Author

In July 1832, Congress sent a bill to renew the charter of the Second Bank of the United States to the White House for President Andrew Jackson’s signature. The measure had passed both the Senate and House by comfortable margins; many legislators and their constituents believed that over the past decade the Bank had proven itself a wise and efficient overseer of the nation’s monetary affairs.

The institution had virtually erased the government’s debt from the War

of 1812. Its paper notes were as good as gold anywhere in the Union.

State banks and businesses had benefited from tens of millions of

dollars in loans by the Bank. Thanks to its interregional payments

system, trade was flourishing from Boston to Chicago, on the expanding

frontier. These successes argued for a new lease on life for the Second

Bank.

The institution had virtually erased the government’s debt from the War

of 1812. Its paper notes were as good as gold anywhere in the Union.

State banks and businesses had benefited from tens of millions of

dollars in loans by the Bank. Thanks to its interregional payments

system, trade was flourishing from Boston to Chicago, on the expanding

frontier. These successes argued for a new lease on life for the Second

Bank.

Jackson begged to differ. The war hero known as “Old Hickory” to his followers considered the Second Bank an unconstitutional “money power” that favored wealthy stockholders over working people and twisted democracy to its own ends. As the bank bill sat on his desk, Jackson lay ill, suffering from a flare-up of an old battle wound and the hot, sticky weather. Martin Van Buren, who would succeed Jackson as president, visited the White House one day and found his mentor lying on a couch, pale and gasping for breath.

“The bank, Mr. Van Buren, is trying to kill me,” he said in a whisper. Then Jackson grasped his friend’s hand tightly and added, “but I will kill it.”1 True to his word, Jackson vetoed the bill, and four years later, upon expiration of its charter, the Second Bank closed its doors. There would not be another bank like it for 77 years, until the formation of the Federal Reserve System.

The creation and destruction of the Second Bank were flashpoints in a long-running debate in the United States over the need for a central bank and how the economic power of such an entity should be controlled. Established as a national bank to restore financial order after the war with Britain, the Second Bank got off to a rocky start. But led by the brilliant and forceful Nicholas Biddle, the institution thrived and developed into a de facto central bank with some functions analogous to those of the modern Federal Reserve. Most scholars agree that by issuing a uniform currency, ensuring access to credit and facilitating domestic and international trade, the Bank fostered economic stability and growth in the 1820s and early 1830s.

But what many regarded as a force for public good came to be seen by others as a plutocracy that held too much sway over the nation’s fortunes. “Many people have argued that United States history shows the suspicion of all concentrated power but a special suspicion of concentrated financial power,” said Richard Sylla, an economic historian at New York University, in an interview.

The Bank War in which Jackson and his supporters killed the Second Bank was a reprise of the bitter fight 20 years earlier over the recharter of the First Bank of the United States (see the September 2007 Region). Congressional opponents brought down the First Bank by charging that the brainchild of Alexander Hamilton was unconstitutionally powerful and an oppressor of state-chartered banks. Similarly, Jackson aroused populist passions and the envy of state banks to topple an institution that he considered unconstitutional and a menace to society because of its unrivaled economic power exercised outside government control. Biddle’s desperate efforts to save the Bank, prostrating the economy in hope of forcing Jackson to relent, showed even its supporters that the Bank was capable of abusing its power.

The architects of the Federal Reserve System took to heart the fate of the Second Bank. Instead of a mostly private bank that massed financial power in one city, the framers of the Federal Reserve Act created a federal bank composed of 12 independent, regional banks overseen by a central board in Washington, D.C. The eventual legacy of the Second Bank was a more democratic banking system that has rendered largely moot the ideological struggle that doomed its predecessors.

For “the public exigencies”

The idea of a national bank was reborn during the War of 1812. The war had thrown the country into financial chaos, with federal debt mounting as the government borrowed heavily to prosecute the war and a British naval blockade of eastern seaports suppressing foreign and coastal trade. Economic activity shrank and investor confidence plummeted.

It didn’t help matters that there was no longer a national bank to issue a uniform currency. The closing of the First Bank in 1811 had greatly increased the number of state-chartered banks issuing their own notes. In 1814, when British raids on Washington and Baltimore triggered bank panics, many state banks stopped redeeming their notes in specie (gold and silver coin). In a monetary system that relied on a bimetallic standard to restrain note issue (paper currency could be readily exchanged for specie held in bank vaults), the refusal of banks to stand behind their notes caused their notes to depreciate at different rates. The uncertain value of paper money complicated financial transactions, disrupting commerce.

The depressed economy hampered the federal government’s efforts to collect revenue and raise money from bond issues, resulting in defaults on public debt. Moreover, without a national bank, the U.S. Treasury had no one bank to go to for a quick loan, and no easy way to move funds to where they were needed. In 1814, Congressman Alexander Hanson of Maryland reported that the Treasury had so little money and credit that it was unable to pay its stationery bill.2

Before the war, the Republican Party founded by Thomas Jefferson had decried the First Bank as a corporate monopoly that flouted the Constitution and enriched financiers while bilking yeoman farmers and other ordinary workers. But after the war, ideological objections gave way to the pressing need to fix a sputtering economy. The Treasury needed a national bank to furnish it loans, hold government deposits and restore the value of currency by pressuring state banks to resume specie payments.

President James Madison, who had vehemently opposed Hamilton’s original proposal for the First Bank but supported recharter because he believed the constitutional issue had been settled by precedent, now urged Congress to provide a bank for “the public exigencies.” Madison emphasized the nation’s money woes in his December 1815 annual message (today’s State of the Union address): “The benefits of an uniform national currency,” he said, “should be restored to the community.”3

Congressman John C. Calhoun of South Carolina then introduced a bill to establish a national bank, offering in its favor a rebuttal to the old argument against the First Bank’s constitutionality. The Constitution gave Congress an exclusive right to regulate the value of currency, he said; therefore it had an obligation to do so, by creating a national bank that would impose discipline on state banks.

Calhoun’s argument and those of other bank proponents were persuasive; Congress passed the bank bill, and the Second Bank opened for business Jan. 7, 1817, in the same building in Philadelphia that the First Bank had once occupied.

Under its 20-year charter, the new bank had much in common with the old. The government owned a fifth of its stock; merchants, landowners and other private investors held the rest. Three-quarters of its privately held shares were to be purchased with government securities, enhancing demand for the country’s war debt. Backed by its stock and government deposits, the Bank was authorized to issue a sizable currency suitable for the payment of taxes and to lend to businesses as well as government.

However, the Second Bank was a much bigger institution than its predecessor, with more than three times the capital and many more branches (by 1828, there were 25 serving every part of the country, compared with the First Bank’s eight). Another difference was the government’s somewhat larger say in the daily operation of the new institution. Directors chosen exclusively by stockholders ran the First Bank; in the Second Bank, five of 25 directors were appointed by the U.S. president with Senate approval.

Avarice and panic

Reincarnated to breathe life back into the economy, America’s national bank appeared to do more harm than good in its early years. Its first president was William Jones, a Philadelphia merchant and politician backed by businessmen in Baltimore eager to tap the Bank’s wealth. The Second Bank began its career, recalled future Bank president Nicholas Biddle years later, as “a monied institution governed by those who had no money … a mere colony of the Baltimore adventurers.”4

The Bank lent aggressively to merchants and land speculators, and gave sweetheart loans secured by the Bank’s own stock to Jones’ associates. In the Baltimore branch, lending to directors and other insiders without collateral resulted in a loss of $1.5 million—$21 million in today’s dollars.

Ironically, one of the recipients of these fraudulent loans—Baltimore Cashier James W. McCulloch—is immortalized in a landmark U.S. Supreme Court case that seemed to affirm the Second Bank’s constitutionality once and for all. In 1818, the state of Maryland had imposed a stiff tax on the Baltimore branch and other banks not chartered by the Legislature. In McCulloch v. Maryland, the court ruled that the states had no power to interfere with a bank incorporated by Congress under the necessary-and-proper clause of the Constitution.5

Profligate lending weakened the Bank, and—coupled with its failure to persuade all but a handful of state banks to resume specie payments—caused paper currency to depreciate at varying rates in different parts of the country, weakening the national economy.

On the brink of collapse, the Bank was forced to retrench, calling in loans and slashing circulation. Langdon Cheves, who replaced Jones as president in 1819 after a congressional inquiry into the Bank’s problems, tightened credit further—just as the country was sinking into a depression. The Bank’s efforts to save itself worsened the Panic of 1819, which caused widespread bank and business failures.

Many scholars believe that the Bank’s actions (or inaction) during the Panic sowed the seeds of its later destruction. Jane Knodell, an economic historian at the University of Vermont, notes that in the west, where Bank branches had been active in lending for land purchases, the Bank repossessed people’s livelihoods. “There was lingering resentment,” Knodell said in an interview. “People saw the Bank acquiring all these assets that were formerly theirs, and that created some pretty permanent enemies for the Bank.”

Nicholas Biddle’s bank

After serving as a government director of the Second Bank, Biddle became its president in 1823. A member of a prominent Philadelphia family who had turned his talents from literature to finance (see “The Rise and Fall of Nicholas Biddle”), Biddle transformed a national branch banking system with federal fiscal duties into a functional central bank, a forerunner of the Federal Reserve. Sylla of NYU points out that by leveraging the Bank’s currency reserves, Biddle systematically regulated the monetary system for the good of the overall economy in a period when the Bank of England was only tentatively flexing its monetary muscle. “I could make an argument that he was the world’s first self-conscious central banker,” Sylla said.

An effective tool for regulating the money supply was the Bank’s holdings of notes issued by state banks. As the chief repository of customs duties and other government revenue, the Bank received millions of dollars annually in such notes, which could be redeemed for gold and silver (the majority of state banks had reluctantly resumed specie payments by this time). Because most banks kept minimal specie reserves, they were forced to curtail lending when the big bank in Philadelphia or any of its branches demanded specie.

To tighten credit, the Second Bank promptly presented state banknotes for redemption, sometimes buying banknotes in the money market to apply more pressure; to ease credit conditions, the Bank held onto the banknotes, letting the banks lend more freely. Through this early form of open market operations, Biddle and his lieutenants aimed “to preserve a mild and gentle but efficient control over the monied institutions of the United States,” as Biddle explained in an 1826 letter.6

The Second Bank also regulated the money stock by issuing currency and lending to state banks. The Bank’s notes, legal tender for the payment of taxes and accepted everywhere at par, were the closest thing the country would have to a national currency until after the Civil War. Biddle kept a tight rein on circulation, making sure that the Bank provided an adequate money supply while removing the temptation of some branches to overissue by requiring that notes be payable only at the bank location that issued them.

Loans to banks—provided by the Federal Reserve today to banks that cannot otherwise meet their reserve obligations—allowed them to avoid calling in loans when bank runs or regional trade imbalances drained their specie reserves. Historians credit timely lending by the Second Bank for helping to avert bank failures during the global stock market crash of 1825, which closed scores of banks in Britain.

In addition to fine-tuning the monetary system, the Bank stimulated interregional and international trade through bills of exchange, financial instruments that enabled farmers and merchants to obtain payment for their goods from customers in distant markets. By selling drafts at a premium, the Bank acted as a clearinghouse for long-distance transactions—a function roughly similar to check clearing at the Fed.

Unlike the Federal Reserve, the Second Bank operated as a commercial bank as well as a central bank. The Bank profited from its domestic and foreign exchange business, which competed with services offered by state banks and brokerages; and it accepted deposits from and made loans to businesses and individuals.

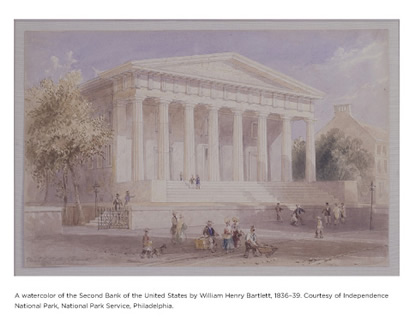

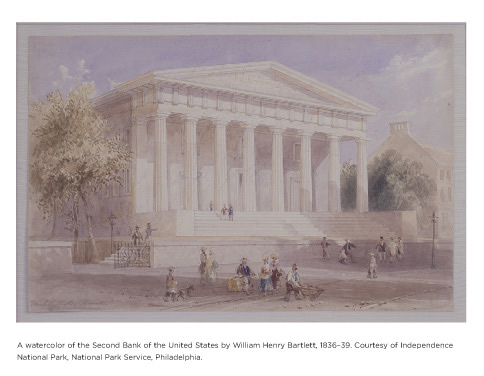

By the time Jackson was elected president in 1828, the Bank was, in historian Robert V. Remini’s words, a “financial colossus, entrenched in the nation’s economy.”7 Headquartered in a splendid new building on Chestnut Street and modeled on the Parthenon (the structure still stands, in the care of the National Park Service), the Bank was by far the largest corporation in the nation. The head office and its branches maintained a note circulation of $21 million, held one-third of the banking system’s total bank deposits and specie, and accounted for 20 percent of the country’s loans.8 At the colossus’ head was Biddle, his sure hands on the levers and pulleys, personally directing the Bank’s lucrative commercial business and tightening and relaxing access to credit at will.

But some Americans disapproved of the Bank’s power, none more resolutely than Jackson. The president and Biddle would soon be locked in a Manichean struggle over who should govern the nation’s monetary system.

The Bank War

Jackson held a jaundiced opinion of banks. Like Jefferson, he believed they perverted democratic ideals, profiting bank stockholders and mercantile interests at the expense of the working class. As a young man, he had been stung in a land speculation scheme, an experience that soured him against paper money and banks in general. Jackson was hostile to the Second Bank in particular because of what he perceived as its stranglehold on financial power—the ability of a single private institution to redistribute wealth among different social classes and regions of the country.

The president was also convinced that the Bank was wielding its financial clout against his party, the Democrats (or Jacksonians). He had heard reports that during the last election, the Bank had bought votes in Kentucky to assist the reelection of Republican John Quincy Adams, donated money to the National Republican party and spurned the loan applications of Democrats. Whether or not they were true, the rumors deepened Jackson’s animus toward the Bank, convincing him that its power must be curbed.

In his annual message of 1829, Jackson attacked the Bank, resurrecting the constitutional issue. A literal interpreter of the Constitution and an ardent supporter of states’ rights, Jackson asserted what he saw as his prerogative to disagree with the Supreme Court’s decision in McCulloch v. Maryland. He also charged—contrary to available evidence—that the Bank had failed to establish a uniform currency, and he proposed that the Bank become an arm of the Treasury in order to bring it under closer government supervision.

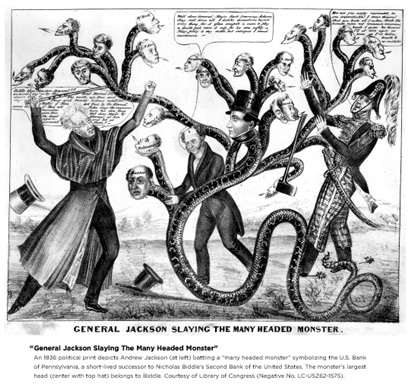

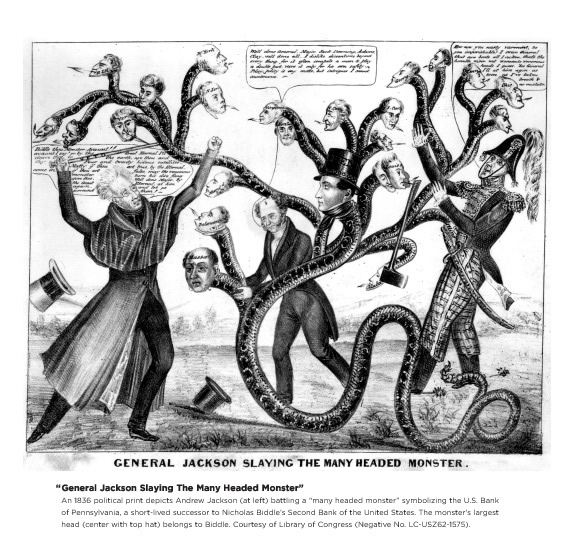

Over the next two years, Jackson stepped up his campaign against the Bank, denouncing it in speeches and letters as a “monster,” a fearsome hydralike creature that threatened liberty and the Republic. Jacksonian newspapers such as the Washington Globe picked up on this bestial imagery, excoriating the Bank in editorials and cartoons.

Old Hickory’s accusations struck a populist chord with farmers, laborers and artisans who shared his view of the Bank as a tool of the rich that threatened equal opportunity, the essence of democracy. Many Jackson supporters in western and southern states still resented the Bank for calling in loans and foreclosing on their property during the Panic of 1819. Allied with the populists were state banks and businessmen who chafed under Biddle’s “mild and gentle” monetary restraints in an era when credit was in high demand to fuel economic expansion and development on the frontier. Wall Street bankers were jealous of the Bank’s financial might and coveted its federal deposits.

As what came to be known as the Bank War escalated, Biddle the master financier found himself out of his depth. “Where Biddle gets into trouble is his political skills, or lack thereof,” Knodell said. “He made a lot of bad moves.”

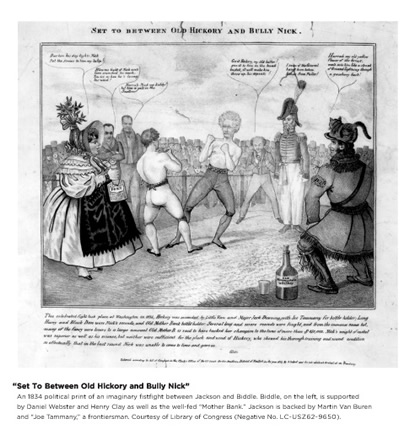

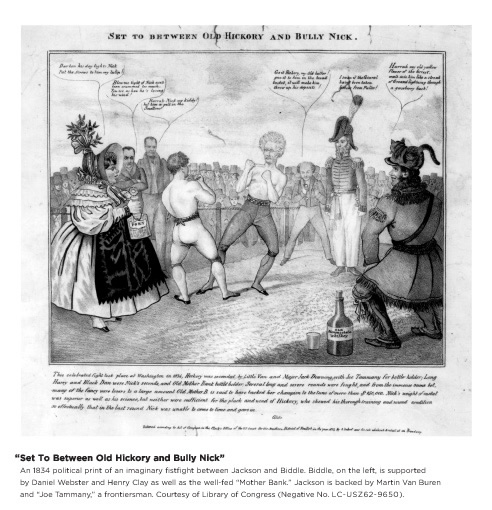

Compromise may have been possible with Jackson, who in December 1831, looking to enhance his reelection chances, signaled that he was willing to make peace with the Bank. But Biddle didn’t propose substantive changes to the Bank charter that might have mollified the president and ended the Bank War. Instead he used Bank funds to place newspaper articles praising the Bank’s salutary influence on commerce and to pay handsome retainers to politicians such as Massachusetts Sen. Daniel Webster, an eloquent spokesman for regulation of currency and credit.

Then Biddle made a strategic blunder that sealed the fate of the Bank. Encouraged by Webster and presidential aspirant Henry Clay, who wanted to make the Bank’s future an issue in the 1832 election, Biddle applied to Congress to renew the Bank’s charter. The charter still had four years to run, but Webster, Clay and other Bank supporters believed that Jackson would be more likely to sign a recharter bill before the upcoming election than afterward.

Fight to the finish

They were mistaken. The bank bill easily won approval in both the Senate and the House, receiving strong support from lawmakers in New England and the Middle Atlantic states. But Jackson was waiting, ailing yet determined to not just chain the “monster” but kill it outright. In his famous veto message of July 10, 1832, Jackson blasted the Bank, insisting that it was unconstitutional—not “necessary and proper” for the execution of Congress’ powers—and depicting it as a financial monopoly that granted “titles, gratuities and exclusive privileges to make the rich richer and the potent more powerful.”9

Dismissing Jackson’s veto message as “a manifesto of anarchy,” Biddle redoubled his lobbying in an effort to get Congress to override the veto, courting legislators with large bank loans. And he openly supported Jackson’s rival Clay in the 1832 election, drawing upon Bank funds to distribute Clay’s speeches in favor of a national bank and recharter. Biddle’s aggressive politicking availed him nothing; Congress lacked the will to overturn the veto, and Jackson scored a landslide November victory over Clay.

When an emboldened Jackson took steps in the fall of 1833 to remove the Second Bank’s Treasury deposits and give them to “pet” banks friendly to the administration—a move that would cripple the Bank as a regulator of currency—Biddle made a last desperate bid to save his Bank. So far he had used Bank resources to curry political favor by retaining high-powered lobbyists and bribing newspaper editors and lawmakers. Now, in an act that would be unthinkable for a financial institution today, Biddle deliberately curtailed credit to inflict misery on the money market and force Jackson to not only return the deposits but agree to recharter as well.

Decreasing lending was a natural defensive response to the loss of federal deposits, but Biddle took matters to extremes. Over the next few months, he cut loans drastically and ordered state banks to immediately pay off their debts in specie—which forced many banks to curtail their own lending. By the following spring, the Bank’s assets and demand liabilities had fallen by a fifth, contributing to a recession exacerbated by general panic. Banks and mercantile houses collapsed, wages and real estate values fell, workers lost their jobs. Delegations of businessmen begged the president to restore the deposits and end Biddle’s contraction. Jackson sent them packing, and Biddle was now committed to a fight to the finish. “My own course is decided—all the other Banks and all the merchants may break, but the Bank of the United States shall not break,” Biddle wrote in February 1834.10

Finally, Biddle was forced to relax his chokehold on credit when the public and even the Bank’s supporters turned against him. His scorched earth policy seemed to confirm what Jackson was saying; the Bank was indeed an all-powerful, dangerous beast that must be destroyed for the good of the nation. With its federal deposits drained away, the Bank lost the ability to restrict the note issue of state banks and ceased functioning as a central bank. After the Bank’s charter expired in 1836, Biddle defiantly kept the head office going as a private, state-chartered institution, but the bank was dogged by mismanagement and allegations of fraud, and it collapsed in 1841. The building that the Bank’s enemies had derided as “the Greek temple in Chestnut Street” became a U.S. Custom House.

The once and future bank

Jackson’s pet banks multiplied and lent exuberantly in the mid 1830s, providing the funds entrepreneurs craved to start new businesses and expand operations. Economists have estimated that between 1834 and 1836, the money supply grew at an average annual rate of 30 percent, sparking a commercial boom but also rampant speculation in land and commodities. In a replay of events following the demise of the First Bank, notes issued by state banks depreciated, forcing Jackson to intervene by ordering federal officials in July 1836 to accept only specie for the purchase of public lands.

Within a year, the speculative bubble burst in the Panic of 1837. There’s considerable debate about the exact causes of the Panic and subsequent deep depression that lasted until 1843, but recent scholarship has shown that the death of the Second Bank was a significant factor. Knodell’s research, for example, indicates that the closing of Bank branches spurred private investment in western state banks, which leveraged that equity and their new federal deposits to make risky long-term loans for land development. When many of those loans turned bad, the banks were forced to curtail credit, quickening the country’s slide into depression.11

Banking booms followed by busts would occur roughly every decade for the rest of the 19th century and into the 20th. Without a bona fide central bank to exercise control over currency and access to credit, the monetary system was susceptible to periodic banking disruptions.

Finally, the Panic of 1907—a stock market meltdown and ensuing recession relieved by the intervention of financial mogul J. P. Morgan—prompted the creation of the Federal Reserve System in 1913. In designing an institution that would issue a uniform currency, hold Treasury deposits, discount commercial paper for banks and perform other central bank functions, the founders of the Federal Reserve were aware of the traumatic history of the Second Bank. They understood that the immense financial power the Bank put in the hands of a select few bred distrust and disaffection.

In 1909, Sen. Nelson Aldrich of Rhode Island, chair of a commission charged by Congress with reforming the monetary system, invoked the Second Bank in a speech to a group of Chicago businessmen. Aldrich said that the Bank had been “destroyed as a matter of party policy” and assured his audience that any new central bank would be governed and structured differently from its predecessors to avoid becoming mired in politics. “[N]o one is thinking of adopting the First or Second Bank of the United States as a model,” he said. “No institution of similar construction or methods in management could possibly receive the approval of the people of the United States at this time.”12 Two years later, Aldrich chided critics of his central banking plan for conjuring “the ghost of Andrew Jackson” to stir up political opposition.13

Aldrich’s vision of a central bank that avoided the political pitfalls of the past was a starting point for a central bank proposal developed by Rep. Carter Glass of Virginia and economics professor H. Parker Willis. The new institution created by the Federal Reserve Act struck a balance between public and private, centralized and local control of the monetary system. A Federal Reserve Board in Washington would oversee operations carried out by “not less than eight nor more than twelve” District Banks spread around the country, under the direction of representatives from local banks.

Thus the Federal Reserve did not concentrate financial power in the private sector and in one city, as the Second Bank had done. And unlike the Second Bank, it was not a commercial bank; it would assist state and national banks—by lending them reserves and clearing checks—but not take business away from them. The ghost of Andrew Jackson could rest in peace.

Legislation during the Great Depression restructured the Federal Reserve, giving more power to an oversight board in Washington and less autonomy to the 12 District Banks. Today’s Fed is fundamentally a government entity dedicated to the public interest, not private gain. This is the legacy of the nation’s first central bank, an institution that fostered prosperity during most of its 20 years of life. How the Second Bank died is a cautionary tale about the political dangers of concentrated financial power that appears to benefit private or parochial interests rather than the nation as a whole.

Endnotes

1 Martin Van Buren, Autobiography, ed. John C. Fitzpatrick (Washington, 1920), p. 625.

2 Bray Hammond, Banks and Politics in America: From the Revolution to the Civil War (Princeton, N.J.: Princeton University Press, 1957) p. 230.

3 Ibid., p. 233.

4 Charles Sellers, The Market Revolution: Jacksonian America 1815-1846 (Oxford University Press, 1991) p. 134.

5 17 U.S. 316 (1819).

6 Hammond, p. 307.

7 Robert V. Remini, Andrew Jackson and the Bank War: A Study in the Growth of Presidential Power (New York: W. W. Norton, 1967) p. 39.

8 Ibid.

9 Ibid., p. 83.

10 Nicholas Biddle, The Correspondence of Nicholas Biddle, ed. Reginald C. McGrane (New York: Houghton Mifflin, 1919) pp. 221–22.

11 Jane Knodell, “Rethinking the Jacksonian Economy: The Impact of the 1832 Bank Veto on Commercial Banking,” Journal of Economic History 66(3), pp. 541–74.

12 “Keep banks free, Aldrich advises,” New York Times, Nov. 7, 1909,

p. 7.

13 “Bankers indorse Aldrich money plan,” New York Times, Nov. 22, 1911, p. 9.

A note concerning the art for “The ‘Monster’ of Chestnut Street”The Region acknowledges generous assistance from Karin Murphy of the Federal Reserve Bank of Minneapolis; Karie Diethorn, chief curator, and Andrea Ashby, photo librarian, Independence National Historical Park, Philadelphia; Susan Drinan of the Atwater Kent Museum, Philadelphia; and Erica Kelly, photoduplication services, Library of Congress. |

Related Content

{kind=link}

{kind=link}

{kind=link}

Related Content