Native Community Development Financial Institutions (CDFIs) play a vital role in providing homeownership opportunities for tribal members. These community-based loan funds are developing loan products to meet the needs of tribal members, creating strong lending portfolios, and showing private lenders that mortgage lending on trust land can be done. Here are three Native CDFIs focused on mortgage lending in different regions of the country:

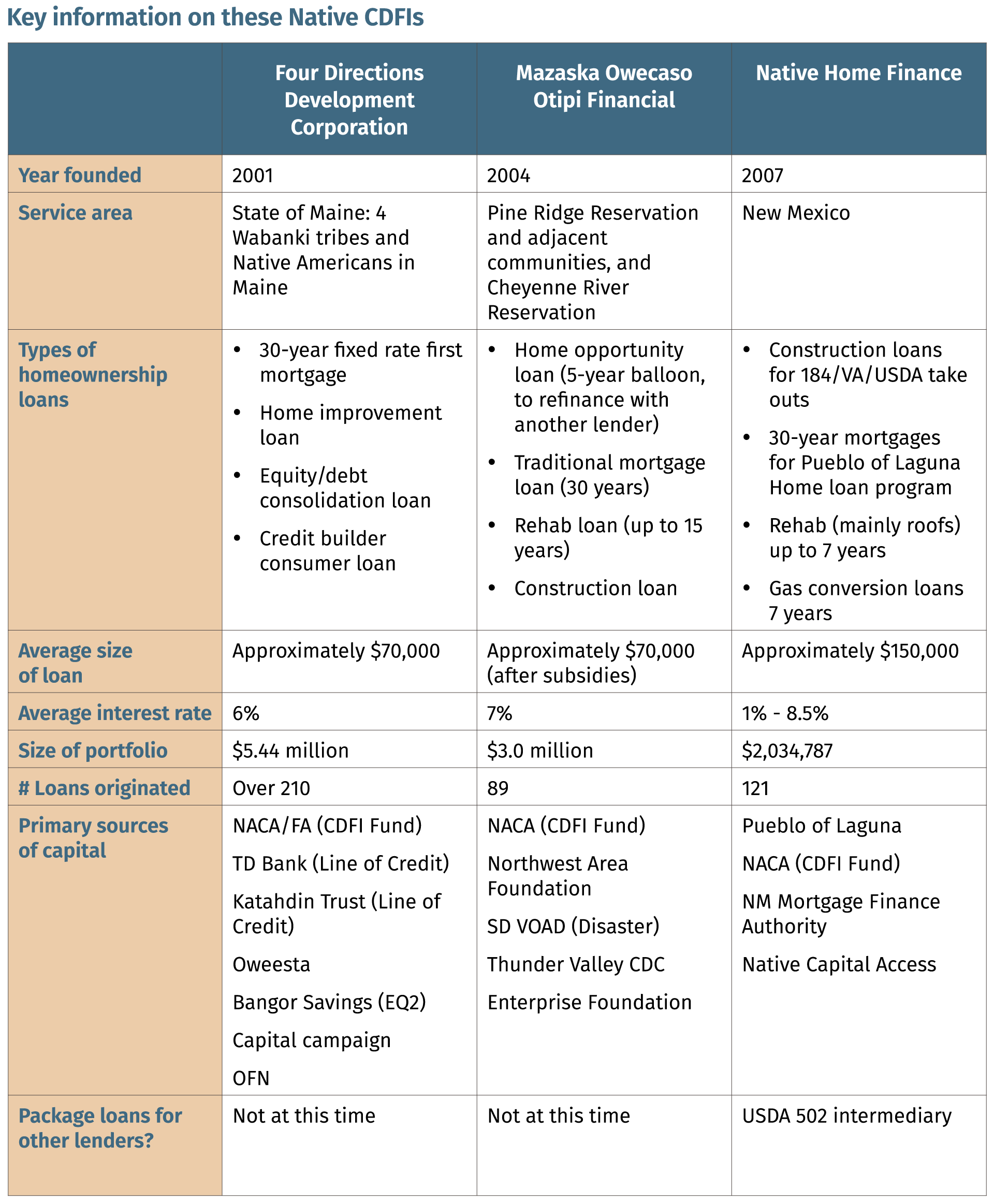

Four Directions Development Corporation, Orono, Maine

Created in 2001, Four Directions Development Corporation (Four Directions) is a Native CDFI serving the four Wabanaki tribes in Maine: the Penobscot, Passamaquoddy, Micmac, and Maliseet nations. In addition to a small business lending portfolio, Four Directions focuses primarily on home improvement, home mortgage, credit-builder, and home equity/debt consolidation loans. It also provides financial capability workshops and counseling. Based in Orono, Maine, its board of directors and advisory board are composed of tribal leaders, council members, and directors of tribal government departments, as well as non-Native members specializing in banking, small business, community development, and housing.

Native Community Finance, Laguna, New Mexico

Native Community Finance (NCF) is a CDFI started in 2007 through the interest of the Pueblo of Laguna (POL). NCF serves all of New Mexico’s tribes and pueblos, offering a variety of products and services for any Native American residing in the state. In addition to its POL mortgage loan product, NCF offers loans for home improvement and repairs, and provides construction loans for families that have qualified for another mortgage loan product.

Mazaska Owecaso Otipi Financial, Pine Ridge, South Dakota

Founded in 2004, Mazaska Owecaso Otipi Financial (Mazaska) serves members of the Oglala Sioux Tribe living on, or in communities adjacent to, the Pine Ridge Reservation, as well as tribal members on the Cheyenne River Reservation, both based in South Dakota. Mazaska’s mission is to create safe and affordable housing opportunities by providing loans, development services, and financial guidance to help build assets and create wealth. Focusing on homeownership lending, Mazaska provides 30-year traditional mortgages, five-year balloon loans, construction loans, and rehab loans.

Ingredients for Success

Elements of a successful homeownership lending program for tribal borrowers:

- Understand the tribes involved – their traditions, needs, and how they want loan products structured.

- Develop strong relationships with borrowers and the target market–these relationships and the trust that develops are a big part of borrowers repaying their loans and letting you know when issues arise.

- Build strong relationships with funders, the main sources of loan capital for the project–diversify funding and go beyond the CDFI Fund.

- Establish solid lending policies and practices to help mitigate risk and demonstrate to lenders (including sources of loan capital) that mortgage lending can be done.

- Make payments affordable for borrowers–to ensure that they can make timely payments and maintain homeownership.

Impact of Native CDFIs’ Homeownership Lending

Looking at the impact of their work, each of these Native CDFIs underscores that they are putting people in homes–creating homeownership opportunities for tribal families where this opportunity may not have existed. These CDFIs also have realized other important impacts:

- Helping Native families create equity.

- Providing a way for families to build credit (by repaying their loans), which lowers their cost of capital and qualifies them for lower interest rates on other products.

- Showing that low-income borrowers can successfully replay loans (all three CDFIs have strong portfolios with excellent repayment histories).

- Relieving overcrowding as families can move out of tight living situations into their own home.

Native Community Finance is proving that qualifying for a mortgage does not need to be determined by a credit score. With its new POL mortgage loan product, NCF works to determine a loan amount that families can afford, without using credit reports. Instead, NCF’s loan underwriting and qualification process analyzes the borrower’s whole financial picture (debts, income, spending) to calculate what the borrower can successfully repay.

Lessons Learned

In developing their mortgage lending programs, these Native CDFIs point to a number of lessons learned:

- Financial literacy education and homebuyer education is key in preparing families for homeownership, and should be required before closing any loan.

- Adequate software is necessary to track loans, show payment histories, and generate reports.

- Credit reports aren’t always the best way to show the likelihood that borrowers will repay their loans.

- A strong board of directors is crucial–to provide guidance and stay on course.

- Strategic plans are critical to the work of a Native CDFI, and activities need to be aligned with strategic goals.

- Native CDFIs are maturing lenders that must regularly evaluate staffing, structure, products, pricing, and partners.

Ongoing Challenges

Leaders of each of the Native CDFIs agree that finding long-term, low-cost capital for homeownership lending is their biggest challenge. While focusing on business lending can work with shorter-term funding, ideally, homeownership lending means accessing capital for 30-year mortgages.

With this in mind, the Native CDFIs necessarily are creative in assisting tribal families achieve their homeownership goals. In addition to making direct loans to families, Mazaska and NCF provide short-term construction financing that help families build their new homes. When construction is complete, families then access another loan product (such as USDA’s 502 loan, the HUD-guaranteed Section 184 loan, or the VA Native American Direct Loan). Mazaska also provides 5-year balloon loans, which families can then refinance with a private lender.

Beyond accessing capital, other challenges may depend on the community and tribes involved. For Four Directions, because the tribes in Maine are small and the market is somewhat limited, the housing stock may not be as robust. For Mazaska, the prevalence of predatory lending and payroll deductions can be a challenge to working with clients to improve their credit scores. It is difficult to change financial behavior and stay focused on budgeting and saving, when these options are so available.

On the Horizon

Looking beyond their current homeownership lending activities toward the future, each of the Native CDFIs has exciting developments on the horizon:

- Native Community Finance is consolidating with two other Native CDFIs, Cha Piyeh (based at the Ohkay Owingeh Pueblo) and Native Capital Access, based in Phoenix.

- Four Directions is expanding its community development lending products to provide larger-scale development financing to tribes. Building on its work with the Penobscot and Passamaquoddy tribes in Maine, it also is expanding its partnerships with the Maliseet and Micmac tribes, as well as exploring partnerships with other tribes in the region.

- Mazaska is preparing to implement a new 502 re-lending program, where it will use capital received from USDA to make 502 loans directly to qualified tribal members. It also is working with Lakota Funds, a sister CDFI on the Pine Ridge Reservation, to provide mortgages for families living in its Eagle Nest community (a Low-Income Housing-Tax Credit subdivision) who are purchasing their units as the project converts from rental to homeownership.