- Full event(video)

- Media Q&A(audio)

This speech is also available on Medium

Thank you, Chairman Lundgren, for that warm introduction.1,2 I would also like to thank the Economic Club of New York for inviting me today, and David Wessel, of the Brookings Institution, for joining us to moderate our discussion. Before I begin, I would like to remind everyone that the views I express today are my own, and not necessarily those of the Federal Open Market Committee or the Board of Governors, which sets supervision and regulatory policy for the Federal Reserve System.

In February, I announced that the Federal Reserve Bank of Minneapolis was launching an initiative to develop a plan to end the problem of too big to fail (TBTF) banks, and I committed us to releasing a plan by the end of the year. Today we are fulfilling that commitment.

I believe our initiative demonstrates the strength of the distributed structure of the Federal Reserve System that Congress created more than 100 years ago, which they designed to encourage a diversity of perspectives on important economic issues.

The purpose of my speech is to introduce the Minneapolis Plan to end TBTF. I will give some background on the development of the plan, describe what it accomplishes, walk through the key steps of the plan, and then I look forward to discussing it with David and then with the audience.

This morning, we published two documents: First, a Summary for Policymakers and, second, the Full Proposal of the Minneapolis Plan. Those of you here in the audience have a hard copy of the summary in front of you. Both documents are available on the Minneapolis Fed website.

I come at the TBTF problem from the perspective of a policymaker who was on the front line responding to the 2008 financial crisis. When Congress moved quickly to pass the Dodd-Frank Act (the Act) in 2010, I strongly supported the need for financial reform, but I wanted to see the Act implemented before I drew firm conclusions about whether it solved TBTF.

Over the past six years, my colleagues across the Federal Reserve System have worked diligently under the reform framework Congress established and are fully utilizing the available tools under the Act to address TBTF. While significant progress has been made to strengthen the U.S. financial system, I believe the biggest banks are still TBTF and continue to pose a significant, ongoing risk to our economy.

Our initiative brought together a wide range of experts on financial crises and banking regulation through a series of symposiums in Minneapolis and Washington, D.C. By design, we wanted to hear all views. Some experts argued in favor of the current regulatory framework, while others argued for more transformational approaches. We learned something from everyone who participated, and we are grateful for their willingness to candidly share their ideas.

Expert participants in our symposiums included former policymakers such as former Federal Reserve Chairman Ben Bernanke, Vice Chairman Roger Ferguson, and Governor Randy Kroszner. They included leading academics, such as Anat Admati of Stanford and Simon Johnson of MIT, among many others. They included policy experts from think tanks, such as Adam Posen of the Peterson Institute and Aaron Klein of the Brookings Institution. And they included economists currently working at policymaking institutions, such as Giovanni Dell'Ariccia of the International Monetary Fund (IMF) and Mark Flannery of the Securities and Exchange Commission. At every symposium, we invited the private sector to participate and were pleased to hear from experts across several segments of the financial services industry, including John Bovenzi of Oliver Wyman and Michael Hasenstab of Franklin Templeton. The largest banks, however, refused to participate, for fear their presence would be viewed as an acknowledgement that the TBTF problem still exists. We didn’t allow their parochial objections to impede our work.

Our goal was not only to learn as much as possible from these experts, but also to help educate the public about these important topics, so our symposiums were all open to the press and live-streamed to the public via our website. I thank the members of the press who have covered, and continue to cover, this initiative. Their work is essential to informing the public. All presented materials and videos of all symposiums are available at minneapolisfed.org. And as we have done throughout our process, we continue to seek comments from the public. That is why we are releasing the Minneapolis Plan with a 60-day comment period.

The ultimate goal of our initiative is to equip the public and their elected representatives with the information and analyses they need to assess what progress has been made in ending TBTF, to understand what risks remain, and to give them additional options to enhance the safety of the U.S. financial system.

One of the key messages we repeatedly heard from experts throughout our initiative is the need to understand both costs and benefits when considering potential regulatory reforms. Indeed, as I will show you, an objective assessment of costs and benefits is the foundation on which the Minneapolis Plan is built.

One useful analogy that helps highlight the trade-off of costs and benefits is the risk of terrorism. Intuitively, the public understands that we as a society cannot eliminate all risk of a future terrorist attack. It is simply impossible to make that risk zero. And the public intuitively understands that increased physical safety isn’t free. There are costs associated with hiring additional law enforcement officers, for example, or installing more metal detectors. Since we cannot eliminate all risk, we have to decide how much safety we want and what price we are willing to pay for that safety. The same is true for financial crises. We cannot make the risk zero, and safety isn’t free. Regulations can make the financial system safer, but they come with costs of potentially slower economic growth. Ultimately, the public has to decide how much safety they want in order to protect society from future financial crises and what price they are willing to pay for that safety.

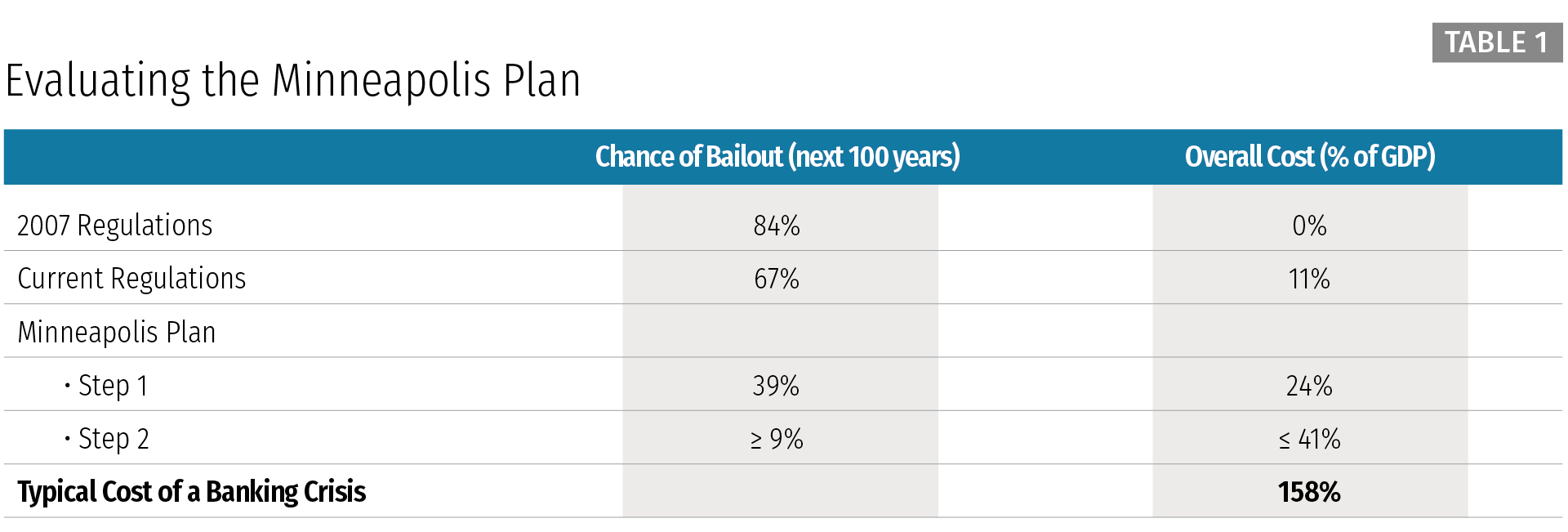

We have developed a framework for assessing safety and costs. The first column says “Chance of a Bailout in the Next 100 Years.” The IMF has compiled a database of financial crises around the world that we use to assess how frequently financial crises have happened in the past and what regulations were in place when those crises happened. Fortunately, financial crises are infrequent events, but that makes them hard to predict, like terrorist events or earthquakes. This IMF database contains the best data available to look at the history of financial crises and make informed estimates about their future likelihood. We look at a 100-year time horizon because the Great Depression took place in the 1930s and the recent financial crisis in 2008, approximately 80 years later. Aiming to prevent financial crises over a 100-year time horizon seems like a reasonable goal, given how devastating crises are when they hit.

On the right side of the table, we list costs. Here we calculate the present value of future costs, using a similar method as do regulators around the world.

We set as a baseline the capital regulations that existed in 2007, before the onset of the recent financial crisis. An examination of the IMF database of crises and the regulations that existed in 2007 implies an 84 percent chance of a crisis in the following 100 years. Obviously, the crisis in fact happened the next year. The database offers a view of how likely crises are to happen, not when exactly they will happen. In terms of costs, we set the 2007 regulations as a baseline, so we assume those costs are zero for comparison purposes.

Next we look at the current capital regulations, which have increased capital requirements relative to 2007. As you can see from the table, the probability of a future financial crisis has been reduced, from 84 percent to 67 percent over the next 100 years. That is a modest improvement in safety at a cost of 11 percent of GDP. Is 11 percent of GDP a lot or a little?

Here we see that the Bank for International Settlements’ consensus estimate for the typical cost of a banking crisis is 158 percent of GDP, which for the U.S. economy equals roughly $28 trillion. This is the present value of the long-term effects of a banking crisis. As we have seen since the recent crisis, the U.S. economy has been growing much more slowly than had been previously expected. These long-term effects are fairly typical for financial crises, which as you can see, are extraordinarily costly for society. Against that enormous cost, 11 percent of GDP seems to me to be a small price to pay for a modest increase in safety.

In contrast, the Minneapolis Plan goes much further to improve safety, admittedly at an increased cost. The Minneapolis Plan has multiple steps.

I will explain what these steps are in a few moments. With Step 1 of the Minneapolis Plan, we reduce the risk of a future financial crisis and bailout from 67 percent under current regulations to 39 percent, a substantial improvement in safety. And as you can see, the additional safety isn’t free. Costs increase to 24 percent of GDP, which is still very small compared with the typical cost of a banking crisis, 158 percent.

Finally, in Step 2 of the Minneapolis Plan, we reduce the risk of a future crisis and bailout to as low as 9 percent. Again, the added safety isn’t free. The total cost is as high as 41 percent of GDP, which is much higher than current regulations, but still much smaller than the cost of a financial crisis. To say it another way, if the Minneapolis Plan prevents one financial crisis, it will have paid for itself multiple times over. These are the trade-offs the public needs to understand in order to assess whether we have done enough to end TBTF or if we should go further. To me, these data make it very clear that we should go much further.

Next I will describe the Minneapolis Plan.

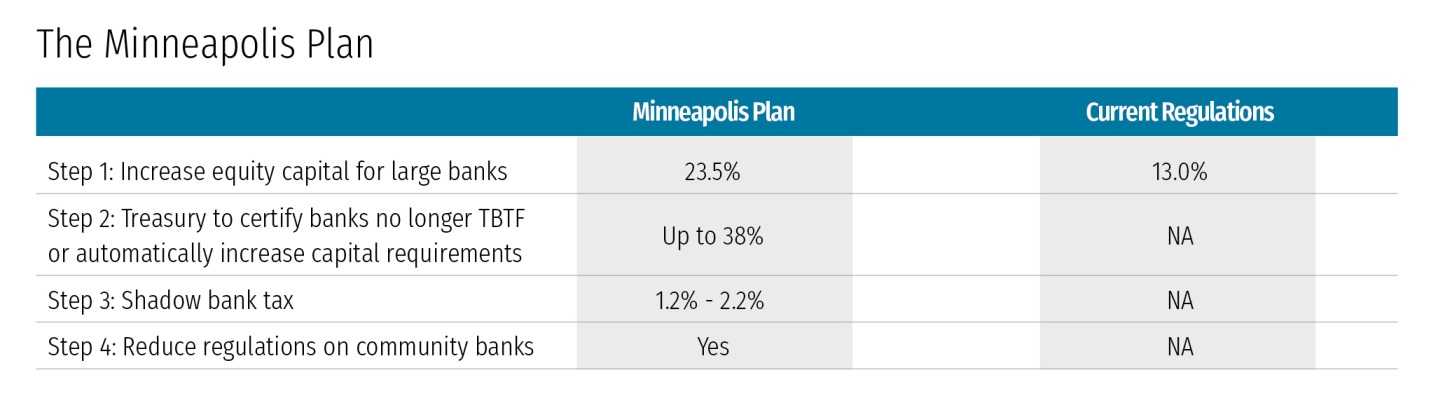

Here I describe the four steps of the Minneapolis Plan and compare them with the current regulatory framework.

Step 1 of the Minneapolis Plan dramatically increases capital requirements for all bank holding companies larger than $250 billion to 23.5 percent of risk-weighted assets. And we count only common equity as capital. That is a key difference from current regulations, which also set 23.5 percent as the total amount of loss absorption that the largest banks must have, but current regulations include long-term debt in that amount. History has shown that long-term debt is not useful protection against losses in a crisis. That’s why we insist on common equity.

Step 2 of the Minneapolis Plan then calls on the U.S. Treasury Secretary to analyze and certify that individual large banks are no longer TBTF. If the Treasury Secretary refuses to certify a large bank as not TBTF, that bank will face dramatically increasing capital requirements, until either the Treasury Secretary certifies it as no longer TBTF or its capital reaches 38 percent. This is a critical step, because today there is no time limit for solving the TBTF problem. Today, banks can enjoy their explicit or implicit status as being TBTF potentially indefinitely. In contrast, the Minneapolis Plan puts a hard deadline on Treasury: Certify banks as no longer TBTF within five years, or else that bank will see dramatic increases in capital requirements. We believe the threat of these massive increases in capital will provide strong incentives for the largest banks to restructure themselves so that they are no longer systemically important. Any bank that remains TBTF will have so much capital that it virtually cannot fail. This is the approach regulators have taken with nuclear power plants. People understand that if a nuclear reactor melts down, it is devastating for society. Rather than ban nuclear power, regulators impose such tight restrictions on it in order to truly minimize the risk of failure. Step 2 takes the same approach with the largest banks.

Step 3 imposes a tax on debt for large shadow banks, greater than $50 billion, including hedge funds, mutual funds, and finance companies, of either 1.2 percent or 2.2 percent, depending on whether they are systemically risky. One of the concerns many experts expressed was the potential for risky activity to move from banks to shadow banks. If we increase capital requirements on banks and the risky activity just moves to large shadow banks, has safety actually improved? To protect against this scenario, our proposed tax will roughly level the playing field between banks and shadow banks by equalizing the cost of the funding so that activity doesn’t just move to a less-regulated segment of the financial system. Shadow banks that do not utilize debt funding will not pay any tax.

Finally, Step 4 rationalizes regulations on community banks, which are not systemically risky for the U.S. economy and that do have a vital role to play in American communities. Banks with less than $10 billion in assets should be subject to a much simpler and less burdensome regulatory framework that reflects their relative lack of risk to the economy.

I have gone through these steps very quickly. We will no doubt go into more depth in the discussion, and there are full details in the published materials.

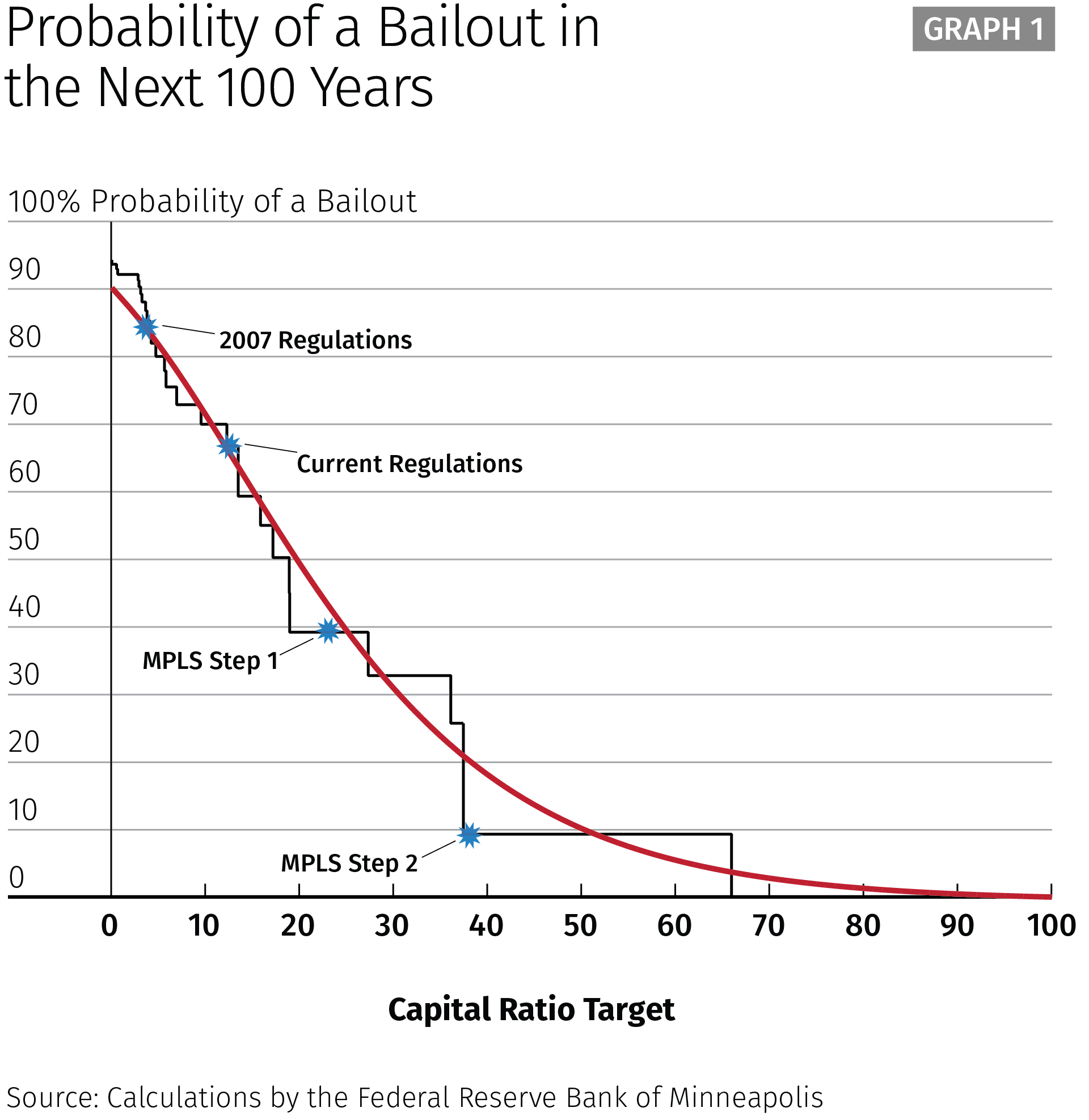

Now let me turn back to how we estimate the probabilities of future financial crises, because this is essential to evaluating whether current regulations go far enough or if we should do more.

As I mentioned, we utilize the best data available on historical financial crises, data from the IMF. This chart utilizes the IMF data to estimate the probability of a future bailout as a function of capital requirements in the banking sector. The X axis is capital ratios and the Y axis is the odds of a bailout over a 100-year time horizon. The black line has steps in it, because it represents actual data from past financial crises, and, as I mentioned previously, crises are fortunately infrequent events. The red line is a smoothed version of the same data, which we use in some of our calculations.

The blue star at the top of the chart indicates the regulatory system in 2007, before the crisis.

The star a little down from it shows the current regulatory framework, a modest increase in capital and a modest reduction in risk.

The next star shows Step 1 of the Minneapolis Plan, with a larger increase in capital and a much larger reduction in risk.

Finally, the bottom star shows Step 2 of the Minneapolis Plan, with a dramatic increase in capital and reduction in risk for the largest banks. We know this is not an exact science, but looking at prior financial crises is the best way we know how to estimate the effect of potential regulations in order to assess safety in the U.S. financial system.

Finally, what will the financial system look like after the Minneapolis Plan has been fully implemented? We will have fewer mega banks, and there will be far less concentration in the banking system. We expect that community banks will thrive and mid-size banks will make up a far larger share of the overall system. The financial system as a whole will be much, much better capitalized and capable of withstanding a major shock without triggering a crisis. If there are any TBTF banks left, they will be so well-capitalized that their risk of failure will truly have been minimized. Like terrorism, we can’t eliminate all risk. But we believe the Minneapolis Plan does a much better job of reducing risks at reasonable costs to society than current regulations. Ultimately, the public needs to make their own determination. We hope this process will equip them with the data and analyses they need to make an informed judgment.

Thank you. I now look forward to our discussion.

Endnotes

1 I wish to thank Javier Bianchi, V.V. Chari, Ron Feldman, Ken Heinecke, Jean Hinz, Patrick Kehoe, Jim Lyon, Brendan Murrin, Danita Ng, Fabrizio Perri, Jason Schmidt, Jenni Schoppers, Tom Tallarini, David Wargin and Niel Willardson.

2 See the Full Proposal of the Minneapolis Plan for all calculations and references to source materials.