Author

The Quick Take

While it’s not a new phenomenon, consolidation among health care providers appears to be growing in activity and expanding in form. Traditional mergers and acquisitions are expanding health care organizations to offer more services to a broader market. But consolidation has also morphed into many different structural and legal forms that stop short of traditional mergers and acquisitions but achieve strategic objectives for both organizations.

Consolidation, in its many shapes, sizes and arrangements, appears to be accelerating as health care organizations look to achieve greater scale to address a dizzying array of market and government pressures. Reimbursement policies, technology, regulations, capital needs, shifts in patient care and other factors have combined to create a state of flux in health care that is making organizational independence more and more difficult.

To many, it’s a four-letter word—spelled with 13 letters. It comes eventually to any big industry, whether farming, auto-making or banking. It’s often feared, at least until one becomes familiar with it, or its alternative. But like it or hate it, it’s probably coming to your health care provider in one of many shape-shifting forms. The word comes laden with emotion, denoting a loss of independence, with small-town businesses getting gobbled up by a faceless corporation. It should almost come with its own dramatic background music.

Consolidation. The combining of two or more previously separate businesses is in full force among health care providers, with large numbers of mergers and acquisitions as providers seek both horizontal breadth and vertical integration to offer the most care services to the most people.

Earlier this decade, Medcenter One, based in Bismarck, N.D., started considering partners for its 228-bed hospital, a college of nursing and seven primary clinics and care facilities serving western and central North Dakota communities like Dickinson and Jamestown. After kicking the tires on possible suitors, in 2012 the organization merged with Sanford Health of Sioux Falls, S.D., but not without some controversy, said Craig Lambrecht, president of Medcenter One at the time, and now president of the newly formed Sanford Bismarck.

“People were scared to death” because there was a lot of uncertainty about potential layoffs and the autonomy of local providers, said Lambrecht. “Once we engaged [employees and the community], that fear dissipated.”

For health care providers, consolidation is simply a logical business reaction to a multitude of economic and policy pressures that require new strategies for providers to remain viable given prevailing, even conflicting, policies for managing costs and getting paid for the care provided.

But this isn’t your father’s consolidation, so to speak. While there are plenty of traditional mergers and acquisitions among providers, consolidation is fundamentally about a relationship between two entities for the economic benefit of both.

As the complexity of health care increases, so do the number of legal arrangements between providers—partnerships, affiliations, joint ventures and other agreements. These “consolidation lite” arrangements offer smaller shifts in control while giving each party better competitive footing in a grueling health care market.

The many shapes, sizes and arrangements of consolidation activity today stem from a dizzying array of drivers. Most can be boiled down to the chase for greater efficiencies and leverage made possible by economies of scale and pursued for the sake of addressing steadily rising health care costs.

But the desire for scale is itself driven by a host of market and regulatory pressures within a dauntingly complex U.S. health care system. Reimbursement policies, technology, government regulations, capital needs, shifts in patient care and other factors have combined to create a state of flux in health care that is making it harder for organizations to remain independent.

The business of consolidation

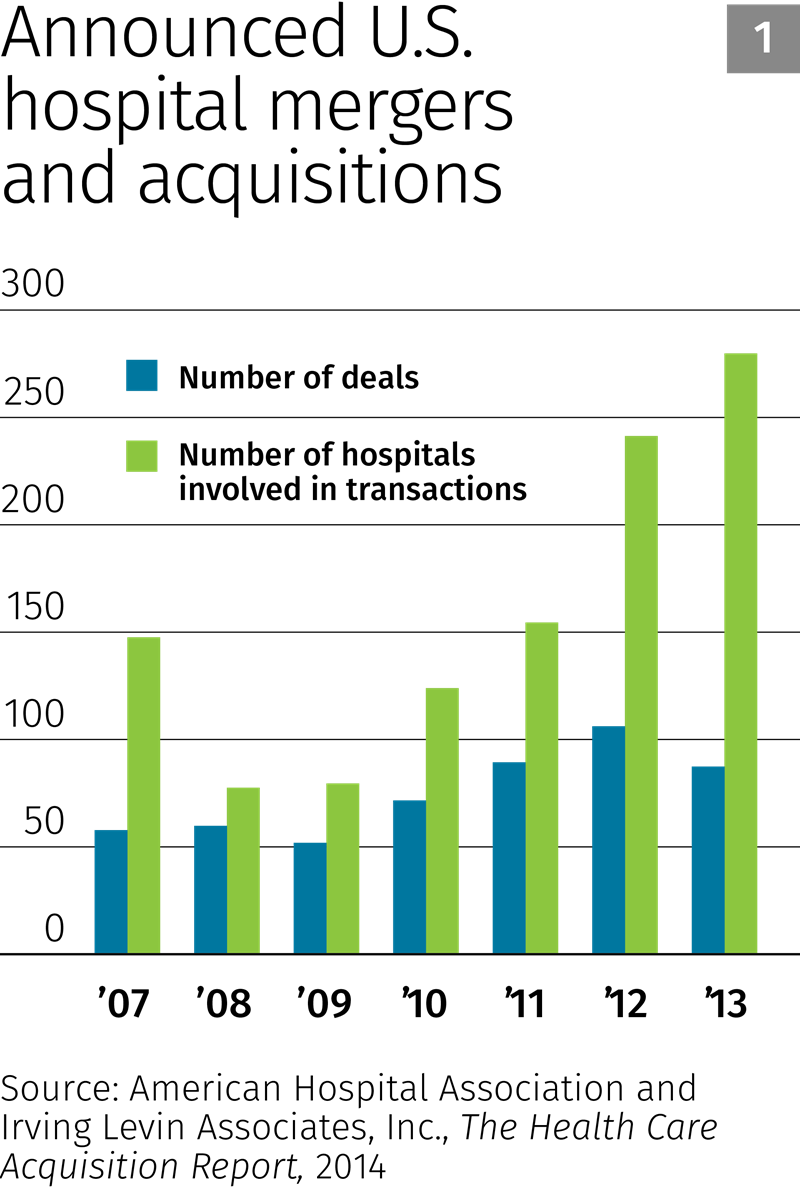

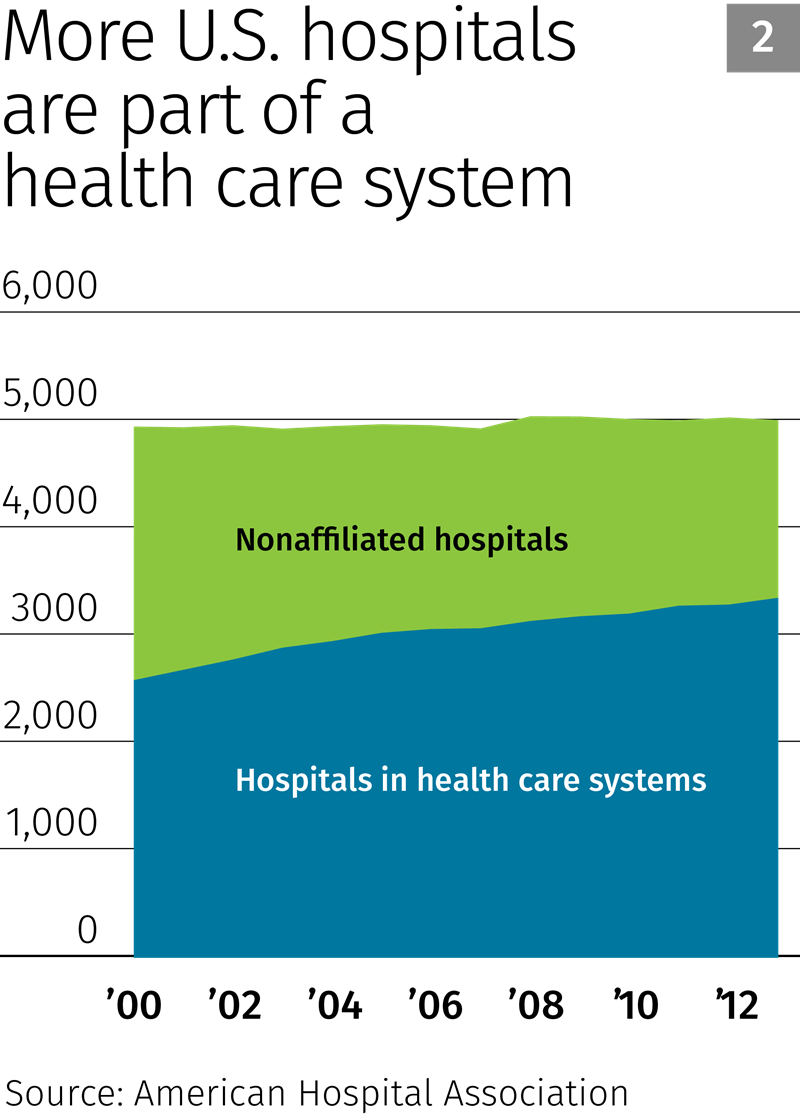

Evidence of consolidation among health care providers is all around. Since 2008, there has been an increase nationwide in the number of mergers and acquisitions among hospitals, according to industry consultant Irving Levin Associates (see Chart 1). As a result, more hospitals than ever are part of a health care system rather than operating independently, according to the American Hospital Association (see Chart 2).

Much of this consolidation is horizontal in nature; providers are seeking to either enter or expand in a given market by acquiring similar providers. In Minnesota, the number of private hospitals that remained unaffiliated with another health care organization fell 26 percent (from 62 to 46) from 2003 to 2013, according to data from the Health Economics Program with the Minnesota Department of Health. The total number of unique private health care systems in the state fell by a similar percentage (see Chart 3).

But consolidation also travels vertically as health care providers acquire other providers to expand available care services and build larger and broader internal referral loops so that patients don’t have to seek care elsewhere.

One of the biggest vertical consolidation trends deals with hospital-based health care systems buying up previously independent physician groups. Historically, most primary and even many specialty care physicians have been employed independently and given special admitting and treatment privileges at hospitals.

That’s changing, as more hospital-centric health care systems add so-called hospital outpatient departments (HOPDs) that look and act much like traditional physician-owned clinics. An Accenture report this year noted that “the era of the independent physician that many adults grew up with is swiftly coming to an end.” In 2000, 57 percent of physicians practiced independently, outside a larger health care system. In 2013, that number had fallen to 37 percent, and Accenture projects a further fall to 33 percent by next year. (See “Loss of independent physicians” for more discussion of this trend.)

Though there are no official data on the matter, that trend appears to be present in Ninth District states. In Montana, there has been a “tidal wave” of physicians leaving private practice to become hospital and/or health care system employees, according to Carter Beck, president of the Montana Medical Association. In Minnesota, physician groups were a hot target for health care systems, “but that game is pretty much done,” with many available groups already getting snapped up, said Mary Brainerd, CEO of HealthPartners. (Full disclosure: Brainerd is the former chair of the board of directors for the Federal Reserve Bank of Minneapolis.)

Specialists are also targets for vertical consolidation and integration. According to a national survey by the American College of Cardiology, the share of cardiovascular practices that are owned by physicians dropped from 59 percent to 36 percent from 2007 to 2012. Hospital ownership of these groups rose from 11 percent to 35 percent over this period (remaining ownership is with universities, government and health management organizations).

Different parts of the Ninth District appear to be at different stages of consolidation. Minnesota’s health care sector is viewed by many as already quite integrated, said Matthew Anderson, senior vice president for policy and strategy with the Minnesota Hospital Association (MHA), who responded at length via email. While there is still consolidation activity in the state, “the rate or frequency of those transactions has not been as feverish over the past five years as in other areas in the country.”

Loss of independent physicians: Follow the money

The downward trend among independent physician groups seems innocuous in the broader context of health care consolidation. But certain reimbursement policies have facilitated the shift.Read more

Given its smaller population and expansive geography, horizontal consolidation among hospitals “has not taken hold in Montana yet. However, there are a number of larger hospitals that have begun conversations” in hopes of expanding their markets and reducing costs, said Dick Brown, president of the Montana Hospital Association. There has been recent activity too. Earlier this year, Benefis Health System (Great Falls, Mont.) paid just $500,000 for Teton Medical Center (Choteau, Mont.), which included a 10-bed critical access hospital, clinic and 36-bed long-term care facility.

Activity in North Dakota has reportedly been heating up. “I think North Dakota has been isolated from consolidation for a lot of years,” said Jerry Jurena, president of the North Dakota Hospital Association (NDHA). The state has an independent streak, and health care organizations traditionally respected each other’s territorial lines.

That changed around 2009, Jurena said, pointing to two events. The first was the merger of MeritCare in Fargo—the state’s largest health care system at the time—with Sanford Health. The resulting entity has become one of the nation’s largest nonprofit, integrated rural health care systems.

The other factor? “They discovered how to get oil out of the ground at a good price,” said Jurena. The oil boom and the subsequent crush of workers coming to the state “brought a whole new clientele” for health care organizations, “who started to see market potential that they wanted to be involved with.”

HORIZONTAL CONSOLIDATION garners the most attention—especially when it comes to mergers and acquisitions. This happens when a large provider, like a hospital, acquires smaller independent hospitals or when a large integrated provider merges with another health system. The goal here is to enter new regional markets or expand in existing ones. In Minnesota, the number of independent hospitals has fallen by about one-quarter since 2003.

When Medcenter One started considering a marriage partner for its sizable operations, “we looked at all the options, and the best option was to go with Sanford,” said Lambrecht. At the time, Sanford had little presence in western North Dakota, and the company pledged to invest $200 million over the coming decade to improve Medcenter facilities and services. This saved some medical services at locations in smaller communities that might otherwise have gone away, because “we could not have afforded them,” Lambrecht said.

In 2014, Sanford built a new $30 million clinic in Dickinson, six times the size of the previous facility, giving patients there better access to primary and specialty care closer to home.

“That’s why the merger was so attractive,” said Lambrecht. “It allowed us to be relevant.”

Smaller, one-off acquisitions tend to reinforce regional markets. Sanford Health grew its Minnesota presence from nine hospitals to 15 from 2003 to 2013, acquiring smaller facilities in the western part of the state in places like Alexandria, Bagley, Thief River Falls and Wheaton. In 2004, Benedictine Health System and St. Mary’s Duluth Clinic Health System merged their seven Minnesota hospitals to eventually form Essentia Health, based in Duluth. By 2013, Essentia had grown to 12 in-state hospitals, mostly by acquiring facilities in rural northeastern communities like Aurora, Deer River and Virginia.

Not every merger involves a major health care system. In some cases, mergers happen between smaller organizations in the same regional market looking to become stronger by joining forces.

In rural northwestern Wisconsin, NorthWoods Community Health Center and The Lakes Community Health Center merged in 2013 to become NorthLakes CHC. “They were both small CHCs with minimal patient base,” said Lisa Olson, director of policy and programs for the Wisconsin Primary Health Care Association, an organization supporting CHCs statewide. “They decided it made the best sense to leverage their strengths and merge … to attract and maintain [qualified health plan] contracts as well as leadership staff.” Turnover of executive and clinical staff was high at both organizations, said Olson.

As a result of the merger, “NorthLakes is more efficient than the two separate entities were,” and the five northern Wisconsin locations offer greater access to a broad array of services, including medical, dental, chiropractic, behavioral health, and occupational and speech therapy. “They now have the largest seal-a-smile program in the state” to provide tooth sealants to kids in schools, said Olson.

Missing a lot of detail

But this overview of health care consolidation leaves out a lot of detail and activity. Unfortunately, measuring the full scope of provider consolidation over time is difficult because the health care sector is so large, at 17 percent of the economy, yet government tracks virtually none of the consolidation activity (though Minnesota offers a few modest exceptions). Private sources fill some of the void, but they typically offer limited insights on a state or regional level.

Hospitals and major health care systems receive the lion’s share of attention in news accounts and other analysis regarding consolidation—not surprising given their size and common status as large employers. But the provider market has exploded outside of hospitals, thanks to growing markets for different care services and settings—many of them still comparatively small, private entities. In Minnesota alone, the number of advanced diagnostic imaging providers roughly tripled between 2003 to 2013—to more than 80—and the total number of unique facilities more than quadrupled, to 272, according to data from the Minnesota Department of Health. The large majority are not owned by major health care systems—at least not yet, as they seem likely to face many of the same consolidation pressures that hospitals and physician groups face.

Beyond mergers and acquisitions

More than a thousand miles separate Mayo Clinic in Rochester, Minn., and Livingston HealthCare, in Livingston, Mont., and possibly as much virtual distance lies between their organizational size, structure and complexity.Read more

So getting a good picture of the state of consolidation is more art than data science. This is especially the case because there is also an undercurrent of other transactions that are bringing more providers together in formal, but less comprehensive ways, leveraging some of the benefits of consolidation without the ownership shift that occurs in a merger or acquisition. These transactions vary in the depth and breadth of legal integration among the parties involved, ranging from management contracts to joint ventures and long-term leases.

Getting any measure of this type of consolidation—everything below mergers and acquisitions—is nearly impossible. Activity encompasses a multitude of legal forms and agreements and no one, public or private, is tracking these transactions, partly because they are privately negotiated and partly because some transactions are mundane—like a management agreement that gives a smaller hospital access to group purchasing through a larger health care system. But sources say this grayer area of consolidation and integration is the most active (see “Beyond mergers and acquisitions” for examples and more discussion).

“We’re seeing huge creativity in the market in this regard … and a lot of interdependent relationships” are developing as a result, said Terry Hill, senior adviser at the National Rural Health Resource Center in Duluth, Minn. He attributed this growth partly to the complexity and imperfections of the health care sector, which creates incentives for experimentation. But this activity is also occurring because of “the difficulties in merging [health care organizational] cultures as much as anything,” said Hill.

Keith Anderson is a partner in the health care practice at the law offices of DrinkerBiddle and consults for major health care systems nationwide. “I’d describe strategic transactions today as frenetic … and they’ve really accelerated” over the past half-dozen years or so, said Anderson. “We see a lot of creative models” in the types of transactions that bring providers together. In many of these, providers “are not looking to merge or sell off assets. They are picking teams” to compete in a variety of areas—recruitment, contracts, IT systems and value-based care models, to name a few.

Driving for change

The forces behind the many forms of consolidation are both simple and exceedingly complex. At its core, consolidation is a market reaction, a structural response by providers that see larger size and broader reach as a competitive advantage, bringing efficiencies that flow through to the bottom line and, ideally, to patients.

In the case of health care, providers are pursuing scale for numerous reasons, but most of them have some relationship to rising costs.

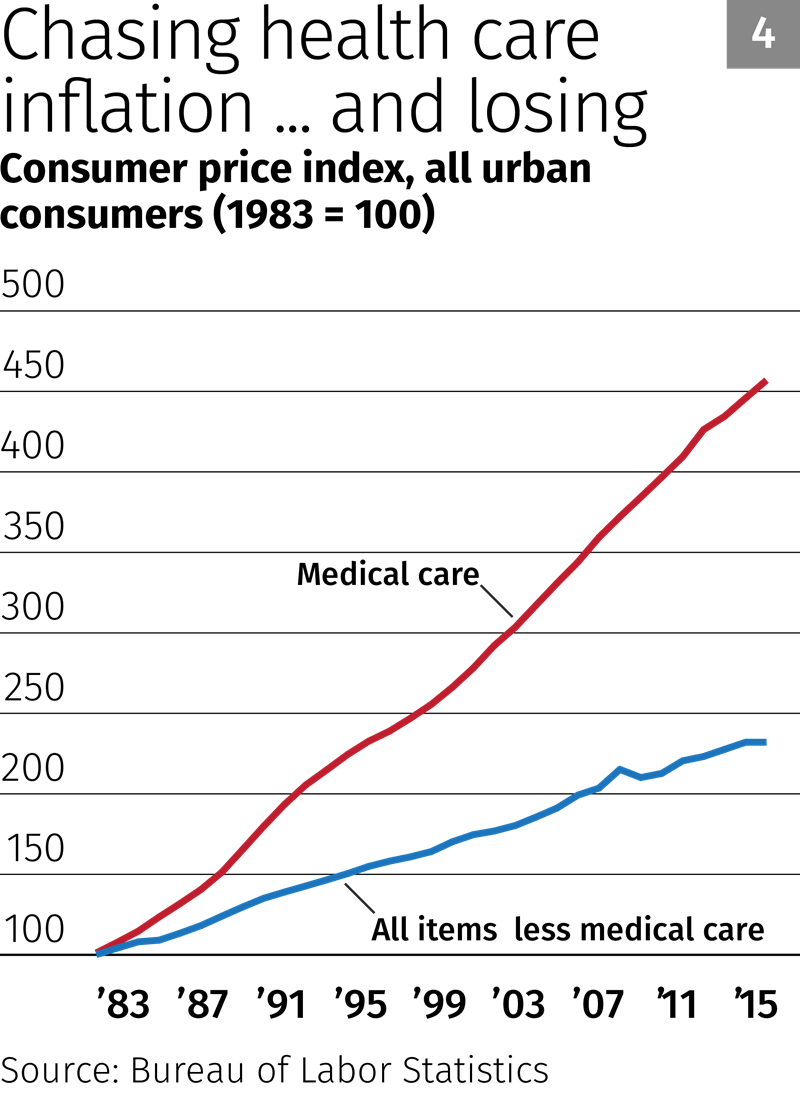

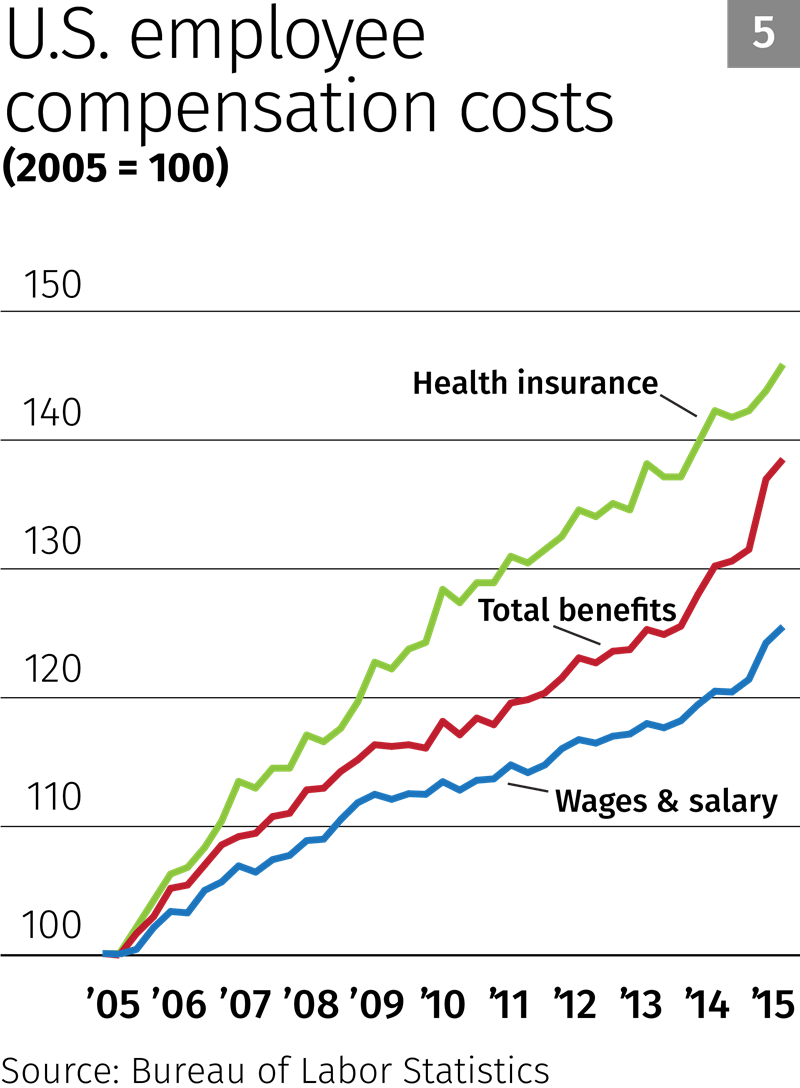

Although health care cost increases have slowed in recent years, costs have consistently been well above inflation in the rest of the economy (see Chart 4). It’s not hard to connect the dots: Spending for Medicare and Medicaid programs has been rising rapidly, and health insurance costs for employers have increased much faster than wages and other benefits since 2006 (see Chart 5).

“As employers and government payers continue to look for ways to reduce health care spending, their efforts will put further pressure on health care providers to reduce costs and increase risk management,” said Scott Duke, president of the South Dakota Association of Healthcare Organizations.

But “rising cost” is itself rather obtuse. It springs from a multitude of other sources, and unbundling some of these factors offers a better picture of the more direct drivers behind consolidation.

(Editor’s note: For a better sense of the many disparate factors driving provider consolidation, see a wide range of examples in the “Grab Bag” boxes sprinkled throughout the text that demonstrate the scope of forces affecting providers.)

For example, human labor makes up 60 percent to 70 percent of costs at a hospital, according to Jurena, from NDHA, “and there is not enough go around,” especially for high-skill positions. A hospital administrator in Bismarck told Jurena that if 200 nurses showed up tomorrow, “he could hire all of them.” A Fargo hospital administrator put the number at 100 nurses.

Minnesota job vacancies in the health care and social services sector more than tripled over a five-year period, reaching 18,000 in 2014, according to biennial surveys by the Minnesota Department of Employment and Economic Development.

Tight labor markets tend to push up wages. In Minnesota and North Dakota, average weekly wages for hospital workers have risen 18 percent (inflation-adjusted) since 2010, according to the Quarterly Census of Wages and Employment. Such circumstances—high vacancy rates in the face of rising wages—make consolidation more attractive, as providers look for efficiencies that can reduce labor need, especially in administrative and other nonmedical positions.

Build it and they will … charge you for it

Capital costs are also a powerful driver of consolidation in health care. Kelby Krabbenhoft, president and CEO of Sanford Health, called health care “one of the most capital-intensive industries in America.” Small hospitals and other providers often struggle to keep up, and as a result “have been amalgamating for some time.”

VERTICAL CONSOLIDATION is done to expand the care services available to patients. This is often referred to as a “cradle to grave” model, and includes the acquisition of providers to build larger and broader internal referral networks. This way, patients don’t need to seek care anywhere else. There are no hard measures, but vertical consolidation appears to be quite strong currently as providers react to the Affordable Care Act and other forces seeking greater care integration.

Capital needs run the gamut, from facilities to advanced medical equipment to the electronic health records that keep track of all those doctor visits. Many rural facilities, for example, are “Hill-Burton hospitals,” named after the federal law in 1946 that gave grants and loans to mostly rural hospitals to grow and modernize over the coming decades. Many have not been updated over the years, “and patients expect more modern buildings, equipment, all the bells and whistles” that come with health care services today, said Michael Topchik, senior vice president at iVantage, a health care analytics firm.

Upgrading such facilities often becomes prohibitively expensive, given razor thin operating margins common in the industry. Many hospitals “have been happy to get by on 1 to 2 percent” net income margins, said Krabbenhoft, but that’s why they have outdated facilities and equipment. The industry target now is 4 to 5 percent, Krabbenhoft said, because “no matter how hard you try, you can’t get by on 1 to 2 percent margins.”

In 2013, 27 percent of Minnesota hospitals had bottom-line margins of 2 percent or less, according to financial data from the Health Economics Program with the state Health Department. Another 9 percent of hospitals cleared that bar only because of other income from nonhospital operations.

But modernizing outdated facilities is just one of the many capital mouths to feed at every health care organization—small or large, rural or urban. New technology, for example, promises increased consumer demand but comes at a steep price. “It’s not that they just need a new emergency room or a new roof,” said Krabbenhoft. “Now they need technology for care, and it’s so, so expensive.”

Cardiac ultrasound scanning systems cost an average of $158,000 in June, almost 12 percent more than a year earlier, according to the ECRI Institute, a nonprofit medical research and technology assessment organization that tracks equipment purchasing and pricing. But that’s a pittance compared with the price of other big-ticket items like MRI machines ($1.5 million) or PET/CT scanners ($1.9 million). Average prices for the 10 most popular capital items rose by 7 percent in June compared with a year earlier, according to ECRI.

Still, even these costs can pale compared with those associated with federal mandates for electronic health records (EHR), systems that keep track of medical histories and provide access for any authorized user, including patients.

To insure “interoperability” among providers, EHR requires entirely new information technology systems, and hardware and software costs can quickly run into the millions—often with additional zeroes. “It’s an expensive ordeal, and there is no reimbursement for that,” said Jurena.

Krabbenhoft said that Sanford has spent more than $1 billion across its network of facilities for seamless record keeping and sharing. With the Medcenter One merger, Sanford has spent $30 million to $40 million “just getting rid of a hodge-podge of IT systems.”

And expense aside, few small providers have the technical know-how to properly manage such systems.

Matthew Anderson, from MHA, said the challenge of installing and maintaining an EHR system that meets federal requirements “appears to be perhaps the most significant factor” among many pushing consolidation.

There is also consolidation activity that stops short of a traditional merger or acquisition, but still achieves strategic objectives for both entities. CONSOLIDATION LITE can take many forms. For example, it can help multiple providers affiliate for a particular objective—like contract negotiation with insurers. Or a management agreement can allow a large health system to give small providers access to their expanse of resources. These types of transactions aren’t new, but they are increasing, thanks to expanding market and regulatory pressures.

As a federal mandate, EHR is part and parcel of growing costs for regulatory compliance. Health care organizations are required to gather truckloads of data on patients, fill out binders of paperwork and jump through other operational hoops to be reimbursed and to meet patient safety and other requirements. A 2014 survey of about 20,000 doctors by the Physicians Foundation found that doctors spend 20 percent of their time on nonclinical paperwork, and that doesn’t consider the compliance efforts of other workers.

A study by PricewaterhouseCoopers and the American Hospital Association found that on average, every hour of patient care provided entails 30 minutes of paperwork. Administrative work benefits from economies of scale, making consolidation an attractive option.

Beck, from the Montana Medical Association, said “exploding” regulatory compliance costs stemming from the Affordable Care Act and other government regulation have “significantly driven the vertical integration … forcing doctors out of private practice.”

Bill collector

On the other side of the financial ledger, reimbursements play a big role in consolidation, particularly those from the country’s largest health insurance plans, Medicare and Medicaid, the federal health care programs for the elderly and poor, respectively. The populations of both programs have been rising, and their combined share of national health care expenditures has grown steadily, from 27 percent in 1990 to 38 percent in 2013 (see Chart 6).

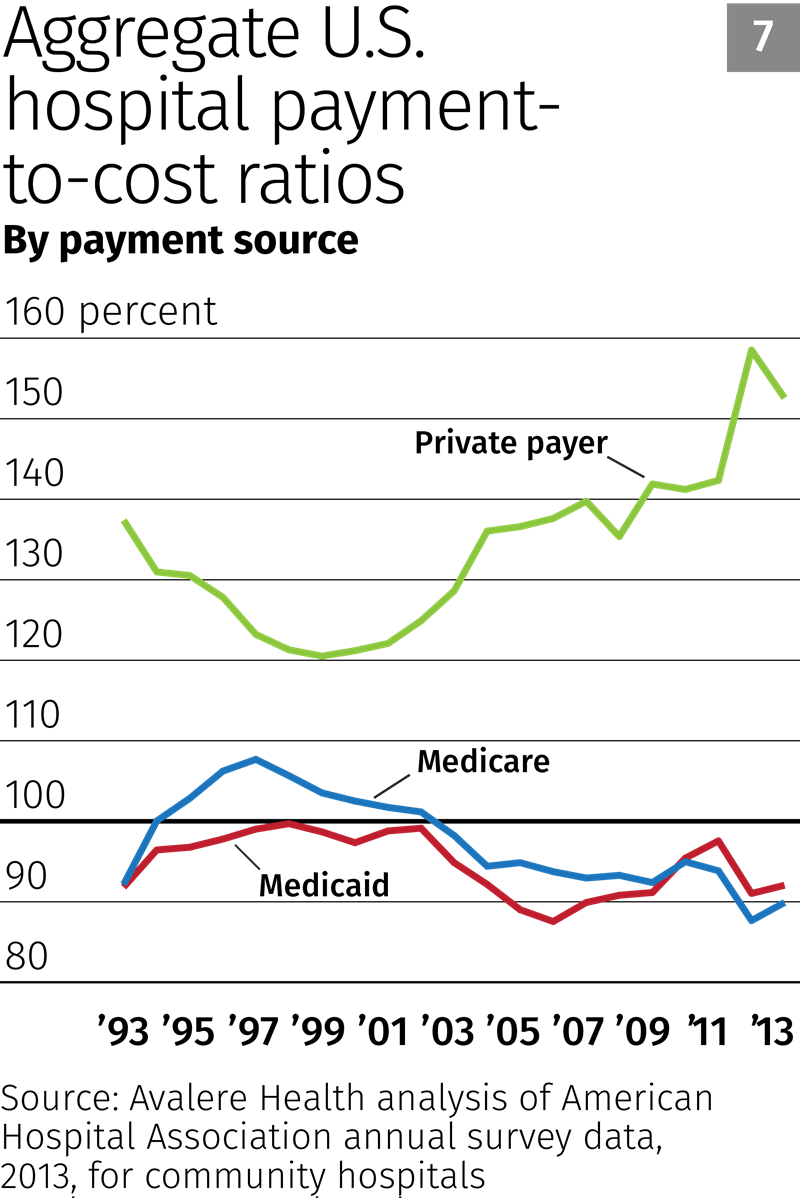

The federal government sets the prices that providers receive for patient care from Medicare and Medicaid—for providers, there’s no negotiating prices. With rising enrollments, the federal government has attempted to control expenditures by tightening the allowable costs that providers can claim for reimbursement—so much so that the operating margin (payments minus cost) for the average Medicare and Medicaid patient has been in the red for a decade and a half. Providers currently receive about 90 cents for every dollar of service provided to these patients (see Chart 7).

“We haven’t figured out how to care for the patient and get paid for it,” said Jurena, who has worked in the sector since 1975. “So everybody is struggling because you don’t have a model that works.”

To keep the doors open, providers have increased what they charge a shrinking base of patients with private insurance. Consolidation helps providers on both ends: It offers centralized expertise in dealing with regulation and paperwork associated with Medicare and Medicaid reimbursements, as well as federal regulation in general, making these patients comparatively less expensive. In the private-payer market, consolidation also expands networks and limits competition, helping to maintain pricing leverage with health insurance companies and the employer plans they sponsor, which have much higher profit margins.

The Accenture report attributed much of the decline of independent physicians to reimbursement pressures. A national survey by the American College of Cardiology attributed the drop in physician-owned cardiovascular practices to Medicare reimbursements that are higher for hospitals than for clinics.

The tensions of this fee-for-service reimbursement model is the impetus for a fundamental change in how care is provided and paid for, something several sources said represented a shift from “volume to value.”

“You’re seeing a compelling and dramatic shift in the very nature of how health care is financed,” said Krabbenhoft, of Sanford. This includes a shift to value- and risk-based contracting, where providers are paid upfront fees to manage the health of an enrolled population and rewarded or penalized depending on whether they meet certain health metrics and cut care costs for patients. (An example of this reimbursement model is accountable care organizations, or ACOs. See “Accountable care organizations” for more discussion.)

Accountable care organizations: The shift from volume to value

![]() Accountable care organizations (ACOs) are an example of new reimbursement models that replace the fee-for-service model with a so-called patient-centric model that emphasizes service value rather than service volume.Read more

Accountable care organizations (ACOs) are an example of new reimbursement models that replace the fee-for-service model with a so-called patient-centric model that emphasizes service value rather than service volume.Read more

The good news is that many sources see a fundamental, positive shift toward smarter health care spending. For example, if Medicare wants to hypothetically pay a significant, one-time fee to care for a patient for a year, and the provider gets to keep any savings but also bears the risk of overspending for care, “you start to think differently than if you get paid every time someone visits the hospital,” said Brainerd, from HealthPartners.

Under such a model, said one source, primary care becomes a driver of provider revenue by keeping patients out of the emergency room and off the surgery table; these expensive services become a net cost to the provider rather than a profit center, as they are in the current model.

But part and parcel with this shift toward value-based care, at least at this stage of development, is that it requires large patient populations to properly distribute and manage risk, and integrated networks offering a full continuum of care to better track and manage the health of a covered patient population. “You need analytics. You need financial heft to accept the risks” inherent in this care model, said Brainerd.

A pleasure to meet you, consolidation.

Build your own models

What consolidation hasn’t done yet is provide a clear view of the future of health care, or even whether it has been net positive for patients in terms of access, care quality and costs.

Sources widely agreed that little progress had been made on cost. “As is readily apparent to anyone, consolidation is not resulting in better pricing for consumers,” said Beck, from Montana.

Anderson, from MHA, was a little more sanguine about the overall effects of provider consolidation. “Studies generally show that the quality of care as a whole continues to improve across the country [and] that the rate of cost growth … has been more stable and lower than it has been in decades.”

But he acknowledged that “whether consolidation is necessary to achieve these results—or if similar outcomes can be achieved through other efforts of independent organizations—remains debatable. … Consolidation seems like a more clear, direct and intentional means to create the kind of alignment and coordination that produce better outcomes at lower costs. But there is not definitive proof that [consolidation] is the only way that providers can accomplish these goals,” Anderson said.

For the time being, it will be consolidation’s game to lose, as no sources believed a reversal of consolidation was likely in the near term. Foley, from Apple Valley Medical Center, said there will always be anecdotes “of two doctors leaving Mayo to start up their own practice, but … I think all big [health care system] corporations are looking to capture market share through mergers and acquisitions or alignment strategies. It’s all about the cost. Follow the money.”

Where the health care market currently lies along the full arc of consolidation is anyone’s guess. In many ways, health care is a constantly rejuvenating industry with new products and services developed to treat both rare and common afflictions that keep us kicking longer, giving birth to new markets and firms.

Health care is also still a regional market almost everywhere. That’s why every state has a small-to-large cadre of unique providers. Multiplied by 50 states, health care is still far from consolidated compared with many industries.

Keith Anderson, from DrinkerBiddle, said health care is not maturing as quickly as other industries like manufacturing, where consolidation typically leads to fewer business models. Anderson said that until fairly recently, health care has been “more of a cottage industry,” with providers at each level of care often not far removed from their local-owner roots.

“I think we’re a long way away” from the point at which consolidation starts to taper off, Anderson said. “But I think we have the seeds” of the models that will survive into the future.

Pointing to the likes of Mayo Clinic and Cleveland Clinic, highly reputable health care systems, “the common seed is that they employ physicians,” said Anderson. “This allows you to design a care model where the physician and hospital have the same stake in the outcome. They are bound together.”

Ron Wirtz is a Minneapolis Fed regional outreach director. Ron tracks current business conditions, with a focus on employment and wages, construction, real estate, consumer spending, and tourism. In this role, he networks with businesses in the Bank’s six-state region and gives frequent speeches on economic conditions. Follow him on Twitter @RonWirtz.