The Federal Reserve Bank of Minneapolis issued a draft Plan to End Too Big to Fail on November 16, 2016. The Plan included a request for comment that contained 11 specific questions for respondents to address. In addition, the Minneapolis Fed has presented the Plan in a number of forums, also with the goal of soliciting comments.

This section of the Final Proposal details the comments we received in the process, our responses to the comments, and the revisions, if any, made to address the comments. We organize the comments by the relevant question they addressed. Note that we summarize the comments we received rather than providing them verbatim, both for brevity and to increase their clarity. The substance of the comments we received has not been changed. We thank all those who took the time to provide comments.

A | Benefit and Cost Analysis of Higher Minimum Equity Requirement

The Minneapolis Plan would increase the minimum equity capital requirement for banks with assets over $250 billion, reflecting an underlying analysis of the benefits and costs of higher capital.

(Q1) Are there improvements that the Federal Reserve Bank of Minneapolis could make to its calculation of the benefits of this aspect of the proposal?

Comment 1.

The Minneapolis Plan overstates the reduction in the chance of a crisis from higher capital because it does not account for the lower capital levels that banks in the rest of the world will have. Lower capital levels in the rest of the world will lead to continued crises outside the United States, which will spill over to the United States.

Response 1.

We do not agree that our estimates overstate the benefits of more capital because we are not accounting for lower capital levels in other countries. Our estimates of the benefits of higher capital derive from calculations that look at the losses from banking crises across many countries. We use these data to calculate the amount of capital a country’s banking system would have needed to avoid the banking crisis that did occur. The empirical data we use reflect data and experiences from countries with different capital standards. In that sense, these data already account for the fact that a crisis in a country with low levels of capital can spill over to a country with higher levels of capital.

In a separate point, the fact that other countries are willing to bail out creditors of TBTF banks in their countries works to the benefit of the United States, as taxpayers in foreign countries pay the costs that could otherwise accrue to a U.S. household or firm. Finally, we think supervisors would naturally review the exposure of banks in the United States to the failure of foreign banks and respond by reducing that exposure if it grew too high.

Comment 2.

William Cline from the Peterson Institute for International Economics argues that the Minneapolis Plan understates the chance of a crisis in banking systems that have low levels of capital. He claims that, as a result, the Minneapolis Plan understates the benefits of adding even small amounts of capital to a banking system that has a low level of capital. In sum, Cline believes that adding what the Minneapolis Plan would see as too little capital to an already low level would have a big effect on reducing the chance of a crisis, in contrast to the findings in the Minneapolis Plan.

Response 2.

Cline’s comment is right in a narrow technical sense, but it does not fundamentally change the results or recommendations of our Plan. As discussed below, Cline is correct that we do not have all the information available to determine precisely the losses avoided for countries with low levels of capital that experience a “not-so-costly” crisis. But adding that information would make our analysis show even larger benefits from the equity levels we recommend. That is, the benefits of adding every additional unit of equity in our analysis would be higher if we addressed Cline’s concern, justifying even higher recommended equity levels for systemic banks.

The Minneapolis Plan calculations rely on an International Monetary Fund (IMF) database of bank crises described in the November 2016 draft Plan. We use those data to estimate the probability that a banking crisis will occur. We do so by simply totaling the number of crises that occur in all countries in the database and dividing by the product of years in the database and countries in the database. The resulting number is the unconditional chance of a crisis.

We also calculate the losses associated with each crisis in the database. To be precise, we make these calculations only for countries that had a crisis and do not consider losses that take place in noncrisis years. With this information, we can estimate the chance that a crisis had a particular cost. That chance is a conditional chance because it depends upon a crisis having occurred.

Next, we use the conditional loss data to determine the number of bailouts that could have been avoided if banks in a country had held a range of equity levels. We do this by assuming that a bailout would not have occurred if banks had held equity capital greater than or equal to particular loss levels. For example, a country that had a banking crisis and losses that amounted to 15 percent of banking system assets would have avoided the bailout if the banking system had held more than 15 percent of equity capital as a percentage of bank assets.

Finally, we combine the chance of having a crisis in the first place with the estimate of the number of crises that could have been avoided for particular levels of equity capital. This gives us joint probabilities, which we called bailout probabilities in the November 2016 draft Plan.

Cline’s comment alludes to the fact that these bailout probabilities are not exactly the same as the chance of a bailout taking place in a country, given a certain level of capital in that country’s banking system. This is true because our calculations do not incorporate information about losses and levels of capital in countries that had such losses but did not have banking crises.

Addressing this omission would require additional data and estimation and would increase the complexity of our analysis. In theory, what we, and Cline, would like is the probability of a bailout conditional on banks’ capital ratios (which we do not have).

However, it turns out that these additional data, and any added complexity from making estimations from these data, are unnecessary. By ignoring the information about what happens when crises do not take place, we assume that the chance of a bailout occurring when the banking industry holds low levels of capital is lower than it otherwise would be. This means that the bailout probabilities we report are a lower bound of what we would compute if we had all the data we wanted. It also means that the effect on our analysis is to reduce the benefit of adding more capital to the banking system. In summary, if we had the additional information, the chance of a bailout occurring at low levels of capital would go up and the benefits of adding more equity to the banking system would also go up. Fixing our calculations as Cline suggests would support even higher levels of equity than those reported in the Plan.

Comment 3.

The Minneapolis Plan does not account for the fact that increasing equity capital at a bank can lead it to take on less risk than it would otherwise. The Plan focuses on the loss-absorbing capacity of equity to reduce the chance of a crisis, but not this feature of reducing risk-taking. As such, the Plan calls for too much equity.

Response 3.

We explained why we do not account for the claim that higher equity capital leads banks to take on less risk on page 17 of the November 2016 draft Plan: “In our analysis, we do not account for the potential that higher equity capital could reduce risk-taking. Instead, we account only for the loss-absorbing capacity of capital that makes failure less likely in the face of any given shock. We take this view because (a) the effect of higher capital on risk-taking of banks is not clear and (b) assuming that capital can only absorb losses rather than change behavior makes our estimates of benefits more conservative.” On the same page we point to analysis finding that higher equity requirements can induce banks to actually take on more risk, not less, suggesting ambiguity in the literature about how more equity influences bank risk-taking. This doubt also supports our position of not including an assumption that higher equity leads to less risk-taking.

(Q2) Are there improvements that the Federal Reserve Bank of Minneapolis could make to its calculation of the costs of this aspect of the proposal?

Comment 4.

The Minneapolis Plan overstates the costs of higher capital. It does so because it views higher equity as more costly than other sources of funding. In contrast, the famous Modigliani-Miller theorem posits that debt and equity have similar costs to a firm. Moreover, recent research on the topic suggests that higher equity requirements do not impose a higher cost than other funding sources.

Response 4.

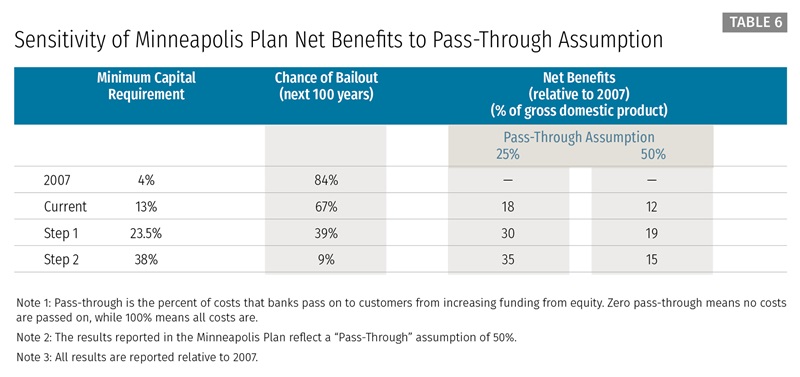

There is a wide range of estimates for the size of the Modigliani-Miller offset. Barth and Miller (2017) find no offset while Clark, Jones, and Malmquist (2017) find an average offset of 85 percent, with the largest banks enjoying a full offset. Other estimates, such as Cline (2015) and Miles, Yang, and Marcheggiano (2012) fall somewhere around a 50 percent offset.

Given that the literature does not narrow down precisely what value to choose, we use a midpoint of the full- and no-Modigliani-Miller effect options by assuming a 50 percent pass-through of the higher funding costs from banks to their customers. Beyond choosing a figure that reflects the uncertainty of the literature, this approach is consistent with our recommendation: Higher equity capital requirements apply to only a small set of covered banks. The vast majority of commercial banks would not have to increase their equity funding and so would not necessarily increase loan rates to the same extent.

We also already provide data in Table 5 in the November 2016 Plan on the effect of altering the Modigliani-Miller offset.

To provide additional information, we have, in the Final Proposal, revised the November 2016 draft Plan to include additional information captured in the table below. The table assumes that only 25 percent of the increase in funding costs implied by higher equity requirements is passed through to bank customers. Assuming a stronger Modigliani-Miller effect essentially cuts the output cost of higher equity in half. That moves the marginal cost curve down, leading to a net benefit-maximizing capital ratio of about 34 percent instead of 22 percent.

Comment 5.

The Minneapolis Plan overstates the costs of a higher equity capital requirement because it does not reflect changes to monetary policy that would occur if the Minneapolis Plan went into effect. In particular, if the Minneapolis Plan reduced bank lending, the Federal Open Market Committee (FOMC) would follow a more expansionary policy, which would offset the effects of higher equity requirements.

Response 5.

The commenter is incorrect. We do account for expected changes in monetary policy in response to the higher equity capital requirement.

Specifically, as indicated on page 33 of the November 2016 draft Plan, we compute the cost of a higher bank equity capital requirement by running simulations of the Board of Governors FRB/US model. In particular, those simulations increase corporate bond spreads to account for the increased cost of funding for banks due to the higher equity requirement. Our simulations start with the FRB/US model in a steady state and run for 10 years. We assume that the change in GDP at the end of the simulation relative to the baseline steady state level is the permanent cost of higher bank equity. The simulation specifically allows for a change in monetary policy. Technically speaking, the simulation allows the federal funds rate to adjust endogenously according to an inertial version of the Taylor rule. Put less technically, there are rules of thumb that link changes in economic conditions to changes in monetary policy. Our simulation follows one of those rules of thumb. In particular, the funds rate declines in response to the increased bond spreads, reducing the costs of higher equity. The funds rate winds up about 25 basis points below its baseline, steady state value.

The approach we took was conservative. For example, we could have adjusted part of the rule of thumb in the model in a relatively standard way (e.g., an intercept adjustment), which would have had the effect of altering the long-run neutral rate of interest to account for the increased spreads associated with higher bank equity. But this approach eliminates any long-run deviation of output from its baseline path, which has the effect of making the cost of additional bank equity zero.

Comment 6.

The Minneapolis Plan does not account for the shift in business away from banks facing the higher equity requirements. Customers of banks facing higher equity requirements will face higher-cost products and services or, if the bank shrinks, they will not be able to obtain the services or products they need. As a result, customers will shift their business to other banks, perhaps foreign banks that have less equity. This shift has several potential outcomes that the Minneapolis Plan does not account for and that reduce the benefits of the Plan. First, the shift will make the new firms from which U.S. businesses and households receive services too big to fail if they were not already, including firms in other countries. Second, bank customers will not receive the benefit of economies of scale from large U.S. banks. Finally, it will reduce the viability of the largest banks in the United States.

Response 6.

The Minneapolis Plan did implicitly consider the potential costs of higher equity requirements and the potential that they could lead to a shift in business away from such firms. At the most general level, the Minneapolis Plan tries to fix a social problem: The enormous costs of the failure of the largest banks in the United States fall onto taxpayers and not the creditors of those banks. Our Plan tries to reduce these social costs and does so by imposing the higher costs of large bank failures back onto bank creditors. The lower potential profits and issues with business models that result are intentional features of the Plan. Put another way, our Plan increases net benefits for society and not for banks and their shareholders.

In terms of the specific comments:

First, as noted in Response 1, the fact that banks in other countries are or may become too big to fail does not reduce the benefits of the Minneapolis Plan. The United States is trying to maximize benefits to its citizens, and the support other countries offer banks does not reduce the benefits of the Minneapolis Plan. Moreover, the Minneapolis Plan anticipates and welcomes the movement of business to smaller domestic banks. This shift reduces the potential spillovers from large bank failures while ensuring that customers receive the services they need.

Second, page 12 of the November 2016 Plan already explains how we take account of potential economies of scale in banking.

Third, as just noted, the Minneapolis Plan will leave a stronger banking system in the United States than the one that exists today. The situation today is one characterized by a small number of huge banks benefiting from government support. Under our Plan, the cost of that support is recognized and leads banks to organize themselves in a manner consistent with the outcome that market forces would otherwise produce.

Finally, we agree that there are costs and benefits to the Minneapolis Plan. We already account for those costs as fully as we can.

Comment 7.

The Minneapolis Plan overstates its benefits by choosing the highest cost of a crisis from the estimates produced by the Basel Committee on Banking Supervision (BCBS). The “middle” estimate of the cost of a crisis, which is 63 percent of GDP, is more plausible than the “high” estimate we use, which is 158 percent of GDP. The higher figure is particularly suspect given that the United States is unlikely, the commenter argues, to experience the more expensive crisis that other countries faced.

Response 7.

We disagree. On pages 23 and 33 of the November 2016 draft Plan, we explain how we chose the cost of a crisis from the prior analysis by the BCBS (2010). The cost of a crisis is the drop in output relative to the precrisis trend and can be temporary or permanent. We think the most appropriate way to measure this cost is by assuming a permanent drop in GDP from the precrisis path, particularly in light of the global financial crisis. Indeed, the U.S. experience justifies this approach. Since the 2007 crisis, real GDP at the end of 2016 was at least 10 percent below a trend estimated through 2007.

The BCBS reviews the literature on the cost of a crisis and finds that 158 percent GDP is a good estimation of the permanent loss. In contrast, the 63 percent cost figure is the median of all studies estimating the cost of a banking crisis, including four of the 13 studies reviewed that argue that the cost is temporary. We do not believe mixing permanent and temporary cost estimates together is a defensible approach.

More specifically, the 63 percent figure comes from a paper (Boyd, Kwak, and Smith 2005) that reports both permanent and temporary cost figures. The permanent loss figure from that same paper was 302 percent, a figure we find technically much more robust than the 63 percent from that specific paper and, in fact, the highest estimate cited by the BCBS long-term economic impact report.

Comment 8.

Analysis from The Clearing House (TCH) finds that the Minneapolis Plan is more costly than the November 2016 draft Plan states. Specifically, TCH argues that the Minneapolis Plan has net costs, not net benefits. (See the TCH blog post of November 18, 2016.)

Response 8.

TCH analysis contains two errors. First, TCH appears to have confused the expected gain from reducing the probability of a crisis with the residual expected costs. In particular, our analysis concludes that the annual probability of a crisis under current regulations is 1.1 percent and would fall to 0.5 percent under Step 1 of the Minneapolis Plan. Using TCH’s preferred cost of a crisis of 63 percent of GDP, the expected loss falls from 63 percent*0.011 = 0.69 percent to 63 percent*0.005 = 0.315 percent for a gain of 0.375 percent of GDP (i.e., the expected loss from a crisis falls by 0.375 percent annually). The TCH post has the 0.315 percent and 0.375 percent figures reversed. Correcting this error reduces the TCH “cost” from $16,000 per person to $13,000.

The second and more serious point relates to TCH’s computation of the present value of net benefits. In sum, if we use the TCH approach, our net benefits are actually much higher than reported in the November 2016 draft Plan. Why? TCH converts the annual costs and benefits from percentages of GDP to present value per capita dollar terms. TCH assumes a 5 percent discount rate and nominal GDP growth of 4 percent. These assumptions imply that an asset that pays $1 today and grows at the same rate as nominal GDP has a present value of $101. The problem with the TCH approach is that it ignores the fact that the loss from crisis is already in present value terms. In particular, the BCBS (2010) study uses a 5 percent discount rate (the same as TCH), but assumes no growth. For example, the 158 percent figure we use for the loss from a crisis is derived by discounting a permanent 7.5 percent of GDP loss at 5 percent. The 63 percent loss value TCH prefers is equivalent to a 3 percent permanent loss. If we were to discount that 3 percent annual loss the way TCH discounts the costs, the present value of the loss from a crisis would be 303 percent of GDP. Translating that into dollar terms results in per capita net benefits of $72,000.

Comment 9.

Several comments focused on our discussion of costs, particularly on Table 1 on page 1 of the November 2016 draft Plan. Specifically, commenters were not clear on the precise definition of costs used in that discussion. For example, was the cost figure an annual loss amount? Was the cost figure a percentage of GDP in the current year?

Response 9.

In response to the comments, we have changed Table 1 and related text to better describe what the cost figures represent. We also respond specifically to several comments we received:

-

The November 2016 draft Plan reports cost figures like 24 percent and 41 percent of GDP. Does that mean your proposal will cost $8 trillion each year given that GDP is $19.5 trillion?

No. The 24 percent figure is the percent difference between (a) what the baseline path of GDP would have been absent Step 1 of our proposal and (b) what GDP will be with Step 1 of our proposal. The 24 percent figure also accounts for the fact that dollars today are worth more than dollars in the future. In other words, it is the “present value” of all the future differences between these two GDP figures.

In terms of 2017 nominal GDP, the 24 percent in Table 1 of the November 2016 draft Plan was about $4.7 trillion.

Alternatively, we could describe the costs as follows: Each year, there is an annual cost to higher capital. We can express that cost as the percent difference between GDP under Step 1 and what GDP would have been, say, under current capital requirements or under the capital requirements as of 2007. In Table 1, that annual difference is about 1.1 percent. We add up these annual differences over time. In fact, we add them up for every year in the future. But we need to account for the fact that a given amount of GDP in the future is not the same as that amount today. People value dollars they get in the future less than dollars they receive today. We apply a “discount” factor to each of these percent differences we calculate annually. And we add these up forever (over an “infinite horizon”). For Step 1 relative to the 2007 regulation, the total of all of this addition equals 24 percent.

-

The cost figures are quite high as reported, correct?

No, they are not. Asking about the magnitude of costs requires one to ask, “Relative to what?” We noted that the present value cost of Step 1 is about $4.5 trillion. But this cost comes with benefits. Specifically, by raising equity requirements, we are reducing the chance of a banking crisis, and there is some chance of a crisis each year. So the benefits of our Plan equal the reduction in the chance of having a crisis in a given year multiplied by the cost of a crisis. That is the amount of money we are saving society by raising equity requirements.

The annual chance of a crisis under Step 1 of our Plan is 0.50 percent compared with 1.79 percent under the 2007 regulations. So the chance of a crisis goes down 1.29 percentage points. The cost of a crisis is 158 percent of GDP (which is the present value of a permanent reduction in GDP due to a crisis of 7.5 percent). The reduced chance of a crisis occurring in a given year multiplied by the cost of a crisis (158 percent times 1.29 percent) equals 2 percent of GDP annually. So Step 1 saves society 2 percent of GDP annually. Adding that annual figure up over time and accounting for the value of current dollars relative to future dollars yields 43 percent of GDP, or $8 trillion. Recall that the cost of Step 1 is $4.5 trillion. So, on net, Step 1 has benefits that are almost twice as high as costs. What about Step 2? Using this same approach, the benefits of the higher equity exceed the costs of the higher equity by roughly $3 trillion.

-

How does your cost estimate compare with how much GDP fell after the 2008 financial crisis?

Real GDP fell 4.2 percent from 2007Q4 to 2009Q2 (peak to trough). In the most current public FRB/US database (released November 8, 2017, https://www.federalreserve.gov/econres/files/data_only_package.zip), potential output rose 3.9 percent over that same period, so relative to “trend,” GDP fell 8 percent. This output seems lost forever. That is, the economy seems to be growing at the same trend as before, but is not growing so quickly as to erase the gap that developed after the crisis. This means that the economy has lost about 8 percent of GDP each year for the rest of time. This figure for the United States is very close to the annual loss figure for a crisis used by the BCBS. The BCBS assumes that an economy loses 7.5 percent of GDP permanently.

Comment 10.

William Cline from the Peterson Institute for International Economics argues that the use of the FRB/US model to estimate the cost of the Minneapolis Plan is flawed. Cline argues for the use of an approach relying on a simpler production function and against allowing for monetary policy to respond.

Response 10.

We disagree.

The approach preferred by Cline estimates the output losses from higher capital requirements directly from a production function. In Cline’s approach, higher capital leads to higher borrowing costs for firms, less investment, a lower capital stock, and less output. However, under his approach, investment is very likely to fall by a larger amount than household saving. If saving and investment are not equal (or do not change by the same amount if they were equal before the change in capital requirements), the amount of output produced will not equal the amount used for consumption or investment. Saving will therefore have to fall when the interest rate falls. So carried to its logical conclusion, Cline’s approach requires lower interest rates, just as we allowed in our model-based approach.

(Q3) Are there improvements that the Federal Reserve Bank of Minneapolis could make to its proposed minimum equity requirement for large banks?

Comment 11.

Capital standards require measures of equity and other potential sources of capital and measures of assets. Two main categories of capital standards are those that “risk-weight” assets and those that do not, which are called risk-weighted asset (RWA) standards and leverage standards, respectively.

The Minneapolis Plan would raise equity requirements for banks with assets over $250 billion relative to the current requirement. However, it raises the leverage ratio proportionately more than it raises the RWA ratio.

Response 11.

We propose a minimum capital ratio of 23.5 percent of risk-weighted assets for covered banks. We use 13 percent as the measure of the current risk-weighted capital ratio. The increase from the current ratio to the proposed one is 81 percent. The comment suggests that we should translate our risk-weighted asset-based target to a leverage ratio by applying that same 81 percent increase to the current minimum leverage ratio requirement.

We do not use that approach; we use a different approach to transform our risk-weighted capital ratio target to a leverage ratio target. Our approach is based on the fundamental fact that the difference between a risk-weighted and a leverage approach to capital standards is the risk-weighting scheme. Those risk weights determine the relationship between total RWAs in the banking system and total unweighted assets. The latter is used in the leverage ratio. We use that relationship to convert our risk-weighted target to a leverage standard. We prefer our approach to the one suggested in the comment because it seems less ad hoc. We discuss the approach we took to translating our recommended RWA ratio to a leverage ratio in Appendix A of the Final Proposal.

We add that our choice of 13 percent as the current RWA ratio target reflects an inherent conservative bias on our part. We could have reasonably chosen a smaller number to represent the current RWA standard. If we had chosen a smaller number to represent the current state, the gap between the current RWA and our proposed RWA requirement would be larger.

Finally, the choice we made of using a simple leverage ratio in our proposal, which has on-balance-sheet assets as its denominator, has important implications for how we translate our RWA target into a leverage ratio. We discuss why we use the simple leverage ratio approach in Comment/Response 12.

Comment 12.

The Minneapolis Plan conducts its benefit and cost analysis on a risk-based capital ratio with CET1 in the numerator and risk-weighted assets in the denominator. It does not conduct that analysis using the simple leverage ratio requirement recommended in the Plan. The Minneapolis Plan should report benefit and cost analysis for the simple leverage ratio as well. Indeed, the leverage ratio has advantages over the risk-based capital ratio. In particular, the risk-based capital ratio may understate the capital needed by banks because it does not capture the true risk of assets. For example, the risk-based capital ratio may treat debt issued by countries as low risk and thus require little equity to absorb losses from that debt when, in fact, the debt is very risky and banks should hold lots of equity against future losses.

Response 12.

We fully support the use of both a minimum risk-based capital ratio and a leverage ratio approach. But, as we note in footnote 5 on page 7 of the November 2016 draft, “We [would] not rely exclusively on a leverage ratio because that approach treats all assets as equally risky and thus can also not accurately set capital relative to the risk the bank takes on.” Thus we already take account of the commenter’s concern about use of the RWA as a minimum standard.

Our cost and benefit analysis would also not change if we applied it to our recommended leverage ratio of 15 percent. This result occurs because of the way we derive the leverage ratio. As generally described in Response 11, the leverage ratio in the Minneapolis Plan is a linear transformation of the RWA target. As such, conducting our cost and benefit analysis on one versus the other would not alter our bottom line findings. Put another way, the capital targets in the Minneapolis Plan are not dependent upon whether we focus on a risk-based capital ratio or a simpler leverage ratio due to our assumption about the relationship between risk-weighted asset and total asset measures. We make this point clearer in Appendix A of the Final Proposal.

Comment 13.

Commenters made two related points regarding the measurement of assets in capital standards and the Minneapolis Plan. These points were motivated by a belief that certain types of capital standards are superior to others. In particular, bank regulators should seek to avoid capital measures that understate the amount of assets a bank holds, as that error will overstate their capital ratio because the measure of assets is the denominator of the capital standard (e.g., the capital standard is a measure of equity divided by a measure of bank assets).

First, some commenters argued that generally accepted accounting principles (GAAP) in the United States understate the assets of banks because that approach does not sufficiently account for the derivative exposures of banks. They argue that the international financial reporting standards (IFRS) do a better job of measuring the complete exposure to banks from derivatives. These commenters asked if the Minneapolis Plan used GAAP or IFRS measures of assets and to explain why we did not use IFRS if that was the case.

Second, some commenters argued that we should use measures of the leverage ratio that, akin to the IFRS point above, have a broad measure of total assets. For example, the so-called supplemental leverage ratio uses a broader measure of assets or exposures relative to more simple measures of the leverage ratio that the Minneapolis Plan uses.

Response 13.

We respond to the two-part comment separately.

First, we are not aware of a data source containing the IFRS data needed to carry out our calculations. At best, we could have tried to make use of average relationships between IFRS and other data to transform our calculations into IFRS terms. But this type of adjustment would not change our results.

We did use a simple measure of the leverage ratio. We did not use a measure of the leverage ratio with a broader measure of assets when we converted our risk-weighted figure to a leverage figure for four reasons.

- There is no one single “correct” leverage ratio. There are multiple measures that are all legitimate. Throughout our analysis, we used the basic approach when we had multiple, reasonable options. We used that approach in this case as well.

- Many important uses of capital measures continue to use the simple leverage figure. For example, we believe the “stress test” run by the Federal Reserve System is a particularly important supervisory exercise for the most systemically important banks. The stress test continues to use a simple leverage ratio measure, among others, in determining the post stress capital position of banks.

- Third, the broad measures of leverage allow for certain nonequity forms of capital to count in the numerator of the ratio. We oppose such inclusion.

- Fourth, the data to convert our risk-weighted target to a leverage target using the broad measure of assets were not available for inclusion in the November 2016 draft Plan.

The data are now available to allow for conversion of the risk-weighted target into a leverage measure using the broad measures of assets. For the sake of transparency, we calculated how our risk-weighted recommendation would translate into a leverage ratio using the broad measure of assets. The 23.5 percent risk-weighted target would translate into a 13 percent leverage ratio using the broad measure of assets. Recall that transformation goes from 23.5 percent to 15 percent when we use a simple leverage ratio approach.

All that said, we are open to using a leverage ratio with a broader measure of assets or the IFRS accounting approach once our Plan is adopted.

Comment 14.

The Minneapolis Plan is silent on the continued use of “stress testing” for the largest banks in its proposal. If the Plan envisions dropping stress testing, explain why.

Response 14.

The November 2016 draft Plan, on page 13, notes, “Our proposal almost always builds on the current reform effort, which we think could make banks more resilient to a shock that hits a single firm during good times. We only seek to modify the minimum capital requirements and long-term debt/TLAC proposal for covered banks.” To be even more explicit, we support the continued use of stress testing for the largest banks. We also believe many of the proposals from former Governor Daniel Tarullo (2016, 2017a) on reforming the stress test are worthy of further study.

Comment 15.

A strength of analysis used by the Bank for International Settlements (BIS)—which includes work by the Basel Committee on Banking Supervision (BCBS), the Financial Stability Board (FSB), and the Macroeconomic Assessment Group (MAG)—is the use of multiple modeling approaches to determine what constitutes the appropriate minimum capital requirement. The Minneapolis Plan seems to rely on just one method, which makes its results less robust and compelling.

Response 15.

Page 21 of the November 2016 draft Plan highlights analysis using different approaches than our own that nonetheless come to similar conclusions. Additional analysis since the release of the November 2016 draft Plan further supports our suggested minimum equity levels. We highlight that analysis here:

-

Passmore and von Hafften (2017) find that the most systemically important banks should face an extra capital surcharge of between roughly 7 percentage points and 14 percentage points on top of their current minimum levels of capital. This surcharge, at its upper ends, would bring capital to a level at or above the proposed minimum of the Minneapolis Plan.

-

Firestone, Lorenc, and Ranish (2017, p. 1) conclude that “optimal bank capital levels in the United States range from just over 13 percent to over 26 percent,” with the higher range meeting or exceeding the Minneapolis Plan’s proposed minimum level.

-

Egan, Hortacsu, and Matvos (2017, p. 170) report, “Our results suggest that capital requirements below 18 percent allow for equilibria with substantial probabilities of bank default and large welfare losses.” We find the analysis in Egan, Hortacsu, and Matvos (2017, pp. 204-06) to strongly support a capital requirement of right around 23 percent (as found in the Minneapolis Plan) and to potentially support a much higher level (e.g., around 39 percent) consistent with Step 2 of the Plan.

-

Schnabl (2017, p. 44) reviews a wide range of analysis of minimum capital requirements and summarizes that “the required thresholds vary greatly across proposals with recommended capital ratios ranging from 9% to 30%. It is clear that all recommendations come with a number of assumptions on the economic magnitude of the costs and benefits of bank capital. Even though there is no unanimous consensus on the recommended level, none of the proposals recommends a number clearly below 10%, and most proposals recommend a number significantly above 10%. A prudent regulator may prefer a threshold that puts more weight on some of the higher estimates.”

-

Barth and Miller (2017) find that increasing the minimum leverage ratio requirement to 15 percent—which matches our recommendation—passes a benefit and cost test.

-

Perri and Stefanidis (2017, p. 3) find, “Quantitatively, however, to achieve a sizeable reduction in the probability of bailout, capital requirements should be increased significantly, in the 20% to 30% range.” They find that these results support the recommendation of the Minneapolis Plan but use a completely different methodology to obtain that result.

Comment 16.

The authors of the Minneapolis Plan could improve it by recommending improvements to Title I and Title II of the Dodd-Frank Act, which concern recovery and resolution planning. In a related point, some commenters asked how resolution would work under the Minneapolis Plan for the largest banks, assuming that even the higher levels of equity are insufficient to prevent failure.

Response 16.

The November 2016 draft Plan articulates a clear view on Title I and II on pages 13 and 14. We note support for efforts taken under these titles and view them as complements to our Plan. We believe authorities should try to use these tools to perform a resolution of a large bank if necessary. We also heard from experts during the production of the Minneapolis Plan calling for a so-called Chapter 14 approach to modifying the bankruptcy code that would facilitate large bank resolution. We would be open to such efforts to improve resolution, although it is not yet clear if Chapter 14 is superior to the Title I and II approaches. In general, we think improved resolution will help address the failure of a single large bank. We do not see improved resolution as able to address more systemic weakness in the financial system. In any case, we note that a resolution regime would not likely prevent the need for government support for bank creditors in the case that losses were larger than the equity requirements we call for.

Comment 17.

The Minneapolis Plan makes no explicit mention of market discipline as a means to end TBTF. Replacing regulator discretion with market discipline is necessary.

Response 17.

We agree. But creditors of banks must believe they will suffer losses in the event of a bank failure in order for market discipline to replace regulator discretion. The question is, therefore, how to convince bank creditors that they are truly at risk of loss. The simplest answer is to focus on creditors on whom the U.S. government has historically been willing to impose losses. Equity holders are that group of bank creditors. For that reason, the Minneapolis Plan focuses on common equity as the most robust form of capital for absorbing losses. Under current proposals, long-term debt counts toward measures of total loss-absorbing capacity (TLAC). We do not believe long-term debt will actually absorb losses in a time of market stress, particularly since it has not done so in the past.

Comment 18.

The Minneapolis Plan focuses on bank holding company size rather than banking activity. Banking activity leads the government to support banking firms in times of distress rather than bank size per se.

Response 18.

The Minneapolis Plan accounts for both size of bank and bank activities. Specifically, the treatment that banks face under the Minneapolis Plan varies by two factors: asset size and systemic risk. Banks that are larger and more systemically important face higher capital charges under the Minneapolis Plan. An important measure of systemic importance is the particular activities that the firm engages in. Under the Minneapolis Plan, the Treasury Secretary will have to certify when banks are not systemically important. The Secretary must review the systemic risk of covered banks, but can identify banks that would otherwise be “not covered” as systemically important with the need to face higher equity capital requirements.

Comment 19.

Addressing TBTF requires the government to set equity requirements at the bank level, not at the bank holding company level as the Minneapolis Plan does.

Response 19.

We disagree. The Minneapolis Plan sets equity requirements at the holding company level for two reasons. First, the government provided support in the last crisis at the holding company level for some firms. Second, issuing increased equity at the banking subsidiary may not adequately protect the bank from losses that threaten the parent company. These losses can arise from any part of the organization.

Comment 20.

Equity requirements should be based on the liabilities of banks, not on the assets.

Response 20.

The government can express equity requirements as a ratio with many options for what is used as the denominator. Our analysis, like all others we are aware of, uses a measure of assets as the denominator. Governments may use assets as the denominator because the losses that equity absorbs come from these assets. Moreover, the underlying data on losses and capital we use for our calculation express capital with assets in the denominator. We agree that certain liabilities pose risk to banks to the degree to which their holders can run. We believe higher equity levels make running less likely, but the thrust of our Plan is to use equity to absorb losses.

Comment 21.

The Minneapolis Plan has an equity requirement that does not vary over time with, for example, the riskiness of the financial system. This limitation of the Minneapolis Plan, some commenters noted, prevents the Minneapolis Plan from operating in a countercyclical fashion.

Response 21.

The November 2016 draft Plan, on page 7, notes that the equity capital requirement under the Plan does not vary by bank or over time. We justify that approach, noting that “we prefer a less-complex capital regime.” We still believe the benefits of simplicity outweigh the benefits of varying the requirement by bank or over time.

Comment 22.

The Minneapolis Plan recommends that equity absorb potential large losses. It would be more efficient and effective to allow banks to tap into reinsurance-type markets or arrangements to shift large losses from the bank to other parties.

Response 22.

The Minneapolis Plan uses equity to absorb losses because there is a strong record of equity playing that role, and it is simple. Creating a contingent approach to absorbing losses for the largest and most systemically important banks does not have the benefits of requiring more equity and adds the drawback of complexity. Contingency approaches are complicated, which means they have a lower chance of working in a crisis.

Comment 23.

The Minneapolis Plan should allow some banks that have assets greater than $250 billion to not face the higher 23.5 percent equity requirement. Some of these banks may pose less risk than others, for example. More generally, some commenters argued that the $250 billion threshold was set too low.

Response 23.

The Minneapolis Plan chose the $250 billion threshold because that figure, per footnote 2 on page 1 of the Plan, is “consistent with an important definition of systemically important banks.” We believe that all systemically important banks should face the higher equity requirement so that the failure of one such bank does not endanger the others. We agree that no threshold for this purpose is perfect, but we believe this one is reasonable.

Comment 24.

The Minneapolis Plan does not use any of the various forms of contingent capital that have been proposed. The Plan would be more effective if such forms of capital were used. Such capital is lower cost and is loss-absorbing.

Response 24.

Pages 10 and 11 of the November 2016 draft Plan explain why we believe common equity is superior to contingent capital. In short, we do not think contingent capital will prove loss-absorbing when it needs to be. Recent evidence from Europe supports this belief. Bailouts of three banks by the Italian government and the European Union in June of 2017 highlight the issue. Minneapolis Fed President Neel Kashkari (2017) argued that these bailouts are a “reminder that only equity can be counted on to protect taxpayers.”

Comment 25.

Analysis conducted under the auspices of the BIS finds that a lower level of equity, relative to the one proposed in the Minneapolis Plan, would prove sufficient to guard against banking crises. The BIS analysis is superior.

Response 25.

Pages 20 and 21 of the November 2016 draft explain why the Minneapolis Plan calculations differ from those conducted by the BCBS/BIS/FSB/MAG. We use a different approach requiring fewer assumptions, which we believe is superior to the approach of the BCBS/BIS/FSB/MAG. Our results are also consistent with the level of loss-absorbing capacity that the Federal Reserve argued large banks should have.

Comment 26.

The Minneapolis Plan should show “confidence intervals” for its calculations.

Response 26.

Our analysis does not lend itself to the calculation of confidence intervals. Instead, and to meet the same objective, we show the results of sensitivity analysis. We also note the uncertainty of our analysis in footnote 4 on page 5 of the November 2016 draft Plan.

Comment 27.

The Minneapolis Plan increases the amount of equity capital that the largest and most systemically important banks must issue. To facilitate the raising of this equity, the Minneapolis Plan should offer recommendations that allow investors to put equity into a bank but not face the burden of becoming a bank holding company.

Response 27.

It is not clear that any change in policy is required to address the concern of the commenter. The analysis to determine if an investor must become a bank holding company is complex and multifaceted, and we do not attempt to capture it fully in this response. But as a general rule, the Federal Reserve will require an investor that owns around 5 percent or more of a bank to be a bank holding company. However, the Federal Reserve has allowed corporate investors who pledge, through a series of commitments, to remain passive owners to control up to 25 percent of a bank and not become a bank holding company.

B | Benefit and Cost Analysis of a “Systemic Risk Capital Charge”

The proposal would create a systemic risk capital charge for all firms that the Treasury Secretary fails to certify as no longer systemically important.

(Q4) Are there improvements that the Federal Reserve Bank of Minneapolis could make to its calculation of the benefits of this aspect of the proposal?

No comments were received for this question.

(Q5) Are there improvements that the Federal Reserve Bank of Minneapolis could make to its calculation of the costs of this aspect of the proposal?

Comment 28.

Several commenters argued, in varying ways, that the Minneapolis Plan still allows a material chance of a bailout due to the “herding” of banks that do not face higher equity requirements under the Plan. The concern is that these smaller and less systemically risky banks will take on the same types of risks and thus tend to fail at the same time. The combined damage caused by multiple failures will result in bailouts similar to those that would occur if a larger bank fails. These commenters thus concluded that the Minneapolis Plan does not really end government support in response to a crisis.

Response 28.

We believe comments on the potential herding of banks without higher equity requirements have some merit, but are greatly overstated in terms of practical effect. As noted on page 12 of the November 2016 draft Plan, it seems likely that banks will continue to use a variety of business models and take on risks that are not highly correlated in the future. Institutions that break themselves up as a result of our Plan are likely to have less-correlated business models. In addition, the costs of having many smaller banks fail, such as during the savings and loan crisis of the 1980s and 1990s, are material but not nearly as large as those of the financial crisis of 2007-08.

(Q6) Are there improvements that the Federal Reserve Bank of Minneapolis could make to its proposal calling on the Treasury Secretary to certify that firms are no longer systemically important?

Comment 29.

Several commenters argued that the Treasury Secretary would not be able to effectively carry out the Minneapolis Plan recommendation that it certify banks as no longer systemically important. In particular, these commenters thought the Treasury Secretary would not have staff with sufficient expertise to carry out the task and would not have access to data and other key inputs to complete the task effectively.

Response 29.

We disagree with the claim that the Treasury Secretary has insufficient resources to certify firms as no longer systemically important. As we argue on page 25 of the November 2016 draft Plan, “The Treasury can take advantage of the full range of data collection and analysis across the federal government to help it identify and respond to systemic risk and financial instability.” We are also confident that the administration would request whatever additional support needed for the Treasury Secretary to carry out this task. It is worth noting that the Treasury Secretary already plays a key role under the Dodd-Frank Act in systemic risk identification and response (e.g., chairing the Financial Stability Oversight Committee).

Comment 30.

The Minneapolis Plan does not give the Treasury Secretary sufficient guidance for certifying firms as no longer systemically important.

Response 30.

The Minneapolis Plan directs the Treasury Secretary to give detailed guidance for determining the degree of systemic risk posed by a bank. Specifically, on page 25 of the November 2016 draft Plan, we note that “the Treasury Secretary would not start with a blank slate. There is a set of metrics and measurements that bank supervisors, including the Board of Governors, use to assess the systemic risk posed by banks. They do so in the context of applying a so-called SIFI [systemically important financial institution] surcharge to GSIBs [globally systemically important banks]. We would call on the Treasury to look to this measurement approach used by other regulators in making its certification that a bank does not pose systemic risk. Of course, this need not be the only methodology, but it could contribute to its assessment.”

Comment 31.

The Minneapolis Plan does not account for the marginal costs and benefits of the systemic risk charge in its recommendations.

Response 31.

Pages 24 and 25 of the 2016 draft Plan provide the exact type of analysis on marginal benefits and costs the commenter calls for.

(Q7) Are there alternative frameworks the Federal Reserve Bank of Minneapolis could use in reducing systemic risk of large financial firms?

Comment 32.

The Minneapolis Plan seeks to reduce/eliminate TBTF by making it less likely that the most systemically important banks fail. This approach is inferior to one that focuses on reducing the underlying cause of the risk-taking that leads banks to fail. The roots of such risk-taking are contractual incentives for bank employees and leadership to take on too much risk and weak corporate governance that does not prevent such excessive risk-taking.

Response 32.

We agree that the Minneapolis Plan focuses on limiting the damage from a shock to the financial system rather than trying to eliminate those shocks from occurring in the first place. We are not aware of evidence supporting the notion that governments can eliminate shocks to the financial system. These shocks have come from different sources over time, including damage to the infrastructure supporting banks, consumer loan concentrations, commercial loan concentrations, trading related assets, exposures to foreign banks, and many others.

The comment also suggests that there is a clear understanding that a few underlying factors cause shocks to the financial system. We fundamentally disagree. The Federal Reserve’s post-financial-crisis approach to monitoring threats to financial stability takes a similar strategy by focusing on factors that can spread instability rather than trying to identify the source of shocks to the financial system. Moreover, the notion that simple changes to corporate governance and contractual arrangements used by financial firms will bring an end to banking crises seems optimistic. We note that such banking crises have been a feature of financial systems across time and countries. Yet contractual arrangements and corporate governance have varied across time and place.

Comment 33.

The Minneapolis Plan identifies TBTF banks based on their size. Yet other factors besides size make them systemically risky. The Plan should account for many factors beyond size in determining which banks are TBTF.

Response 33.

The Minneapolis Plan does not simply rely on size. The Plan requires the Treasury Secretary to determine if a TBTF bank no longer poses systemic risk. This assessment should review a number of attributes of the bank beyond size.

Comment 34.

The Minneapolis Plan assumes that the presence of large and potentially systemically risky banks will lead to banking crises and financial instability. But Canada has a banking system dominated by a small number of very large banks and has avoided some of the costs of financial crises that the United States has faced. This suggests that the United States could maintain its current system of large banks without the threat of a banking crisis that the Minneapolis Plan posits.

Response 34.

Recent analysis of the financial crisis experience of Canada and the United States points to long-standing differences in the financial systems of the two countries to explain why Canada did not have a banking crisis when the United States did. (See Bordo, Redish, and Rockoff 2011 and Haltom 2013.) This analysis views differing outcomes between the two countries in 2007, for example, as deriving from decisions and factors from the early 19th century. This long-term view does not suggest that the United States should accept a few systemically important firms dominating the banking system because Canada ended up with such a system.

This analysis of the Canadian banking system also argues that its composition of highly concentrated banks comes with the cost of oligopoly pricing. (See Boone and Johnson 2010.) Finally, some analysts note that Canada has a very large government safety net for financial assets and institutions.

Comment 35.

It is unclear if the discount window will continue to play its current role under the Plan. In particular, does the Minneapolis Plan view the provision of liquidity from the discount window as a form of bailout that should not continue?

Response 35.

The Minneapolis Plan envisions the discount window playing the role it does today. The Plan seeks to avoid the provision of equity/capital to banks, not liquidity to otherwise solvent institutions.

C | Setting a Shadow Banking Tax

The proposal would levy a tax on shadow banks.

(Q8) Are there improvements that the Federal Reserve Bank of Minneapolis could make to setting a tax on shadow banks within the framework set forth in the proposal?

Comment 36.

The shadow banking tax proposed by the Minneapolis Plan does not have supporting benefit and cost analysis. As such, it is not clear if this proposal represents sound policy.

Response 36.

The cost and benefit analysis we conducted for banks is embedded in our shadow banking tax proposal. First, consider the cost of our proposal. The purpose of the shadow banking tax is to prevent intermediation activities from moving out of the regulated banking sector into the generally unregulated shadow banking sector after the higher equity requirement of Step 1 is imposed. As a result, the tax would raise the cost of funds for shadow banks, increasing the rates they would charge their borrowers, analogous to what would happen in the regulated sector. Our cost calculations are based on the higher cost of borrowing for lenders caused by higher equity requirements. The analysis does not distinguish the firm, bank or nonbank, making the higher-cost loan. So our calculations of the cost of equity already include the costs imposed by the shadow banking tax.

As for the benefits, we have very little data describing the balance sheets of the firms in the shadow banking sector. We have implicitly assumed that by limiting the growth of the shadow banking sector with the tax, we have prevented risk from moving from the regulated sector to the shadow sector. Thus, the benefits from the tax should be similar to the benefits from the higher equity requirement. We now make these points explicit in the revised Minneapolis Plan.

Comment 37.

Imposition of the shadow banking tax will alter the behavior of shadow banks. In particular, it will lead them to increase their leverage through activities that do not face the tax. The tax appears to be set on simple measures of leverage. In response, shadow banks will take on leverage that is hard to detect, such as through derivative transactions. Thus, leverage for shadow banks could grow despite the tax.

Response 37.

We agree, per the comment, that shadow banks will seek to evade the tax just as many firms and households engage in activity to reduce their tax burden. We believe the government should modify the administration and definitions associated with the tax over time in response to such behavior. We have modified the text to make that point clear.

Comment 38.

Shadow banks could herd to a common risk, perhaps as they seek to avoid the tax. This outcome could lead to the failure of many larger shadow banks at the same time, which would pose systemic risk. Alternatively, the failure of many smaller shadow banks could cause sufficient weakness in the real economy as to necessitate a government bailout.

Response 38.

We do not see the herding of small shadow banks as posing a material risk. These shadow firms would each have assets under $50 billion. Failures of such firms seem unlikely to pose risk to the real economy. Moreover, the tax should discourage leverage, which is a major source of risk in the first place.

Comment 39.

The Minneapolis Plan argues that the shadow banking tax equalizes the funding costs between banks and shadow banks, as those terms are used in the Plan. This assertion is not correct. The shadow banking tax equalizes the incremental cost of each additional unit of equity for banks and shadow banks.

Response 39.

This comment is incorrect. The tax does equalize funding costs by assumption. We assume that returns on equity and debt are the same for banks and shadow banks and that they hold equally risky assets. We set the tax to equalize the funding costs across the two types of firms. We agree that if we were to relax our assumptions about equal riskiness of assets, computing the appropriate tax rate would also involve computing an equivalent capital requirement (i.e., a shadow bank with riskier assets should have a higher fraction of equity financing). We do not have information about the riskiness of shadow bank assets to make these calculations.

Comment 40.

A commenter suggested an alternative method for setting the shadow banking tax. Specifically, the commenter suggested varying the tax with the leverage of the shadow bank, imposing a nonlinear tax schedule to encourage shadow banks to limit debt to 76.5 percent of assets, or computing firm-specific capital requirements and imposing them directly.

Response 40.

We discuss this and other alternative approaches on page 29 of the November 2016 draft Plan. While we agree that the assets of shadow banks are likely to have different risk properties than those held by covered banks, we chose to make several simplifying assumptions that led us to recommend a simple tax on shadow banks. We would be open to consideration of more general tax schedules, but that would require more data on shadow banks than are currently available.

Comment 41.

The Investment Company Institute (ICI), which asked for its comments to be on the record, argued against the imposition of bank-like regulation on mutual funds. The ICI argued that mutual funds do not operate like banks and that their failure does not occur in the same way or have the same implications as bank failure. Finally, the ICI claimed that the tax on mutual funds would harm investors. The full comment can be found here: https://www.ici.org/pdf/30544a.pdf.

Response 41.

We agree that mutual funds are not like banks, and the Minneapolis Plan does not treat the two types of firms the same. Moreover, the tax on shadow banks should be of no concern for firms that do not take on leverage. Mutual funds that do not take on leverage will pay no tax.

(Q9) Are there alternative frameworks the Federal Reserve Bank of Minneapolis could use in setting a tax on shadow banks? What are they? How would a fee be calculated using these alternative frameworks? Why are they superior to the framework used in the proposal?

Comment 42.

It would be superior to set equity requirements for shadow banks at the level needed to achieve the same chance of avoiding a banking crisis as was set for banks.

Response 42.

Page 29 of the November 2016 draft Plan addresses this comment. We note the advantages in theory of setting the same capital requirements across sectors to address TBTF. However we noted the practical limitations, and near impossibility, of implementing this approach. There are too many firms and legal frameworks covered by the “shadow bank” label to allow one common capital requirement approach.

D | Right Sizing Community Bank Supervision and Regulation

The proposal would create a separate and more appropriate supervisory and regulatory regime for

community banks.

(Q10) Are there specific features of such a regime that the current proposal should include but does not?

Comment 43.

Step 4 of the Minneapolis Plan reforming community bank supervision and regulation does not recommend changes to consumer-related regulation or supervision. Yet community banks have identified consumer-focused supervision and regulation as a major source of cost without a simultaneous increase in benefits. The Minneapolis Plan is deficient unless it targets consumer regulation and supervision.

Response 43.

We have revised our Plan to reform community bank supervision and regulation, which we discuss in Comment/Response 44 below. However, we continue to exclude consumer supervision and regulation from the Plan. We argue on page 13 of the November 2016 draft Plan that fixing TBTF is a necessary first step to reducing regulatory burden on community banks: “We think reforms for community banks will not occur when the threat from the banking system to the economy remains large.” This explains why we discuss reforms for community banks in a plan aimed at systemically important banks. But this same rationale would not justify including consumer regulation and supervision in our scope. Put another way, we do not review consumer regulation and supervision because these rules and laws seek an objective—“consumer protection”—not directly linked to the TBTF problem or the solution we offer.

Comment 44.

Several commenters noted that the Minneapolis Plan calls for a separate and more appropriate supervisory and regulatory regime for community banks, but that the Plan provides insufficient detail to evaluate how the Plan would achieve this goal. This makes the Plan less credible. In related comments, several commenters noted that other sources, such as Thomas Hoenig, vice chairman of the Federal Deposit Insurance Corporation, had offered plans to provide improved supervision and regulation for community banks and noted that it was difficult to compare these alternative plans with this aspect of the Minneapolis Plan.

Response 44.

We agree that Step 4 of the Minneapolis Plan calling for reform of the solvency regulation and supervision of community banks would benefit from additional detail. We had hoped to support the recommendations of banking agencies charged with reviewing banking regulations under the Economic Growth and Regulatory Paperwork Reduction Act (EGRPRA). The agencies had suggested that they would offer recommendations to make community bank supervision and regulation more effective. But the recommendations from EGRPRA do not go far enough. Our view is similar to those of other observers, such as the Independent Community Bankers of America (2017a), which argued that the “statutorily required EGRPRA report to Congress ... falls far short of making the substantial impact on regulatory burden that ICBA has advocated in several comment letters and meetings since this EGRPRA review launched nearly three years ago.”

The call for additional reform can also be found in the letter former Federal Reserve Governor Daniel Tarullo (2017b) sent to Congress in conjunction with the EGRPRA report. Tarullo offered two broad conclusions while making the overarching point that a broader review and reform effort than that conducted under EGRPRA was needed. Tarullo argued that

-

“quite different regulatory configurations should apply to banks of different sizes and activities, which pose quite different risks to the financial system. ... There are some core forms of prudential regulation that ought to be conceived of differently for different tiers of banks. Foremost among these are capital requirements.”

-

“examination and supervisory processes can be as much or more costly for these banks as the underlying regulations themselves. ... There is need for a complementary effort to streamline the supervision of community banks by, for example, reducing the number of on-site examinations.”

Finally, there are well-known and more comprehensive community bank regulatory reform recommendations from sources such as Hoenig (2016), the American Bankers Association, and the Independent Community Bankers Association of America (2017b). Policymakers should look to these compilations in formulating policy recommendations.

With these comments as context, we have modified the Minneapolis Plan to include these more specific reforms:

-

We previously called for “simple but appropriate standards for these [community] banks.” We now explicitly call for a shift to a capital regime for banks with less than $10 billion in assets, where the risk-weighting is much less complicated and would largely mirror Basel I. Consistent with the November 2016 draft Plan, we do not support returning to a period where debt-like instruments can count as “capital.”

-

We previously called for a “less-costly and less-complex system of supervision focused on fundamental sources of risk.” We make this recommendation, which applies to solvency-related supervision, more detailed in two ways.

First, we propose a new, more risk-focused framework in which examiners implement supervision. In this framework, the default mode for supervision would be to review only (a) how banks comply with specific laws passed by Congress (and the rules and guidance issued to implement those laws) or (b) operations, policies, or procedures of a bank for which the banking agencies have empirical evidence supporting a correlation with materially weaker bank conditions (i.e., the case where bank operation, policy, or procedure, if ineffective, is associated with worsening of bank conditions). We believe such evidence exists with regard to certain asset concentrations, funding strategies, interest rate risk profiles, and growth patterns, among other variables. We are more skeptical that such evidence exists with regard to a wide range of other activities and requirements that supervisors currently review. We think such a requirement would reduce costs to banks to a substantial degree without making them more risky.

We recognize that there may be cases where supervisors cannot readily carry out the empirical analysis to show a correlation between a bank practice or policy and weaker banking conditions. For example, it may be difficult to gather data demonstrating that weakness in an internal audit program at a bank is correlated with future weakness because such data may not exist. As such, we would allow supervisors to have an exemption process to these two limits in our proposed framework, but would expect supervisors to use it sparingly.

Second, we recommend specific changes that community banks have called for:

-

Moving to a two-year examination cycle for banks that have an overall satisfactory supervisory rating and are well-managed and capitalized.

-

Eliminating the need for appraisals for well-collateralized commercial loans (e.g., with loan-to-value ratios above an appropriate amount identified by the banking regulators) made by community banks headquartered in rural areas. Rural areas appear to have very few appraisers.

-

Allowing all mortgages held in portfolio by community banks to count as “qualified” mortgages under the Dodd-Frank Act.[i]

-

Reducing the call report to items for which the banking agencies can affirmatively show a link to the forecasting of future bank weakness or other clear surveillance benefits.

-

Applying the Federal Reserve’s Small Bank Holding Company statement to noncomplex holding companies with assets of $10 billion or less.

-

Requiring an independent commission to analyze the costs and benefits of the shift to the Current Expected Credit Loss accounting standard and to opine on the net benefits of modifying or eliminating this standard.

We would retain the right of bank supervisors to examine banks sooner than this two-year cycle, require appraisals, and so on, but would shift the default position to these recommendations.

-

On page 13 of the November draft Plan, we called for the “repeal [of] solvency and other noncompliance-related provisions of the Dodd-Frank Act that apply to community banks and that do not have a strong link to their chance of failure.” We now specifically call for exemption from the Volcker rule for community banks and either elimination of new Dodd-Frank data collections under the Home Mortgage Disclosure Act or the Community Reinvestment Act or legal protections for banks that show a good faith effort to comply with the rules, but have errors in reporting.[ii]

We believe these changes will make supervision and regulation more effective by focusing on key risks and more efficient by reducing resources allocated to lower-risk activity. The downside of our approach is the potential that supervisors will have to react quickly to a worsening of conditions at a bank rather than catching it earlier under the current regime. We do not see this concern as particularly relevant because our reforms continue to focus on supervision of high-risk areas such as credit and capital and allow supervisors to accelerate their reviews if needed.

(Q11) Are there specific features of such a regime that the current proposal includes that it should not?

Comment 45.

The Minneapolis Plan calls for the deregulation of community banks. Deregulating community banks is a bad idea because these institutions take on risks that lead to failure or impairment, which have real social and economic costs.

Response 45.

The Minneapolis Plan does not call for deregulation in either the November 2016 draft Plan or the Final Proposal. As discussed on page 13 of the 2016 draft Plan, our proposal for community banks would focus supervision and regulation on activities, such as concentration of assets or rapid growth, linked to bank weakness. We believe there are regulations and supervisory practices that impose costs on community banks but do not generate commensurate benefits. We suggest taking steps to eliminate these net costly regulations or supervisory practices.

Endnotes

[i] We view the qualified mortgage rule to have both solvency and consumer drivers and thus include it in our analysis.

[ii] We view these disclosures as having both transparency and consumer drivers and thus include them in our analysis.

References

Barth, James R., and Stephen Matteo Miller. 2017. Benefits and Costs of a Higher Bank Leverage Ratio. Mercatus Working Paper, George Mason University.

Basel Committee on Banking Supervision. 2010. An Assessment of the Long-Term Economic Impact of Stronger Capital and Liquidity Requirements. August. Online at https://www.bis.org/publ/bcbs173.pdf.

Boone, Peter, and Simon Johnson. 2010. The Canadian Banking Fallacy. Baseline Scenario. Online at https://baselinescenario.com/2010/03/25/the-canadian-banking-fallacy/.

Bordo, Michael D., Angela Redish, and Hugh Rockoff. 2011. Why Didn’t Canada Have a Banking Crisis in 2008 (or in 1930, or 1907, or ...)? Working Paper 17312. National Bureau of Economic Research.

Boyd, John H., Sungkyu Kwak, and Bruce Smith. 2005. The Real Output Losses Associated with Modern Banking Crises. Journal of Money, Credit and Banking 37 (6), 977-99.

Clark, Brian J., Jonathan Jones, and David H. Malmquist. 2017. Leverage and the Cost of Capital for U.S. Banks. Online at https://ssrn.com/abstract=2491278.

Cline, William R. 2015. Testing the Modigliani-Miller Theorem of Capital Structure Irrelevance for Banks. Working Paper 15-8. Peterson Institute for International Economics.

Egan, Mark, Ali Hortaçsu, and Gregor Matvos. 2017. Deposit Competition and Financial Fragility: Evidence from the US Banking Sector. American Economic Review 107 (1), 169-216.

Firestone, Simon, Amy Lorenc, and Ben Ranish. 2017. An Empirical Economic Assessment of the Costs and Benefits of Bank Capital in the US. Finance and Economics Discussion Series 2017-034. Board of Governors of the Federal Reserve System. Online at https://doi.org/10.17016/FEDS.2017.034.

Haltom, Renee. 2013. Why Was Canada Exempt from the Financial Crisis? Econ Focus (Fourth Quarter). Federal Reserve Bank of Richmond.

Hoenig, Thomas M. 2016. A Framework for Regulatory Relief. Remarks to the FDIC Community Banker Conference, Arlington, Va., April 6. Online at https://www.fdic.gov/news/news/speeches/spapr0616b.pdf.

Independent Community Bankers of America (ICBA). 2017a. Banking Agencies Fail in Joint Review of Banking Rules. ICBA News, March 21. Online at https://www.icba.org/go-local/why-go-local/news-media/news-media-2014/2017/03/21/icba-banking-agencies-fail-in-joint-review-of-banking-rules.

Independent Community Bankers of America (ICBA). 2017b. Plan for Prosperity. Online at http://www.icba.org/docs/default-source/icba/advocacy-documents/priorities/icbaplanforprosperity.

Kashkari, Neel. 2017. New Bailouts Prove “Too Big to Fail” Is Alive and Well. Wall Street Journal, July 9.

Miles, David, Jing Yang, and Gilberto Marcheggiano. 2012. Optimal Bank Capital. Economic Journal 123 (567), 1-37.

Passmore, Wayne, and Alexander H. von Hafften. 2017. Are Basel’s Capital Surcharges for Global Systemically Important Banks Too Small? Finance and Economics Discussion Series 2017-021. Board of Governors of the Federal Reserve System. Online at https://doi.org/10.17016/FEDS.2017.021.

Perri, Fabrizio, and Georgios Stefanidis. 2017. Capital Requirements and Bailouts. Staff Report 554. Federal Reserve Bank of Minneapolis.

Schnabl, Philipp. 2017. Bank Capital Regulation and the Off-Ramp. In Regulating Wall Street: CHOICE Act vs. Dodd-Frank. New York University.

Tarullo, Daniel K. 2016. Next Steps in the Evolution of Stress Testing. Speech at the Yale University School of Management Leaders Forum, New Haven, Conn., September 26. Online at https://www.federalreserve.gov/newsevents/speech/tarullo20160926a.htm.

Tarullo, Daniel K. 2017a. Departing Thoughts. Speech at the Woodrow Wilson School, Princeton University, Princeton, N.J. Online at https://www.federalreserve.gov/newsevents/speech/tarullo20170404a.htm.

Tarullo, Daniel K. 2017b. Letters to Committee Chair and Minority Leaders, March 21. Online at https://www.federalreserve.gov/foia/files/crapo-brown-hensarling-waters-letter-20170321.pdf.