Author

Article Highlights

- Farm incomes fall along with loan repayments

- Household and capital spending down

- Third quarter results point to farmland value decrease

In contrast to recent years when bountiful harvests have offset some of the impact of low commodity prices, heavy precipitation throughout the growing season had a severe impact on crop production in the Ninth District this year. Meanwhile, low crop prices and trade woes didn’t let up on farmers from July through September 2019, according to the Federal Reserve Bank of Minneapolis’ third-quarter (October) agricultural credit conditions survey.

Farm incomes fell relative to the same period a year earlier, according to lenders surveyed. Spending on capital equipment and farm household purchases also decreased. Falling incomes pushed the rate of loan repayment down, while renewals and extensions increased. Land values fell across district states, and interest rates on loans decreased from the previous quarter. The outlook for the fourth quarter is similar, with lenders in the district generally expecting farm incomes to decrease further.

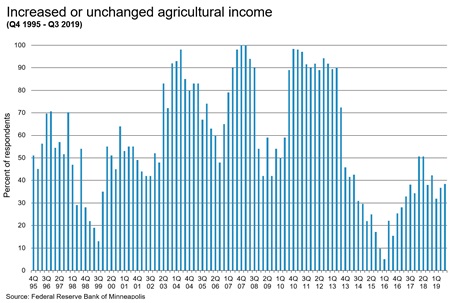

Farm income, household spending, and capital investment

“Crops are poor,” wrote a Minnesota banker. “No market for grain/trade war has had a huge impact on farm income.” A majority of district lenders surveyed apparently agreed with this assessment, as 62 percent reported that farm incomes decreased in the third quarter of 2019 from a year earlier, while most of the remainder reported that incomes were unchanged (see chart). Household spending was down on balance as well, with 36 percent of lenders reporting that it fell, while 5 percent said it increased. Farms also spent less on buildings and equipment—59 percent of lenders reported decreased capital spending, and 4 percent said it increased.

Loan repayments and renewals

Reflecting tighter budgets for farm households, the rate of repayment on agricultural loans fell, while renewals increased. Compared with a year earlier, loan repayment rates decreased for 44 percent of respondents, while 51 percent reported that rates were unchanged. Nearly half of lenders (49 percent) stated that the number of renewals or extensions increased, while most of the remainder said renewal activity was unchanged. Only 3 percent reported decreased renewals.

Demand for loans, required collateral, and interest rates

Demand for loans increased slightly on balance, according to lenders. While a little more than half of respondents indicated that loan demand was unchanged from a year ago, 27 percent noted increased loan demand. Collateral requirements on loans have held steady, according to 83 percent of lenders surveyed, with the balance reporting increases in collateral requirements.

Fixed and variable interest rates for operating, machinery, and real estate loans all decreased from the previous quarter.

Cash rents and land values

Continuing a pattern from the most recent quarterly surveys, the third-quarter results generally pointed to a decrease in farmland values, though the pace of decline quickened relatively. The average value for nonirrigated cropland in the district fell by 4 percent from a year earlier, according to survey respondents. Irrigated land values declined by a half a percent, while ranch- and pastureland decreased 1 percent on average.

Cash rents, by contrast, were a bit more steady. The district average rent for nonirrigated land dropped slightly less than 1 percent. Rents for irrigated land also decreased about a half a percent, while ranchland rents fell about 2 percent.

Changes in land values were generally consistent across the region. South Dakota and Minnesota land prices were in line with the district average, falling by a little more than 4 percent compared with a year earlier. Values in Montana fell at a slower pace of about 3 percent, while North Dakota saw a faster decline, at 6 percent. Wisconsin land prices increased slightly.

Outlook

“The majority of my ag customers will be unable to repay their farm operating lines of credit and their term loans by year-end,” predicted one South Dakota banker on expectations for the final quarter of the year.

The outlook among other respondents was also downbeat. Across the district, 58 percent of lenders expected that farm income will decrease, compared with 7 percent who expected increases. The forecast for capital spending was similar, with 61 percent of respondents expecting decreases, but only 29 percent expecting farm household spending to fall.

A majority of respondents projected demand for loans to remain unchanged in the final three months of 2019, while 29 percent expected increased loan demand. About 45 percent of bankers expected loan repayment rates to decline, and a similar proportion forecast increased renewals and extensions. One in six respondents thought that the amount of required collateral on loans would increase.

Survey results

Percent of respondents who reported decreased levels for the past three months compared with the same period last year:

|

MN |

MT |

ND |

SD |

WI |

Ninth District |

|

| Rate of loan repayments |

54

|

-

|

56 | 42 | 17 | 44 |

| Net farm income |

65

|

60 | 76 | 58 | 17 | 62 |

| Farm household spending |

35

|

20 | 47 | 37 | 17 | 36 |

| Farm capital spending |

54

|

25 | 71 | 72 | 33 | 59 |

| Loan demand |

19

|

20 | 29 | 16 | - | 19 |

Percent of respondents who reported increased levels for the past three months compared with the same period last year:

|

MN |

MT |

ND |

SD |

WI |

Ninth District |

|

| Loan renewals or extensions |

58

|

- | 76 | 28 | 33 | 49 |

| Referrals to other lenders |

12

|

- | - | - | - | 5 |

| Amount of collateral required |

20

|

-

|

- | 32 | 17 | 17 |

| Loan demand |

35

|

40

|

18

|

26

|

17 | 27 |

Percent of respondents who expect decreased levels for the next three months:

|

MN |

MT |

ND |

SD |

WI |

Ninth District |

|

| Rate of loan repayments |

25

|

60

|

56

|

65

|

20

|

45

|

| Net farm income |

40

|

100

|

69

|

74

|

17

|

58

|

| Farm household spending |

20

|

20

|

41

|

37

|

17

|

29

|

| Farm capital spending |

42

|

20

|

59

|

53

|

20

|

46

|

| Loan demand |

25

|

-

|

12

|

18

|

-

|

16

|

Percent of respondents who expect increased levels for the next three months:

|

MN |

MT |

ND |

SD |

WI |

Ninth District |

|

| Loan renewals or extensions |

42

|

20

|

59

|

53

|

20

|

46

|

| Referrals to other lenders |

13

|

20

|

-

|

-

|

-

|

6

|

| Amount of collateral required |

22

|

-

|

-

|

35

|

-

|

17

|

| Loan demand |

21

|

60

|

29

|

35

|

20

|

29

|

Note: The Upper Peninsula of Michigan is not part of the survey.

Endnote

- Agricultural Interest Rates [xlsx]

Joe Mahon is a Minneapolis Fed regional outreach director. Joe’s primary responsibilities involve tracking several sectors of the Ninth District economy, including agriculture, manufacturing, energy, and mining.

{kind=link}