About eight million manufactured homes make up over 6 percent of the year-round housing stock in the United States. Manufactured homes are a widely used form of affordable housing in Indian Country. About 17 percent of reservation households currently reside in a manufactured home, on par with the rate in rural America generally, and close to half of the American Indians who borrowed to buy a home on reservation land in 2016 secured their loan with a manufactured home. Tribal communities are clearly aware that manufactured homes are a practical option for meeting local families’ housing needs.

—GOVERNOR VIRGIL SIOW, Pueblo of Laguna

Tribal communities are also familiar with the problems of factory-built housing, especially with “FEMA trailers” and pre-1976 units built to low quality standards. Over time, however, the quality available in manufactured homes has improved significantly, in response to federal regulations and market forces, making them a more viable affordable housing choice. This chapter discusses how tribal communities can take steps to mitigate the problems and accentuate the benefits, making manufactured homes a practical option for affordable homeownership on trust lands.

A recurring theme will be the differences between titling and financing a manufactured home as personal property (chattel lending) versus real estate (mortgage lending). These differences are especially important for Indian Country, due to the additional steps needed to pledge trust land leases as security for mortgages and the generally higher costs of chattel loans.

The HUD Code for Manufactured Homes

A manufactured home is a factory-built home that is essentially ready for occupancy upon leaving the factory, except for some inherently local tasks such as placing the unit on its site and connecting it to local utility networks. Since 1976 in the United States, the term “manufactured home” has had a specific meaning under the Manufactured Home Construction and Safety Standards Code of the U.S. Department of Urban Development (HUD). The standards have strengthened and broadened over time, especially in 1994, when stricter wind-resistance requirements were added. The standards now cover materials and performance standards for design, energy efficiency, fire safety, and more.

The HUD code preempts state and local building codes, allowing each factory to build homes to a single national standard. This guarantees a minimum quality standard for all new manufactured homes. It also promotes scale and efficiency in manufacturing and, thus, generates an affordable product.

Transportation and Installation

After their construction, manufactured homes must be transported to the buyer’s location and installed on site. At the buyer’s site, the home is set down and secured (e.g., by bolts or straps). About 37 percent are placed on a concrete pad or permanent foundation, with the others affixed mostly to blocks or piers.

The newly delivered home must also be connected to local water, sewer, electric, and utility systems. Transportation and installation together make up a significant share of the installed cost of a manufactured home, and the proper execution of these steps is critical to preserving the quality and integrity of the home and the safety and comfort of its occupants. HUD requires that installers be licensed and registered. In addition, manufacturers require specific setup procedures at the final site in order for their warranties to remain in effect.

The Existing Inventory of Manufactured Homes

The quality of manufactured homes still in use in the United States varies tremendously. New, high-end units are comparable to high-quality site-built homes and attract middle-income buyers. However, older units are still common and generally of lesser quality.

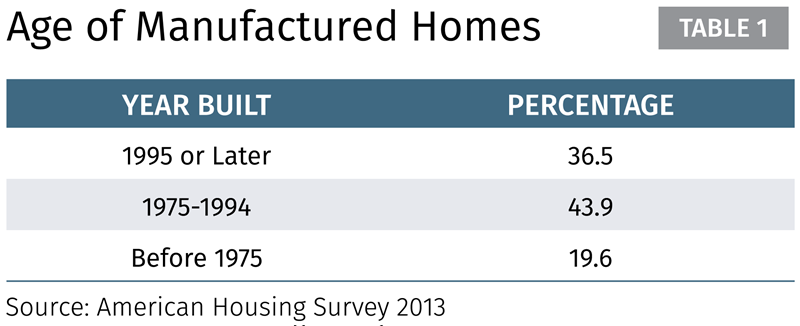

As shown in Table 1, about 20 percent of the manufactured homes in the U.S. in 2013 was built before the HUD code took effect in 1976. An additional 44 percent was built between 1975 and 1994, or mostly before the significant 1994 upgrades to the HUD code.

Once installed, most manufactured homes stay put. According to the American Housing Survey (AHS), about 80 percent of the manufactured homes were still located at their original site in 2013.

The Titling of Manufactured Homes

Titling is an important part of the manufactured homebuying process, especially in Indian Country. Unlike site-built homes, which are almost invariably titled as real estate, manufactured homes can be titled either as real estate or personal property (chattel). This is discussed further below in connection with financing a manufactured home and its possible placement on trust land.

Cost, Quality, and Appreciation—the Core Pros and Cons of Manufactured Housing

Manufactured or site-built—which is the best option for Indian Country homebuyers and tribal communities? There’s no one right answer. Traditionally the primary trade-off has been between the lower cost of manufactured homes and the perceived or real quality and long-term appreciation advantages of site-built homes. However, quality differences have narrowed over time, and research shows that appreciation is driven mostly by the value of the underlying land, not the home itself. (On trust land, individual allotments or long-term leases may substitute for outright ownership of the land.)

Cost

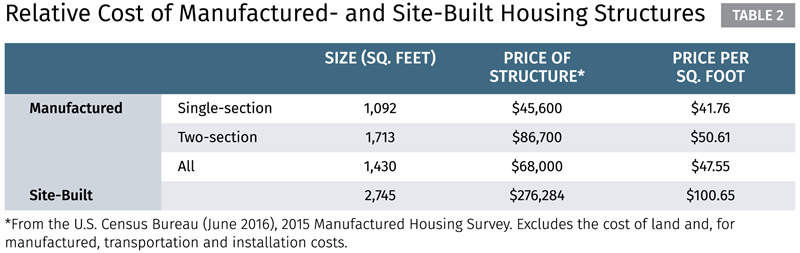

Low cost is the most obvious advantage of a manufactured home. As shown in Table 2, the cost per square foot of a manufactured home is estimated to be about half or less that of a site-built structure. Excluding land, a 1,700 square-foot structure, for example, could be built for about $86,000 in a factory (assuming two-section construction) as opposed to about $171,000 on-site.

Adding in the costs of transporting and installing the manufactured home narrows but normally does not close the gap. Transportation costs for a two-section home partly depend on distance but typically are between $3,000 and $15,000. Installation fees vary, often in the $1,000 to $5,000 range. The cost of a foundation is often between $6,000 and $20,000, but placement on piers is less expensive. Even at the high end of these ranges, or $40,000 for transportation, foundation, and installation, the cost of a typical manufactured home (excluding land) would be $126,000, about 26 percent (or $45,000) less than for the site-built home. These are very significant savings for low- and moderate-income families.

Consumers’ monthly housing costs also show an advantage for manufactured homes. Based on AHS data, the Consumer Financial Protection Bureau concluded, “Typical all-in housing costs for manufactured-home owners in nonmetropolitan areas were over a third less than the costs for households that owned a site-built home in a nonmetro area.”

Quality

If the cost of the home itself was the only consideration, manufactured homes would clearly be a leading option for expanding affordable homeownership. In practice, the choice is less clear, due to concerns about quality and appreciation.

The current HUD code has narrowed the quality gap between new manufactured and site-built homes. However, many older, lower quality manufactured homes are still available for sale. Buyers of older manufactured homes can find it difficult to judge a unit’s quality. Also, since most manufactured homes are titled as personal property, the quality disclosure requirements and other forms of consumer protection associated with real estate transactions often are not available.

Housing experts and consumer advocates still worry about the quality of new manufactured homes as well. Specific quality concerns still heard include:

- Uncertainty about the life span of new units.

- The quality of manufactured home inspections.

- The possibility that significant remodeling of a manufactured home may take it out of compliance with the HUD code (limiting financing options) and subject the entire home to local building codes, triggering additional expenses.

Appreciation

Another concern is that manufactured homes will not appreciate in value, preventing buyers from building home equity. However, the best study of this topic had a clear result— long-term control of the site is the key factor to appreciation of both manufactured and site-built homes. Specifically, the study found that, on fee simple land when the buyer owned both the home and land, the average rate of appreciation of manufactured homes was not significantly different from the average appreciation of similar site-built homes, according to AHS data for 1995-1999. Although no equivalent study has been done on trust lands, the logic of the study’s findings suggests that the same would be true for homes on individually controlled allotments or long-term leased lands.

Collectively, the three core factors—cost, quality, and appreciation—suggest manufactured homes have a place among the affordable homeownership options for low- and moderate-income households.

Manufactured Home Sales and Finance

The selling and financing of both new and existing manufactured homes can strongly affect buyer satisfaction and financial well-being, sometimes to the point of erasing the underlying cost advantage of manufactured homes.

A key factor is whether the manufactured home is financed as real estate, with a mortgage rather than a chattel loan. Nationally, about 60 percent of manufactured-home owners also own the land below the home. Nonetheless, from 2001 to 2010, most buyers financing the purchase of a manufactured home on land they own used a personal property, or chattel, loan.

A similar pattern probably holds In Indian Country, given the additional difficulties of using trust land as collateral. This is important, because chattel loans are typically more expensive than real estate loans.

Selling and Financing New Manufactured Homes

The selling and financing of new manufactured homes is somewhat more standardized and regulated than the selling and financing of existing manufactured homes.

New-home Dealers. Manufacturers are not allowed to sell directly to consumers, so new manufactured homes are sold through retail dealers. All dealers are licensed and bonded. Some dealerships are owned by a separate affiliate of the manufacturer or are franchised with the manufacturer’s backing. Others are independent but often small, with one or a few locations. Dealers are usually responsible for overseeing the transportation of the new home to the buyer’s site and its installation.

Consumers visit dealerships to inspect homes for sale. If the consumer wants features not available in the models on the lot, the consumer can work with the dealer to order the home they prefer. Price is often negotiated, as in a new car purchase.

Some consumer advocates have accused some dealers of abusive practices that take advantage of buyers. Alleged practices include:

- Adversely altering the agreed-upon terms of the sale at closing.

- Failing to provide buyers with full documentation.

- Delivering a home different from the one ordered or agreed upon.

- Poor after-sale service and failure to honor warranties.

New-home Financing. Manufactured-home dealers offer to finance the purchase, even taking the buyer’s loan application on-site during negotiations. The buyer can also arrange their own financing, perhaps with a local bank or credit union. However, some lenders only finance homes sold by dealers with whom they have a prearranged relationship. Buyers who wish to arrange their own financing must find a lender and dealer willing to work with each other.

Loans to purchase manufactured homes are relatively expensive. On the whole, for both chattel and real property loans, the CFPB found that manufactured-home loans were much more likely to be higher priced, and by a higher margin, than mortgages on site-built homes. This can significantly erode or even reverse the cost advantage that otherwise accrues to manufactured-home ownership.

Chattel financing of manufactured homes is especially expensive. The CFPB estimated that the annual percentage rate on new manufactured-home loans was about 1.5 percentage points higher for chattel loans than for mortgages.

Manufactured homes titled as real estate can qualify for lower-cost mortgage financing. In Indian Country, tribes can enter into a memorandum of understanding (MOU) with Fannie Mae or Freddie Mac to make competitively priced mortgage financing essentially equally available for site-built and manufactured homes on owned, leased, or allotted land.

Despite the higher cost of chattel financing, most loans for the purchase of a new manufactured home are secured only by the structure itself, as personal property, and not by the land the home will be sited on. Chattel financing remains prevalent even when the underlying land is owned by the homebuyer. This is partly because manufactured homes are still routinely classified as personal property under most state laws. In Indian Country, another factor is that owners of individual trust land may simply not want to deal with the burdens of obtaining the required paperwork for a mortgage on trust land.

Whatever the reasons, classification of manufactured homes as personal property requires the buyer to pay fees to title the property (similar to titling a car) and changes the consumer protections that apply to the sale and loan. For example, good faith estimates of mortgage closing costs, required by the Real Estate Settlement Procedures Act, are not required for chattel loans, and the procedures for repossessing personal property may be much simpler and quicker for the lender than the procedures for foreclosing on a mortgage.

Consumer advocates accuse some manufactured-home lenders of abusive practices, including in Indian Country. A typical complaint is illegal steering of buyers to expensive loans from lenders tied to the dealer.

Selling and Financing Existing Manufactured Homes

The resale market provides a low-cost option for homeownership, which can be especially relevant for families with very low incomes. However, buying an existing home involves additional challenges as well as opportunities, such as:

- Assessing the quality of the unit. Existing units vary significantly in quality, as a result of factors such as their original quality, age, maintenance, use, and whether they have been moved before. Buyers may be challenged to know whether the home they are looking at is a good deal or a lemon.

- Complying with local codes in a new location. If the unit is moved, the buyer needs to check if it complies with building codes in the new location. Older units may not satisfy current standards.

- Dealing with transportation and reinstallation. If the buyer plans to move the unit, additional transportation and installation costs are involved. Damage can occur in the process. These factors tend to reduce the resale value of manufactured homes that are moved.

- Obtaining finance. The limited number of lenders who finance existing manufactured homes tends to depress the value of these units. Some lenders at the low-price end of the manufactured-home resale market secure the loan with other collateral, such as the buyer’s vehicle.

- Whether to re-title the property as real estate. For manufactured homes titled as personal property but fixed to land owned by the homeowner, re-titling the home as real property may be advantageous. This can be useful even for owners not intending to sell because it facilitates refinancing, which is nearly unavailable for chattel loans. Re-titling may be especially useful if the owner is preparing to sell the land as well as the home. It helps attract additional interest from buyers who understand the appreciation advantages of real property and widens the array of financing options.

Enhancing Manufactured Homes as an Affordable Homeownership Option

Below are some steps that can help families decide whether a manufactured home is right for them and, if so, make their ownership experience more positive and beneficial.

- Understand today’s manufactured-home option. Manufactured homes have changed. It is increasingly important for community leaders and consumers to understand the pros as well as the cons of manufactured homes and why, on balance, manufactured-home ownership is an option many Indian Country families choose.

- Facilitate low-cost home finance, including for manufactured homes. Evidence shows that manufactured-home borrowers pay higher interest rates than buyers of site-built homes, especially when a personal property loan is used. Local actions to be considered for helping all home buyers while also reducing this gap include:

- Putting in place the agreements that make tribal members eligible for beneficial federal loan guarantee programs, such as HUD 184 and USDA 502 loans.

- Adopting ordinances and procedures to clarify and fairly govern the process for foreclosing on a mortgage, including a manufactured-home mortgage, especially on trust land.

- Adopting the Revised Model Tribal Secured Transactions Act (RMTSTA) and a companion lien filing system to clarify and govern the process for repossessing a manufactured home financed with a chattel loan.

- Working with Fannie Mae to ensure that the tribe’s ordinances make it eligible for the Native American Conventional Lending Initiative (NACLI), and encouraging lenders to partner as well.

- Encouraging local lenders, including community development financial institutions, to qualify as a Fannie Mae seller-servicer or to partner with an existing seller-servicer.

- Protect manufactured-home buyers. Navigating the homebuying process is a challenge, especially for the low- to moderate-income families that typically purchase manufactured homes. Tribal leaders may be able to help them and all manufactured-home buyers by:

- Getting to know the manufactured-home dealers that serve the reservation. Dealers are responsible for the buyer’s post-purchase warranty claims but are not always very responsive. Tribal leaders may be able to help buyers hold their dealer to account.

- Reaching out to state manufactured-housing industry associations that can connect tribal leaders and borrowers with retailers, lenders, and service providers.

- Partnering with the federal (HUD) or state government staff responsible for enforcing the HUD code on the reservation, including the code’s provisions for appropriate installation of manufactured homes.

- Understanding dealers’ licensing and bonding requirements. These requirements may put pressure on them to provide positive purchasing experiences and good after-sale service.

- Request that local vocational training programs consider covering training to transport, install, repair, maintain, and remodel manufactured homes.

- Educate tribal members on manufactured-home buying. Include information on the pros and cons of manufactured-home buying in new or existing personal finance or homebuyer readiness programs.

One of the most significant ways tribal leaders can address housing of any sort in Indian Country—stick-built or manufactured housing—is to facilitate the effective use of tribal lands for home ownership, including manufactured-home ownership. Many buyers may be better off if they place their manufactured home on owned land and title it as real estate. Tribal community leaders can make this easier by:

- Working with the BIA to ensure efficient processing of land leases for all homebuyers, including manufactured-home buyers.

- Educating all tribal members, from childhood on, about the history of the tribe and its lands, the meaning of tribal sovereignty, the significance of trust lands to the community and tribal sovereignty, and the procedures of putting trust lands to effective use.

- Requesting that affordable homeownership and housing programs serving the community incorporate appropriate coverage of manufactured-home options into their programming.

- Adopting tribal ordinances to facilitate the re-titling of manufactured homes from personal property to real estate and taking steps to make existing manufactured-home owners aware of the benefits of this option.

- Establishing tribal land use plans that clarify future infrastructure availability and areas zoned for residential use.

- Adopting manufactured housing ordinances that supplement the HUD code. For example, these ordinances could set minimum quality standards for used manufactured homes transported onto the reservation. Writing beneficial ordinances requires careful balancing of the community’s need to exclude unsafe or unsightly homes against low-income families’ needs for shelter. Tribes may wish to consult model ordinance or successful practices by other tribes.

These are only some of the steps that tribal leaders and others might consider. Their decisions will determine the extent to which tribal communities make wise and appropriate use of manufactured housing as an option for affordable homeownership in Indian Country.

Factory-built housing has become an important part of affordable housing.