Authors

Article Highlights

- Historical 7(a) loan activity may predict limited Paycheck Protection Program access for Native employers

- Restrictions on lending to gaming enterprises further limit access

- Recent federal actions may bring more relief

Many tribal employers are facing major challenges during the COVID-19 pandemic and there is concern that the current federal fiscal response will not address their unique needs.

A particular concern raised to the Federal Reserve Bank of Minneapolis’ Center for Indian Country Development (CICD) is whether tribal employers have equitable access to the Coronavirus Aid, Relief, and Economic Security Act’s primary small business relief program, the U.S. Small Business Administration’s (SBA’s) Paycheck Protection Program (PPP).

Under the PPP, businesses with fewer than 500 employees are eligible for federally guaranteed loans of up to $10 million that are fully forgivable if 75 percent of the funds are used for payroll; the rest is used for rent, mortgage, or utilities; and the borrowers retain their full-time employees. Businesses can apply through any existing SBA 7(a) lender or through any federally insured depository institution, federally insured credit union, or Farm Credit System institution that is participating. Other regulated lenders will be available to make these loans once they are approved and enrolled in the program.

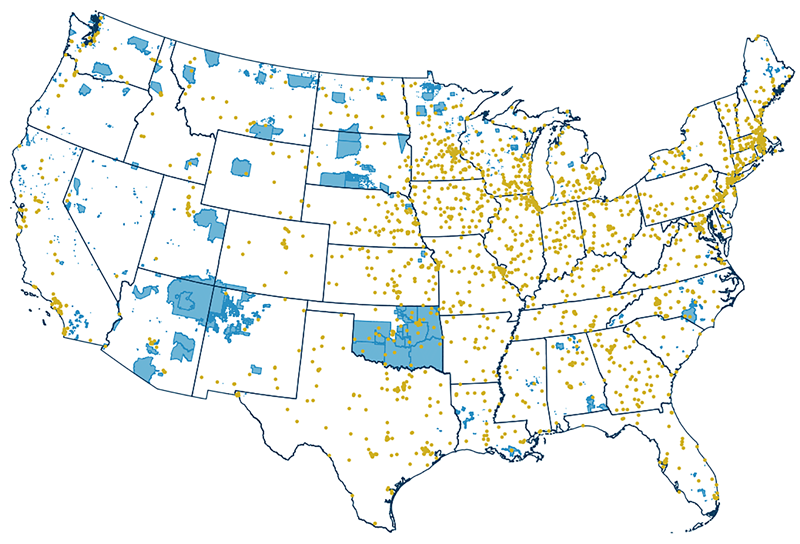

Locations of SBA 7(a) lenders with approved loans made under the 7(a) program, 2015–2019

Given the increase in online lending, we also explored whether the borrowers that leveraged funds under 7(a) were located in tribal areas. CICD analysis suggests this is also not the case. Ideally, we would also analyze where loans made under the PPP are being deployed successfully. CICD is currently pursuing data on the locations of all eligible PPP lenders and looking into acquiring data from the SBA on the locations of PPP loans made.

To investigate Indian Country’s historical access to SBA 7(a) lenders, CICD acquired publicly available SBA data on all 7(a) loans approved from 2015 until the end of 2019. We geocoded the addresses of all the lenders of these loans using OpenCageData.com and then overlaid the locations of these lenders with the geographic boundaries of Indian Country, as depicted in the map above. Over this five-year period, with the exception of lenders in Oklahoma, few 7(a) lenders made 7(a) loans geographically contiguous to or in Indian Country.

To the extent that having an established relationship with a financial institution that makes SBA 7(a) loans is predictive of being able to access funding through the PPP, our analysis indicates that Native American employers may be at a significant disadvantage.

Tribal leaders have raised several other concerns related to equitable access to the PPP. First, most tribal gaming enterprises were not able to access the first round of the PPP because of the SBA's restrictions on gaming enterprises. Second, since the PPP is structured as first-come, first-served, unfunded applications from round one sit at the front of the line, awaiting deployment of round-two funds. As round-two funds are disbursed, tribal gaming enterprises that weren’t eligible to join the queue earlier could be left out. Third, a review of the SBA’s PPP first-round borrower data by industry shows that the industry in which Native American employment is most over-represented—arts, entertainment, and recreation—received only 1.44 percent of the first-round draw-down. And fourth, many PPP lending institutions have reportedly set their own restrictions on access to relief loans, such as limiting applications to current customers—a practice that could put tribal employers at a disadvantage for initiating relationships with PPP lenders.

The initial $349 billion PPP appropriation ran dry in just two weeks. But recent federal actions could bring more relief: Congress recently doubled down on the program, appropriating an additional $310 billion to assist struggling firms; the SBA now allows gaming operations to access the PPP; and a $60 billion carve-out of round two funds will be deployed through community development financial institutions and other smaller lenders—many of which have historically worked closely with underserved communities.* And, reportedly, more lenders are applying to become 7(a)-certified and thus able to make PPP loans.

Increasing the number of PPP lenders—particularly those located near tribal populations—and removing the restriction on gaming enterprises may improve tribal access to the PPP beyond what our findings suggest. As of this writing, it appears that answers about equitable access for Native American employers may be better known in the coming days.

Endnote

* Community development financial institutions (CDFIs) are specialized entities that provide financial products and services, such as small business loans and technical assistance, in markets not fully served by traditional financial institutions. For more information, visit our CDFI Resources web page.

Casey Lozar is a Minneapolis Fed vice president and director of our Center for Indian Country Development, a research and policy institute that works to advance the economic self-determination and prosperity of Native nations and Indigenous communities. Casey is an enrolled member of the Confederated Salish and Kootenai Tribes and he’s based at our Helena, Mont., Branch.