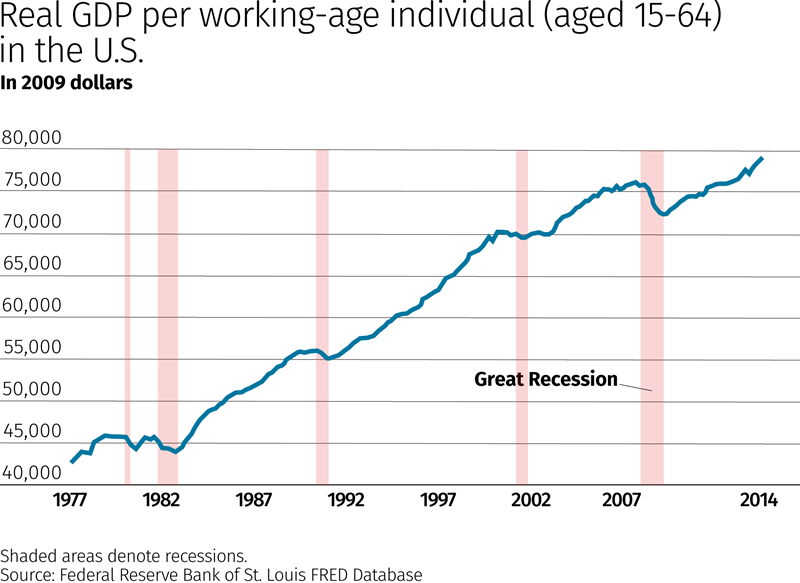

Another reason to consider this recession “Great” is how uncommonly long the economy has been taking to recover. The accompanying figure displays labor productivity (output per working-age person, adjusted for inflation) from 1977 through 2014.1 The vertical pink bars in the figure indicate the starting and ending dates for recessions, as determined by the National Bureau of Economic Research (NBER).

The U.S. economy did not return to the 2007 level of output per capita until a little over five years later, in first quarter 2013.2 The productivity trend lines for the previous four recessions show that the economy usually snaps back more quickly. Even now, the U.S. economy is still about 10 percent below normal (that is, trend growth in 2007).3

What caused the Great Recession?

Conventional wisdom is now converging on a particular narrative about the cause of the Great Recession. In effect, the Great Recession was a “perfect storm” created by the concurrence of three factors.4 Taken by itself, none of these factors would have caused a major recession, but in combination, they were explosive.

The first was the decline in housing prices that began in the summer of 2007. Whether this was the end of a “bubble” or just an ordinary fluctuation does not matter for the narrative. The second factor was that the financial system was heavily invested in housing-related assets, mortgage-backed securities.5 The third factor was that the shadow banking system was invested in housing assets and highly vulnerable to bank runs.6

These three factors are the essential elements in the following narrative about the Great Recession.

The fall in housing prices damaged the assets of the shadow banking system and thereby created the conditions in which a run on the shadow banking system could occur. Alas, a run did occur in the summer of 2007, forcing the shadow banking system to sell its assets at fire sale prices.

This asset decline damaged the whole banking system and hindered its ability to intermediate not just house purchases, but investment more generally. With reduced credit, purchases of houses declined and the fall in house prices was reinforced.

By reducing household wealth, the fall in house prices induced households to cut back on spending. Faced with declining sales, firms pulled back on investment and hiring. All of these factors reinforced each other, sending the economy into the tailspin documented above.

Why has it lasted so long?

The conventional view on why the recession lasted so long is that the events described in the previous paragraph reinforced the desire to save, relative to the desire to invest. If markets worked efficiently, then the interest rate would have fallen to balance the demand and supply of savings, without a significant fall in employment. According to the conventional view, this required that interest rates be substantially negative, something that could not be achieved because the nominal interest rate cannot be much below zero. Because interest rates could not fall enough to clear lending markets, something else had to bring the demand and supply of saving into equality. That something else was the fall in aggregate output and income, which allowed lending markets to clear by reducing saving as people tried to avoid reducing their consumption too much. This is essentially the logic of the “paradox of thrift” analyzed in undergraduate textbooks in macroeconomics.7 Consistent with those textbooks, the fall in output arising from this paradox-of-thrift reasoning could in principle last for a long time.

Why didn’t policymakers or economists see it coming?

The emerging consensus is that no one, neither policymakers nor academic economists, was aware of the third factor underlying the Great Recession, the size and fragility of the shadow banking sector (see, for example, Bernanke 2010).8 The reason is simple. Much of what policymakers and economists know about financial markets comes about as a side effect of regulation, and the shadow banking system existed mostly outside the normal regulatory framework.

Impact on macroeconomics

The Great Recession is having an enormous impact on macroeconomics as a discipline, in two ways. First, it is leading economists to reconsider two theories that had largely been discredited or neglected. Second, it has led the profession to find ways to incorporate the financial sector into macroeconomic theory.

Neglected paradigms

At its heart, the narrative described above characterizes the Great Recession as the response of the economy to a negative shock to the demand for goods all across the board. This is very much in the spirit of the traditional macroeconomic paradigm captured by the famous IS-LM (or Hicks-Hansen) model,9 which places demand shocks like this at the heart of its theory of business cycle fluctuations. Similarly, the paradox-of-thrift argument10 is also expressed naturally in the IS-LM model.

The IS-LM paradigm, together with the paradox of thrift and the notion that a decision by a group of people11 could give rise to a welfare-reducing drop in output, had been largely discredited among professional macroeconomists since the 1980s. But the Great Recession seems impossible to understand without invoking paradox-of-thrift logic and appealing to shocks in aggregate demand. As a consequence, the modern equivalent of the IS-LM model—the New Keynesian model—has returned to center stage.12 (To be fair, the return of the IS-LM model began in the late 1990s, but the Great Recession dramatically accelerated the process.)

The return of the dynamic version of the IS-LM model is revolutionary because that model is closely allied with the view that the economic system can sometimes become dysfunctional, necessitating some form of government intervention. This is a big shift from the dominant view in the macroeconomics profession in the wake of the costly high inflation of the 1970s. Because that inflation was viewed as a failure of policy, many economists in the 1980s were comfortable with models that imply markets work well by themselves and government intervention is typically unproductive.

Accounting for the financial sector

The Great Recession has had a second important effect on the practice of macroeconomics. Before the Great Recession, there was a consensus among professional macroeconomists that dysfunction in the financial sector could safely be ignored by macroeconomic theory. The idea was that what happens on Wall Street stays on Wall Street—that is, it has as little impact on the economy as what happens in Las Vegas casinos. This idea received support from the U.S. experiences in 1987 and the early 2000s, when the economy seemed unfazed by substantial stock market volatility. But the idea that financial markets could be ignored in macroeconomics died with the Great Recession.

Now macroeconomists are actively thinking about the financial system, how it interacts with the broader economy and how it should be regulated. This has necessitated the construction of new models that incorporate finance, and the models that are empirically successful have generally integrated financial factors into a version of the New Keynesian model, for the reasons discussed above. (See, for example, Christiano, Motto and Rostagno 2014.)

Economists have made much progress in this direction, too much to summarize in this brief essay. One particularly notable set of advances is seen in recent research by Mark Gertler, Nobuhiro Kiyotaki and Andrea Prestipino. (See Gertler and Kiyotaki 2015 and Gertler, Kiyotaki and Prestipino 2016.) In their models, banks finance long-term assets with short-term liabilities. This liquidity mismatch between assets and liabilities captures the essential reason that real world financial institutions are vulnerable to runs. As such, the model enables economists to think precisely about the narrative described above (and advocated by Bernanke 2010 and others) about what launched the Great Recession in 2007. Refining models of this kind is essential for understanding the root causes of severe economic downturns and for designing regulatory and other policies that can prevent a recurrence of disasters like the Great Recession.

Endnotes

1 The output and population data were obtained from FRED, the online database maintained by the Federal Reserve Bank of St. Louis. The FRED label for the output measure is GDPC1, and the label for the working-age population is LFWA64TTUSQ647S.

2 The exact amount of time required for per capita output to return to its prerecession peak depends somewhat on the population measure used. If instead the civilian non-institutional population measure (FRED label CNP16OV) were used, then the amount of time would have been longer, roughly seven years. The difference from the results in the figure reflects demographic factors that cause the working-age population to grow less rapidly than the population as a whole.

3 For additional discussion about the trend of U.S. economic output in 2007, see Christiano, Eichenbaum and Trabandt (2015). The 10 percent number in the text was rounded after doing the following calculations. I fit a linear time trend to the natural logarithm of the output measure in the figure, using data from the beginning of the sample to the fourth quarter of 2007, the quarter before the Great Recession began according to the NBER. I extended the trend to the end of the sample. The difference between the trend at the end of the sample and the (log of the) last data point is 0.136, which I rounded to 0.10. The 10 percent number reported in the text is the last number, multiplied by 100.

4 An early, subsequently discarded, view was the so-called labor mismatch hypothesis. It held that the low level of employment was not due to a lack of jobs, but to the lack of workers with the right skills to fill them. Workforce and firms were “mismatched.”

This view lost its appeal as it became apparent just how broad-based the recession was. Employment and hours worked fell in virtually all sectors. The unemployment rate jumped for virtually every type of worker, by level of education and occupation. According to the mismatch hypothesis, wage growth should have been especially high and unemployment low for the highly sought-after types of workers. But jobs were scarce virtually everywhere, for everyone.

Why did employers hire so few workers? Since the early 1970s, the National Federation of Independent Business has surveyed its members to find out what their top problem is. They are asked to select from among 10 possibilities, including taxes, inflation, poor sales and quality of labor. Under the mismatch hypothesis, a large fraction of firms should have selected “quality of labor” as their top problem. They didn’t. Instead, “poor sales” surged beyond all other options as their top problem. Firms were not hiring simply because people were not buying their goods and services.

5 It is an interesting story, beyond the scope of this analysis, how so much money came to be invested in mortgages. Under the conventional view, the source of the money was what Bernanke (2005) called the “savings glut”: Money poured in from high-saving countries in Asia and oil-producing regions. Under what Shin (2012) called the “banking glut,” a lot of that incoming money went to Europe and then came right back to the United States. The European institutions that managed this back-and-forth flow had a strong preference for mortgages.

Evidence in favor of the notion that the large current account deficit reflected an increase in the supply of funds by foreigners is the sharp drop in interest rates since 2000. The evidence that a lot of the extra money went into mortgages is that mortgage rates and lending conditions became particularly loose. For further discussion of this view, see Justiniano, Primiceri and Tambalotti (2015). Evidence consistent with the notion that the U.S. current account deficit played an important role in housing markets can also be seen in the substantial covariation between U.S. housing prices and the current account (see Figure 1.1 in Justiano, Primiceri and Tambalotti 2015).

6 Technically, what happened was a rollover crisis, not a traditional bank run like those familiar from movies and photographs from the Great Depression. For a careful discussion of a rollover crisis, see Gertler and Kiyotaki (2015).

7 The paradox-of-thrift argument described in the text lies at the heart of the analysis of the interest rate lower bound in Eggertsson and Woodford (2003).

8 That shadow banking system was of a similar order of magnitude as the traditional banking system discussed in Geithner (2008).

9 The IS-LM model—often depicted graphically and thought to encapsulate traditional Keynesian theory—describes the relationship between real output (GDP) and nominal interest rates. On a graph with real interest rates on the vertical axis and real GDP on the horizontal, IS-LM is seen as a downward-sloping IS curve (investment and savings, or the market for economic goods) and an upward-sloping LM curve (liquidity preference and money supply). The intersection of these curves indicates an economy’s equilibrium interest rate and GDP.

10 This is the idea that if people feel poor because the economy is not prospering, they’ll cut back on spending; that cutback will, in turn, encourage businesses to retrench on investment and hiring, leading to a self-fulfilling prophecy of economic downturn. The “paradox” is that while thrift at the individual level may be wise, it can have a harmful impact on the broader economy and ultimately on individuals as well. See, for example, “Paradox” Redux in the June 2013 Region.

11 Businesses reducing investment when they experience lower sales, for instance, or households cutting back because they feel poor with the fall in house prices.

12 For another model that may also be able to come to terms with the data on the Great Recession, see Buera and Nicolini (2016).

References

Bernanke, Ben S. 2005. “The Global Saving Glut and the U.S. Current Account Deficit.” Sandridge Lecture. Virginia Association of Economists, April 14.

Bernanke, Ben S. 2010. Statement before the Financial Crisis Inquiry Commission. Washington, D.C., Sept. 2. https://www.federalreserve.gov/newsevents/testimony/bernanke20100902a.pdf

Buera, Francisco and Juan Pablo Nicolini. 2016. “Liquidity Traps and Monetary Policy: Managing a Credit Crunch.” Unpublished manuscript, Federal Reserve Bank of Chicago.

Christiano, Lawrence J., Martin S. Eichenbaum and Mathias Trabandt. 2015. “Understanding the Great Recession.” American Economic Journal: Macroeconomics 7 (1): 110-67.

Christiano, Lawrence J., Roberto Motto and Massimo Rostagno. 2014. “Risk Shocks.” American Economic Review 104 (1): 27-65.

Eggertsson, Gauti, and Michael Woodford. 2003. “The Zero Bound on Interest Rates and Optimal Monetary Policy.” Brookings Papers on Economic Activity 34 (1): 139-235.

Geithner, Timothy F. 2008. “Reducing Systemic Risk in a Dynamic Financial System.” Remarks at The Economic Club of New York. New York City, June 9. https://www.newyorkfed.org/newsevents/speeches/2008/tfg080609.html

Gertler, Mark, and Nobuhiro Kiyotaki. 2015. “Banking, Liquidity, and Bank Runs in an Infinite Horizon Economy.” American Economic Review 105 (7): 2011-43.

Gertler, Mark, Nobuhiro Kiyotaki and Andrea Prestipino. 2016. “Wholesale Banking and Bank Runs in Macroeconomic Modelling of Financial Crises.” Working Paper 21892, National Bureau of Economic Research.

Justiniano, Alejandro, Giorgio Primiceri and Andrea Tambalotti. 2015. “The Effects of the Saving and Banking Glut on the U.S. Economy.” Working Paper 19635, National Bureau of Economic Research.

Shin, Hyun Song. 2011. “Global Banking Glut and Loan Risk Premium.” Draft. 2011 Mundell-Fleming Lecture.